Cimabue and Giotto, the Bundesbank and the ECB: an analogy?

Cimabue is defined by the Encyclopaedia Britannica as “the last great Italian artist in the Byzantine style”,while in the web-site of the Louvre one reads that Giotto “has been seen down the centuries as the instigator of a painting revolution without precedent since ancient times”. Dante Alighieri in his Divina Commedia so defines the relationship between the two painters: “Credette Cimabue ne la pittura tener lo campo, e ora ha Giotto il grido,

sì che la fama di colui è scura”, which can be translated in English as “Cimabue thought to hold the field in painting, and now Giotto hath the cry.”

Painters and central banks do not have much in common, even if both are said to practice an art. And history of art books do not report that Cimabue and Giotto ever confronted themselves in front of a court, as the Bundesbank, represented by its President, Weidmann, and the European Central Bank, represented by one of his Board Member, Asmussen, did last June in front of the German Federal Constitutional Court. Still there are some analogies between the relationship that Giotto had to his master and that of the European Central Bank to the Bundesbank. To understand this relationship and thus also help forecast the behaviour of the European Central Bank, it is useful to see in what way the European Central Bank kept with the tradition of the Bundesbank and in which way it innovated it.

The main legacy from the German central bank to its European counterpart is the monetary technology[1]founded on an independent central bank devoted to the primary objective of price stability. This technology was severely tested during the Great Recession, when central banks in a number of advanced economies had to go to the limits of their abilities and competences to avoid that a Great Recession would transform itself in a repeat of the Great Depression[2]. Still, no clear superior alternative has emerged to this technology, which affirmed itself, thanks to the Bundesbank, after decades of trials and errors in managing a fiat currency, following the demise of the gold standard. And the ECB has shown to use, in an innovative way as we shall see, this technology also during the crisis, as shown by the following two charts.

The first chart illustrates that the control of inflationary expectations has been as perfect as human things can be, having been consistently kept below but close to 2% since the launch of the euro.

Chart 1: Inflation Expectations (Professional Forecasters). 1999-2013

Source: European Central Bank

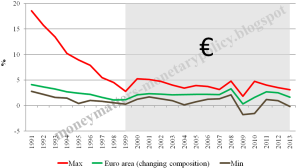

The second chart shows that ECB has managed to effectively control not only inflation forecasts but also actual inflation throughout the euro area since it took the responsibility of monetary policy.

Chart 2: Inflation developments within €-area countries, 1991-2013.

Source: European Central Bank

While the attachment to price stability as an objective and to central bank independence as an organization principle remained solid, the reliance on monetary aggregates substantially faded over the years[3] in that part of Frankfurt occupied by the European Central Bank. Indeed experience showed that it was simplistic to take a reference growth rate of a monetary aggregate as an intermediate target. Money can give useful information for the conduct of monetary policy, but extracting this information requires much more analysis than just comparing the actual rate of growth of money to a reference rate. As a consequence, the so-called second pillar of the monetary policy strategy of the European Central Bank is more a memo item than a real guide. If anything, my sense is that it took too long to the European Central Bank to unshackle itself from a misguided devotion to monetary aggregates.

A real difference between the Bundesbank and the European Central Bank is to be found in the attitude towards the internationalization of the currency. For long years the Bundesbank fought a quixotic fight to try and avoid the internationalization of the D-mark, lest the conduct of monetary policy be disturbed. The European Central Bank took, instead, an equanimous approach to the internationalisation of the euro: if international agents found it useful to use the single currency for some international purpose, the ECB would not oppose it. It would not, however, have as an objective a wider international use of the euro, even if one can perceive some sense of satisfaction in those Reports on the International role of the euro[4]where some progress is documented.

More generally, the European Central Bank has had full awareness of being the second most globally relevant central bank after the FED, while the Bundesbank inevitably considered itself a national institution. The only area in which the ECB arguably did not fulfil all its responsibilities as a global institution was in its restricted approach in granting euro swaps to non-euro but European central banks during the crisis, thus somewhat not fully standing up to its role as regional monetary leader.

Another area in which the European Central Bank differed from the Bundesbank has been in its attitude to purchases of government securities. While the Bundesbank had and still has a revulsion towards purchases of government securities, arguably as a consequence of the havoc played by such purchases in the hyperinflation of the twenties, the European Central Bank has shown a much less anxious attitude toward these purchases, recognizing that they are a legitimate tool to implement monetary policy. This difference of attitudes emerged strongly when the European Central Bank announced the Outright Monetary Transaction (OMT) program and led to the confrontation in front of the German Constitutional Court mentioned above. While seeing two institutions that should tightly cooperate in conducting the monetary policy of the euro area arguing one against the other was definitely a sorrow experience, it is legitimate to ask which of the two institutions will suffer more for it. My sense is that this will be the Bundesbank rather than the European Central Bank. When future developments will show that not only the OMT helped dealing with the crisis but also that it caused no inflationary dangers, the Bundesbank will be seen as having made a big mistake in opposing it so vocally and stubbornly. This could weaken the voice of the Bundesbank in the Governing Council of the ECB: when in future the President of the Bundesbank would object to some policy move, even with more solid motivations than the ones he used for opposing the OMT, his opposition could meet an easy, and unwarranted, rebuke from other members of the Council referring to the “wrong” opposition to the OMT. The necessary support for sound central banking principles could, as a consequence, be weakened in the Governing Council of the European Central Bank.

To complete the picture let me mention one more similarity and one more difference between the two institutions.

A similarity is the expectation, which the experience during the European phase of the Great Recession did not confirm, that fiscal restrictions can quickly lead to improved confidence, offsetting their effect on aggregate demand: in discussions within the troika administering the programs in Greece, Portugal and Ireland, the European Central Bank, as well as the Commission, tended to take the more hawkish position in the fiscal domain, so much that the IMF, notwithstanding the fact that its acronym is often meant to mean “It´s Mostly Fiscal”, was seen as something of a wimp in budgetary matters.

A difference is the attitude towards the market: the Bundesbank maintained an aloof attitude towards market participants, it did not really look for intimate contacts. The European Central Bank, instead, has gone out of its way to establish smooth, frequent and free contacts with market participants, and these paid handsomely when these helped the central bank understand the gravity of the crisis that started in 2007.

Overall, the European Central Bank could not have been created if the Bundesbank had not had the success that it had in the control of inflation since after the German monetary reform in 1948. Similarly, Giotto could not have painted the way he did if Cimabue had not preceded him. Judge by yourself which painter you prefer.

[1] Mercier and Papadia: The concrete euro, Oxford University Press 2011.

[2]Papadia, Central bank cooperation during the Great Recession

[3]Papadia and Daluiso, Where has all the (base) money gone?

The comparison of the OMTs to Giotto is indeed interesting.

There is a theory that the development of perspective in painting at the beginning of the fourteenth century was encouraged by the Catholic church which was worried that the rejection of earthly life by the heretics of the times (notably the Cathars) was a grave risk to the church. By presenting paintings in a more realistic way ( hence the perspective) the church wanted to convey the message that life before death is just as real and important and thus the Cathar rejection of life was wrong.

In that sense Giottos’ paintings are “realistic” which means that they resemble (the three-dimantional) reality though of course they are an illusion ( in two dimensions on a flat wall).

So it’s interesting to see the OMT as an illusion, an article of faith, as everything about money at the end is

thanks Francesco for sharing your competence and reflections.

I would like to add an additional perspective for the relationship between ECB and the Bundesbank. The former is a decision maker, i.e a manager, the latter was a decision maker but has become, on monetary policy matters, a wise and experience adviser.

Advisers have sometimes the lucky position that they can raise the risks, point out misbehaviors, suggest solutions but ultimately is the manager that has to take a decision and bear the responsibility. On the other hand the manager that does not listen carefully his/her advisers is in the long run deem to fail, and history is full of such examples. Working for 9 years at the ECB, I am among those who witnessed how a good manager you have been.

The OMT that you mentioned is one important example where the conflict has emerged between the manager and the adviser, especially because short term financial stability and euro existence objectives may have conflicted with some long term ones, including the right incentives to country discipline towards in a well-functioning federation. This is also because the ECB’s control on the road map to build a genuine EMU, and ultimately a political union, is limited and currently is in the hands of member states. In other words, on non-monetary policy matters, the EU plays the adviser’s role and you have 17 or 28 managers, depending on the geographical perimeter.

This institutional inconsistency is the main root of our problems, and is being partly addressed with the Single Supervisory Mechanism. Until we, at least the euro area, have reached a non-turning point towards the United States of Europe, a government for the single currency, I would argue that the ECB decision on the OMT was correct but we will not be able to judge it in the long run because it depends on the exogenous factors.

Importantly, the strong resistance played by the Adviser, Buba, has probably helped the Manager, ECB, to introduce a fundamental element in the OMT which was missing in the first purchase of government bonds in 2011, namely the conditionality on exogenous factors.

I do not know who has invented the conditionality element but I believe this was really an excellent decision to manage intertemporal and institutional inconsistencies. Until it is credible, OMT incentives can temporarily achieve a comparable outcome as a Treaty change, though Germany prefers the Treaty change. The conditionality is giving some sort of managerial responsibilities to the EU level by strengthening the EU Commission role and has introduced costs and constraints for the (country) managers. Germany is an experienced Adviser in terms of federation and we cannot neglect it. The incentives introduced by the conditionality are closer to a marked-oriented tool, a sort of self-regulation by the Manager. The Adviser is telling us that self-regulation is not sustainable and we need to enforce those incentives into “regulation”, a real constitution of the United States of Europe. Against this reading, both the Manager, Giotto, and the Adviser, Cimabue are right.