The ECB Asset Backed Securities Purchase Program

In a previous post I concluded that: “…while it is not easy to design and implement an effective ABS purchase program, one can see the contour of a program that would not have dramatic, immediate effects but would help in the medium and long run. … if quantitative easing is seen by its supporters as a tool to jolt the €-area economy into higher growth and closer to price stability, an ABS purchase program is more like a corroborating diet, gradually reinforcing the vigor of the €-area financial system and economy.” In that post I also offered a cautious view of the possible size of an ABS Purchase Program (ABSPP): less than 100 billion. 1

In a subsequent post I reiterated that view, guessing that the joint contribution of Asset Backed Securities and Covered Bond purchases would be unlikely to contribute 20% of the 900 billion increase of the balance sheet of the ECB needed to bring it back to the level reached in the summer of 2012, as announced by Draghi in his September press conference. 2

My cautious view was based on the current conditions in the ABS market, which the ECB and the Bank of England defined as moribund in their recent joint paper, and on the expectation, which proved wrong, that the dominant segment in the ABS domain, Residential Mortgage Backed Securities, would be excluded from the ECB purchase program, consistently with the fact that mortgages were excluded as basis to allocate drawings from the TLTRO.3

Since I wrote the two posts mentioned above, I have read the recent speech of the ECB President in front of the European Parliament: there he clearly foresees that the ECB action will bring a drastic improvement of the ABS market so that the moribund will not only recover but also acquire new vigour. 4

I have also had interesting conversations with some market participants that tend to share the optimistic view of Draghi.

In this post, waiting for the ECB to give details of the ABSPP on October 2nd, I want to examine again its prospects.

Let me start by listing the possible criteria to assess the success of an ABSPP. These can be distinguished in three categories.

The first category would include the characteristics of the program, among these, market observers seem to put a lot of weight on its announced size: a big announced program would be a success and a small one a failure. I think this criterion has clear limitations: a big effort, in term of purchases, producing little results is hardly a sign of success.

The second category would move from the characteristics of the program to its immediate financial effects. These can be distinguished between price effects and quantity effects. The price effects essentially consist of the reduction of the spreads applied to ABS yields. The quantity effects should be measured by the increase of issuance having as underlying legacy assets and, even better, new assets.

The third category includes macroeconomic effects, in particular more lending, especially to SMEs, and eventually less anaemic growth and a return to the ECB definition of price stability: a rate of inflation lower but close to 2.00%.

While the criteria in the third category are, of course, the most important ones and, eventually, the success of the ABSPP should be measured according to them, the assessment of the macroeconomic effects will be a difficult endeavor, which could be attempted only quite a few quarters after the launch of the program. The criteria in the second category can, instead, be assessed more quickly and more easily, while being more significant than those in the first category. Let me, therefore, be a little more precise about them.

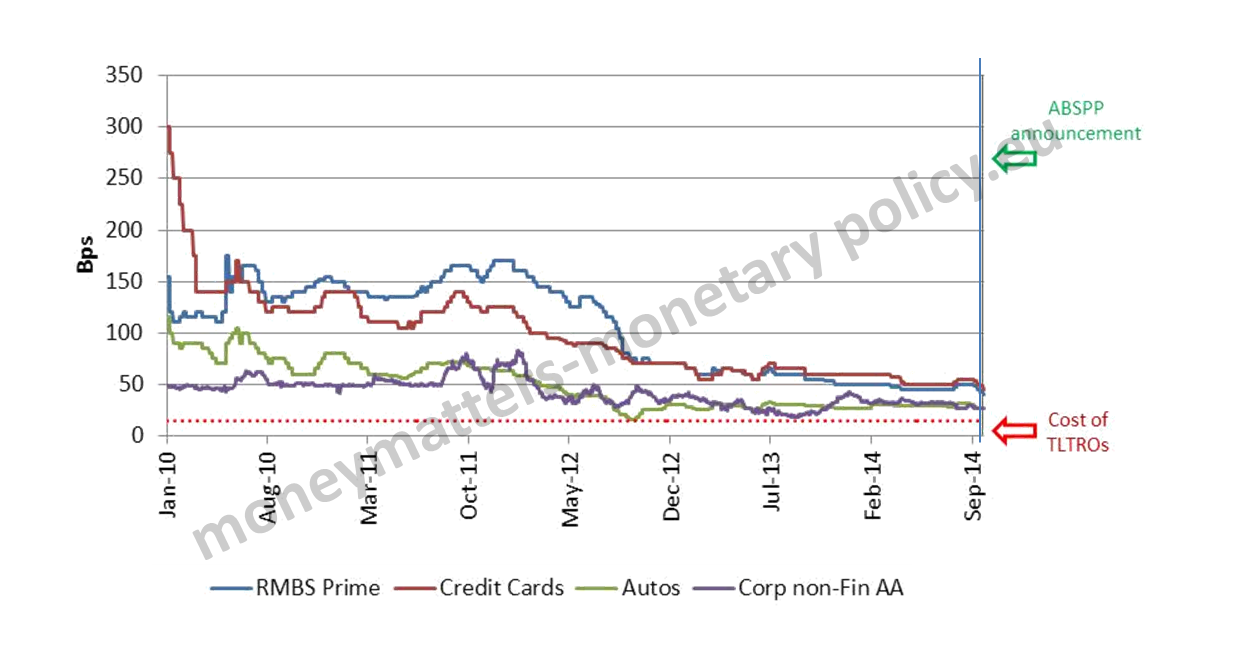

If the ABSPP will turn out to be just an additional, pure funding tools, then the reduced demand for liquidity expressed by banks at the first allotment of the targeted Longer Term Refinancing Operations (TLTRO) can be taken as a bad omen for the success of the ABSPP. In addition the ABSPP will have a difficult time competing with very cheap TLTRO. This last aspect can be easily seen in Chart 1.

Chart 1: Yields on different types of European Asset Backed Securities

Source: BofA Merrill Lynch Global Research

Note: Yields are shown as spread over Euro-libor.

We see in this chart that there has been a substantial compression of yield spread over Libor since the peak reached some three years ago. With a magnifying lens one can also detect a further compression of some 10-15 basis points after the announcement by Draghi last week that the ABSPP had been indeed decided. Given that euro-Libor is about zero currently for short maturities, the most recent part of the curves, while strictly speaking being a spread, can be considered as indicating the absolute yields on the senior tranche of all categories of ABS, which are still significantly higher than the 15 bp cost of the TLTRO. A weighted yield, including the higher cost of equity and mezzanine tranches, would necessarily be even higher. Of course, once one adopts, as it should be done, a portfolio approach to liabilities, the conclusion to put all eggs in the basket of the cheapest liability reveals itself as fallacious, as does the prescription to concentrate a portfolio of securities in the one with the highest yield. Still, with current yields, there is not much room for ABS in a portfolio of liabilities.

Of course, a successful ABSPP should further lower the yields, as foreseen by Draghi. There should be two important channels bringing about this result. First, a portfolio balance effect: as the ECB purchases, and is seen continuing purchasing, for a sustained period of time, ABS, their yield should go down and investors should move towards riskier assets, including junior tranches of ABS. In a way the mechanism should be analogous to that underlying the effectiveness of Quantitative Easing in the US. A second contribution to yield reduction would come if the ABSPP increased the liquidity of the ABS secondary market, which is currently very limited: according to Alexander Batchvarov, International Structured Finance Strategist at Bank of America Merrill Lynch, secondary trading amounts to only 2.0-2.5 billion per week.

There can legitimately be different views on what will be the effect of the ABSPP on yields: if the effect generated when the program is implemented would be, say, twice the 10-15 announcement effect recalled above, then ABS would definitely become an interesting funding tool for banks.

It may be risky, however, from the ECB point of view, to count on this large compression just from its purchases. This is, in my understanding, the reason why the ECB is insisting on three other aspects:

1. A precise definition of High Quality (or Qualifying, according to the ECB-BOE name) Securitizations. Here my view is that the one elaborated with market participants by the Primary Collateralised Securities initiative, which I chair, and which is widely used in the market since nearly two years , is an obvious candidate. 5 It is also to be hoped that the ECB definition will be consistent with the one that is expected from the European Banking Authority for the beginning of October;

2. A substantial revision of the regulations of ABS, in particular those of high quality, which would make them more consistent across different assets and calibrated on the actual performance of ABS in Europe, which was incomparably better than that of US subprime, still tainting the overall image of ABS. 6

This revision, which the European Commission could, if it so wished, announce quite quickly , would have a tonic effect on the demand of ABS, both for senior and junior tranches; 7

3. The request of guarantees that would allow the central bank to extend its purchases to the junior tranches of ABS. The French and German ministries of finance are, according to press reports, against guarantees, but it cannot be excluded that public banks, like the KfW (Kreditanstalt für Wiederaufbau), CDC (Caisse Depots et Consignations) and the CDP (Cassa Depositi e Prestiti), for instance, could complement the ECB action with purchases of junior tranches of ABS or that they could offer partial guarantees, that would only cover the purchases of the ECB;

The second and third aspects mentioned above would, in particular, add a capital relief dimension to the funding dimension, which would be particularly important to recreate room for banks to increase their lending and thus achieve the macroeconomic effects that are the ultimate objective of the ABSPP. Indeed in this way they would clearly differentiate the ABSPP from the TLTRO.

In conclusion, it would be wrong to judge the prospects of the ABSPP only, or even mostly, on the announced size of the purchases, if indeed there will be one. The success of the program depends on the improvement it will bring about to the ABS market: will it raise it from its moribund state and transform it in a vibrant venue with more supply and demand? Or will the more skeptic view I presented in previous posts prevail? The three conditions mentioned above are the really important ones to assess which development will prevail and thus the prospects of the ABSPP, market participants should focus on them rather than on the size of the program.

This post benefitted from conversations and inputs from Alexander Batchvarov, International Structured Finance Strategist at Bank of America Merrill Lynch and Ian Bell, Secretary of PCS, but the responsibility of its content is only with the author. Madalina Norocea provided research assistance.

- About elephants and ABS[↩]

- Liquidity supply and demand in the €-area: a schematic approach[↩]

- The Impaired EU Securitisation Market: Causes, Roadblocks, and How to Deal With Them, ECB and BOE joint paper on securitization, March 2014[↩]

- “…the ABS market remains severely impaired – so that the potential for interventions for changing market dynamics is high in that particular market” “The total stock of eligible securities which is currently outstanding … is already sizable. We are confident that it will grow as a result of our presence in the market. …market size and purchasing volumes are to a certain extent co-determined and endogenous.”[↩]

- The amount having received the PCS label has recently reached 100 billion[↩]

- William Perraudin, High quality securitisation. An empirical analysis of the PCS definition, May 2014, available at pcsmarket.org[↩]

- When announcing the mandates for the EU financial stability commissioner, President Juncker set a three month deadline to resolve the HQS problem[↩]

The relevance is in the potential, not in the current volumes. The potential is now widely recognised (ECB, Bank of England, European Commission, EBA, Eiopa,……) and has a strong economic basis.