What a difference between 1931 and 2012!

A previous post looked at the debt crisis which took place in the early 1930s, right in the midst of the Great Depression, and advanced the hypothesis that we could have had a repeat of the destructive Reparation Problem during the Great Recession if the advice of those suggesting to limit intra European Central Bank support (taking the form of so called Target2 balances) would have been followed. 1 It is somewhat ironic that such suggestions came from German economists, like Hans Werner Sinn, who should have been well cognizant of German suffering after World War I. Many economic historians believe that the rigidity and lack of leadership of the interwar monetary system, with the attempt to return to the pre-World War I Gold Standard, was one of the key reasons behind the severity and duration of the worldwide slump as well as the break-up of the system itself. A repeat of such rigidity and lack of international cooperation, combined with no clear monetary leadership, would have presumably led to similar outcomes during the recent crisis.

In this post, we follow the same line of enquiry. Specifically, we compare the financial support that central banks in indebted countries received through the European Central Bank in the €-area during the Great Recession, which peaked in 2012, with what was extended to central banks in indebted countries, specifically Germany, Austria, Hungary and Yugoslavia, in the early 1930s. 2

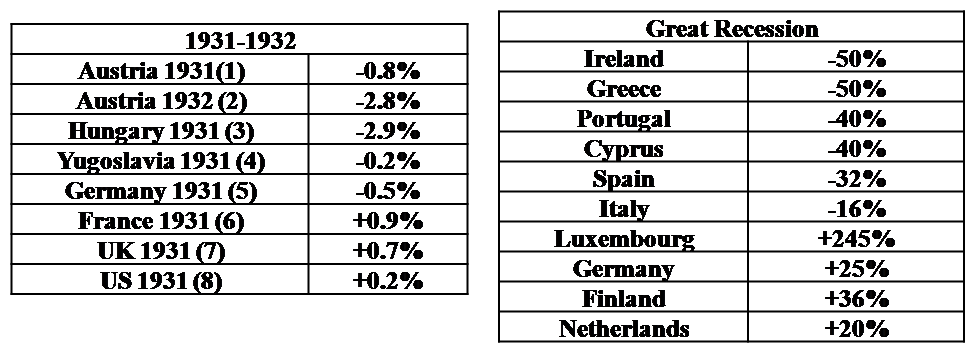

Table 1 reports the amounts, expressed as the share of the receiving and of the granting country GDP, which were extended in the 1930s and in the Great Recession. Where available, an indication of the conditions of the lending (maturity and cost) is also given.

The disproportion between the huge support granted during the Great Recession and the misery of what was given back in the 1930s is immediately clear: both for debtor and creditor countries the support granted during the Great Recession has been a very large multiple of the support offered in the 1930s. In addition, support in the 1930s was very short, while it had unlimited duration (and a cheap rate) during the Great Recession.

Table 1: Financial support among central banks: 1931-1932 vs 2012

As a share of GDP

(A negative figure indicates a debtor position, a positive one a creditor position)

Source:G. Toniolo, Central Bank Cooperation at the Bank for International Settlements, 1930-1973, Cambridge University press, 2005, pages 109-110.

P. Cour-Thimann, Target Balances and the Crisis in the Euro Area , IFO Forum April 2013 Volume 14, Special Issue

Notes:

(1) 13.5 Million dollar/1780.530 Austrian GDP in 1931; The loan had a 3 month maturity and was partially renewed several times

(2) 40.5 Million dollar/1462.71 Austrian GDP in 1932.

(3) 41Million dollar/1390.13 Hungarian GDP in 1931.The loan had a 3 months maturity and was renewed several times and consolidated in 1933

(4) 3 million dollar/1247.061 Yugoslavian GDP in 1931.

(5) 100 million dollar/ 20048.44 German GDP in 1931. The loan had a 3 weeks maturity

(6) 147.5/16474.58 GDP of France in 1931; the total support provided to Austria, Germany, Hungary and Yugoslavia is compared to the Income of the 3 largest creditor countries.

(7) 147.5/21724.43 GDP of UK in 1931; as in note 6.

(8) 147.57/82631.870 GDP of US in 1931 ; as in note 6.

The GDP figures (Estimated levels of aggregate GDP, expressed in current-price US$ and not adjusted for purchasing power) are from: Quantifying the Evolution of World Trade, 1870-1949, by Mariko J. Klasing and Petros Milionis

Target balances have no maturity and their cost is equal to the Main Refinancing Rate of the ECB, which at the end of 2012 was 0.75%.

One can draw five messages from the comparison:

1. While counterfactuals are always difficult to make, there is support for the hypothesis that the avoidance during the Great Recession of the catastrophic effects of the crisis in the 1930s was at least partially due to the much more forthcoming solidarity among central banks. 3 This can be seen as a specific aspect of a more general attitude, whereby the solution to the crisis was, unlike in the 1930s, grounded in international collaboration rather than in protectionism and autarky. 4

2. Germany, and more generally creditor countries, have provided during the Great Recession much more support than one could infer from public commentary and discussion in these countries. Of course, lending did not come from the Bundesbank alone, but the size and economic and financial solidity of Germany made its central bank the linchpin of the intra-central banks financial support during the Great Recession. It should be recalled, however, that this lending was also very profitable for the creditors: in a previous post it was estimated that the ECB, and therefore its owners, i.e. the National Central Banks, made nearly 70 billion € of extra-profits from their action to counter the Great Recession;5

3. Symmetrically, countries in the periphery do not seem to recognize the extent to which they were supported during the crisis;

4. The existence of the (Target2) intrinsic solidarity mechanism centered on the European Central Bank was critical, as it is doubtful that the same degree of support would have been possible without it. The preservation of monetary union, which implied unlimited lending through Target2 balances, within the overall framework of the European Union, was the critical difference with the 1930’s. Destructive positions like those of Sinn could have prevailed if the decision would have not been in-built in a new institution but taken in a highly politicised and discretionary environment, like in the 1930s, 6

5. Arguably, without conditionality, implicit or explicit, whereby the countries receiving financial support corrected their imbalances and vulnerabilities, there could not have been the same degree of financial support. Conditionality was enforced through the European Central Bank, pushing National Central Banks to pursue appropriate policies towards their banking system, and was accompanied, for the countries that had recourse to the financial support of other EU governments, by the explicit macroeconomic conditionality of adjustment programs. One cannot exclude that the rhetoric of creditor countries and of the EU institutions, in particular the EU Commission, had to be tough just to enforce conditionality.

________________________________________

This post was written jointly with Andrea Papadia, PhD student at the London School of Economics. Madalina Norocea provided research assistance. Andrea´s website is available at http://personal.lse.ac.uk/papadia/default.htm

________________________________________

- Target balances and the risk of another “Reparations” problem[↩]

- An analogous line of inquiry is followed by Bordo (TARGET balances, Bretton Woods, and the Great Depression, VOX website, 21 March 2014), who analyses intra-US gold flows rather than international financial flows, as it is done in this post. His conclusion on that case in comparison with the recent € experience resonates closely with the main line of this post: ”Thus, the build-up of TARGET imbalances in the Eurozone since 2007, rather than being a signal for the collapse of EMU – as was the case for Bretton Woods between 1968 and 1971 – was a successful institutional innovation that prevented a repeat of 1933. The TARGET experience reflects learning the correct lessons from the past.” As in the Great Recession, help was extended to debtor countries through channels other than central banks in the 1930a. For example, the Standstill Agreement of 1931 froze all short-term liabilities between countries. The Lausanne Conference of 1932 virtually put an end to reparation payments and, contextually, to inter-allied war debts. The consensus is that these interventions came too late and were too small to turn the tide of the Great Depression. Here we focus on central bank alone.[↩]

- The argument can be extended from intra-European financial support to the global level cooperation among central banks, as illustrated in a Bruegel paper Central bank cooperation during the great recession[↩]

- Toniolo, Central Bank Cooperation at the Bank for International Settlements, 2005, Cambridge University Press, page 87 – “ What if action on war-related debts had been taken six or nine months earlier than it actually was? One may plausibly argue that it might have entirely altered the course of history” and, page 110: “Was the quantity of ammunition supplied sufficient to successfully combat the crisis? Ex post the answer must be negative. Only credit lines several orders of magnitude larger than those initially made available to Austria and Germany might have convinced market of the credibility of the international commitment to the gold standard.”; Kindleberger, The World in Depression 1929-1939, London (1987), Penguin. “ I believe that if the runs on Austria, Germany and Britain had been halted by timely international help on massive scale, the basic recuperative powers of competitive markets would have prevented the depression from going on so long and so deep.” Eichengreen, Golden Fetters: The Gold Standard And The Great Depression, 1919-1939, Oxford University Press, 1992. Page 286: […] in the absence of international cooperation, the gold standard posed an insurmountable barrier to the unilateral pursuit of stabilizing action. Not only were reflationary monetary and fiscal initiatives incompatible with the maintenance of gold convertibility, but efforts to contain domestic financial instability were thwarted and even rendered counterproductive. As domestic banking panics spread contagiously across countries, the monetary authorities stood idly by”; [↩]

- Central bank profits and multiple equilibria [↩]

- Toniolo, page 103: from“summer of 1931…the position of central bankers was more and more that of helpless onlookers than of significant players. They saw the reason for their being gradually sidelined in the increasingly political nature of the crisis and of its solutions”.[↩]