Target balances and the risk of another “Reparations” problem

The crisis that started in 2007, threatened the global economy with the demise of Lehman Brothers in the Autumn of 2008 and moved to Europe in the Spring of 2010, where it is still not surpassed, has shaken the trust of laymen and economists alike in the ability of economics to predict and manage events. The analogy with physics as a science and engineering as a technique has been found wanting.

A consequence of this reconsideration has been the effort to complement the analytics of economics with the lessons of economic history. Confronted with the most serious crisis since the thirties, it was natural to go back exactly to that period. Attempts have been made, in particular, to understand better the European phase of the current crisis looking back at the reparations problem that poisoned the relationships between Germany, on one hand, and the winners of World War I, on the other hand, until Hitler came to power and relationships started to move in the belligerent direction that eventually led to World War II.

A consequence of this reconsideration has been the effort to complement the analytics of economics with the lessons of economic history. Confronted with the most serious crisis since the thirties, it was natural to go back exactly to that period. Attempts have been made, in particular, to understand better the European phase of the current crisis looking back at the reparations problem that poisoned the relationships between Germany, on one hand, and the winners of World War I, on the other hand, until Hitler came to power and relationships started to move in the belligerent direction that eventually led to World War II.

This post also refers back to the events of the thirties, and in particular to the reparations that Germany was supposed to pay to the winners of World War I, arguing that a mishandling of Target balances could have produced somewhat similar catastrophic consequences.

To make the point it is necessary to clarify the nature, size and consequences of Target balances. These have been examined by many economists, from the alarmist and politically tainted treatment of Sinn and Wollmershaeuser (2011), to the more technical and objective treatment of Bindseil and König (2011 and 2012), Bindseil and Winkler and Buiter and Rahbari (2012). Cour-Thimann (2013) finally provides an encyclopaedic treatment of Target balances, covering all their possible aspects from every possible perspective[1].

Without rehearsing the analyses and the controversies in the papers mentioned above, it is useful to retain here 5 conclusions:

1. Target balances are the necessary consequence of an asymmetric crisis in a monetary union – when there was no crisis there were no significant Target balances, if there was no monetary union there would not be Target balances.

2. Target balances measure the support that the Eurosystem provides to the periphery. More specifically, Target balances are the reflection of the uneven distribution of central bank liquidity throughout the euro-area, much more abundant to banks in the periphery than in the core. In this way, the Eurosystem fills the gap created by the withdrawal of private funding that generates capital flows from the periphery to banks in the core. Central banks thus offset the “sudden stop in private capital inflows” (Pisani-Ferry 2012) that had financed over the years the current account deficits of the countries in the periphery.

3. If the creditor central banks would insist, against the rules but following the proposal of Sinn and Wollmershaeuser 2011, ”that the Target balances are paid annually with marketable assets”, given that debtor central banks would not have, in aggregate, enough marketable assets[2], the consequence would be a severe debt position for some states in the periphery towards some other states in the core of the euro-area and debtors would need very quickly huge current account surpluses (or implausibly large private capital inflows) to repay their public international debt.

4. If a limit, explicit or implicit, was established on Target balances and thus market participants would no longer be assured that, at any point in time, the Eurosystem would make good the liabilities of all its members, inevitably runs on central banks would follow, threatening the existence of the euro.

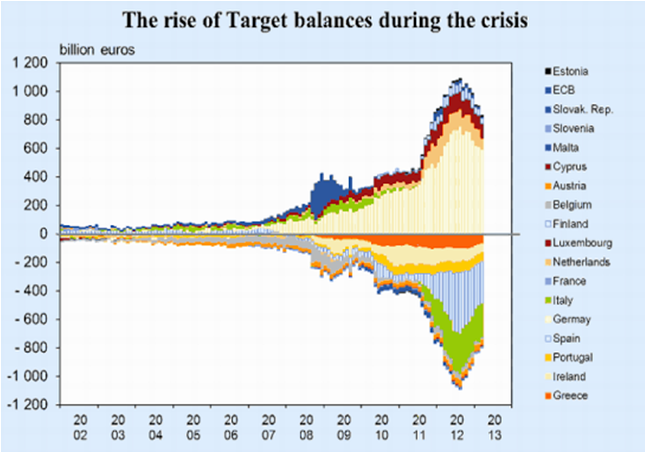

5. Target balances are large, correspondingly large is the problem they would represent in case a swift settlement was required (see the following Chart, drawn from Cour-Thimann 2013).

|

| Source: P. Cour-Thimann, Target Balances And The Crisis, April 2013 |

The same author reports the target balances at the end of 2012 as a per cent of national GDP as follows:

“In relation to their home countries’ GDP, NCBs’ Target balances were particularly large at the end of 2012 for Luxembourg (+243 percent of GDP), Ireland and Greece (around -50 percent of GDP), Portugal and Cyprus (around -40 percent of GDP), but also Finland (+36 percent of GDP), Spain (-32 percent of GDP), Germany (+25 percent of GDP), the Netherlands (+20 percent), and Italy (+16 percent).”

The figures for Ireland, Greece, Portugal, Cyprus and Spain were, at the end of 2012, of the same order of magnitude or higher, in per cent of GDP, than the amounts of the reparations for Germany finalised at the Conference of Lausanne in 1932 (about one third of German income at the time), even if much lower than those that Germany was initially supposed to pay.

Fortunately, the idea that Target balances should be “repaid” was not considered seriously in any policy circle and, thanks to the lessening of tensions since the Summer of 2012, Target balances have started to decrease and the trend has not even been broken by the crisis in Cyprus in the Spring of 2013.

In conclusion, a possible catastrophic event has been avoided; the inter-central banks capital flows giving rise to Target balances have given time to countries in the periphery to start correcting their imbalances[3] while avoiding even graver recessions; the, implicit and explicit, conditionality attached to the support that the core of the euro-area has given to its periphery has dealt with the moral hazard problems that unconditional help would have created; finally, significant institutional innovations are being implemented in the fiscal and banking domains to remedy the design flaws of a perfect monetary union with an insufficient economic union. The crisis, as mentioned above, has not been surpassed and adjustment fatigue in the periphery, the difficulties to finalize the necessary institutional innovations, the poor macroeconomic conditions in the euro-area as a whole and, in particular, the recession in the periphery could still bring a rekindling of tensions. Recognizing the difficulties ahead should not, however, hide the fact that the euro-area, with its awkward, reactive, “on the brink” (Bergsten and Kirkegaard, 2012) approach is moving in the right direction with sufficient speed.

References

F. Bergsten and F. Kirkegaard (2012), The Coming Resolution of the European Crisis: An Update, Peterson Institute Policy Brief, Number PB12-18.

U. Bindseil and P.J. Koenig, (2011) The economics of TARGET2 balances, SFB 649 Discussion Paper, 2011-035.

— _— (2012) ‘TARGET2 and the European sovereign debt crisis, Kredit und Kapital, 45 (2), 135–174.

U. Bindseil and Adalbert Winkler, Dual liquidity crises under alternative monetary frameworks– a financial accounts perspective’, ECB Working Paper Series No. 1478.

Willem H. Buiter, E. Rahbari , Target2 Redux The simple accountancy and slightly more complex economics of Bundesbank loss exposure through the Eurosystem, November 1, 2012.

P. Cour-Thimann, Target Balances And The Crisis In The Euro Area, Special Issue of CES-IFO papers, April 2013,Volume 14.

J. Pisani-Ferry, S. Merler, Sudden Stops In The Euro Area, Bruegel Policy Contribution, March 2012.

H. W. Sinn and T. Wollmershaeuser, (2011), Target Loans, Current Account Balances and Capital Flows: The ECB’s Rescue Facility, NBER Working Paper 17626 (2011).

[1] The only regret is that the ECB does not publish information on the split of monetary statistics for the countries of the euro-area that the article widely uses.

[2] Cour-Thimann reports, for example, that gold holdings and foreign currency reserves of the Bank of Greece amount to 6 billion euro, while the Target negative balance of that central bank is around 100 billion. The only assets a peripheral central bank could transfer in sufficient amounts to a core central banks would be its lending to local banks: would the Bundesbank really be interested in lending directly to Greek banks?

[3] Current account balances have moved or are forecasted to move towards balance in most of the peripheral countries.

“4. If a limit, explicit or implicit, was established on Target balances and thus market participants would no longer be assured that, at any point in time, the Eurosystem would make good the liabilities of all its members, inevitably runs on central banks would follow, threatening the existence of the euro.”

Yes, I totally agree with this post, especially the point you make above. I wrote something here that addresses the bank run problem that will inevitably emerge should Target2 imbalances be capped.

Welcome to the econblogosphere.