Will lower rates help the ECB in regaining price stability?

Draghi has opened up the possibility, at the last press conference, of a further reduction of the rate on the deposit facility, which seemed beforehand to be excluded.

It is in my view likely that this move will indeed be taken already in December, even if probably not unanimously, since Hannson, the governor from Estonia 1, and Rimšēvičs, governor of Central Bank of Latvia 2, as well as Klaas Knot, governor of Central bank of Netherlands, have recently said that they do not see the need of further easing, thus breaking the kind of consensus that was seemingly emerging in the Governing Council. In addition Mersch cautioned about the impact of negative rates.

While the probability of a cut is high, we do not know what the size of this cut could be, nor whether it would also be accompanied by a cut of the Main Refinancing Operations (repo) rate.

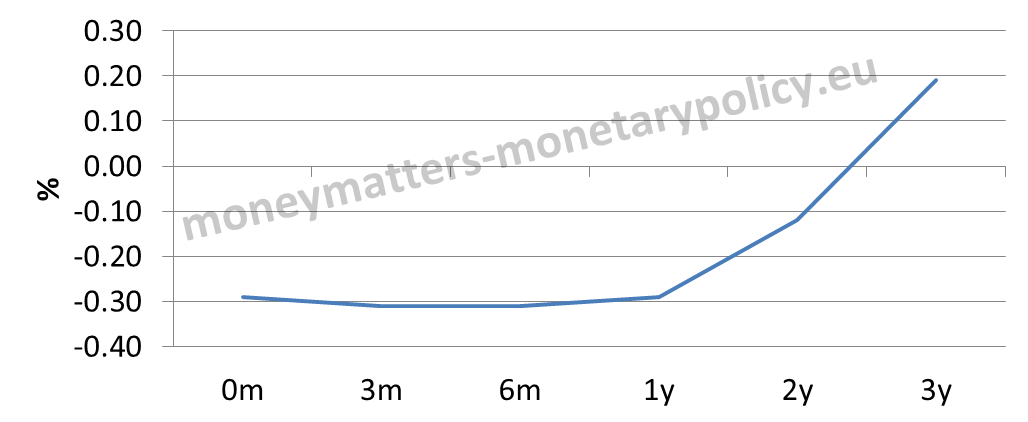

As regards the size, market commentary is concentrating on a 10 basis points cut and this is consistent with OIS forward rates, as seen in Chart 1. Some observers, however, think the ECB could go nearly as deep into negative territory as the Swiss National Bank, and thus the cut could be up to 50 basis points.

Chart 1: EUR OIS Curve

Source: Barclays Live

(*)Note: The chart reflects the EONIA Forward Interest Rate Swap, cut off date 13 Nov 2015

As regards the MRO rate, its importance is reduced in the current situation of very ample liquidity that pushes EONIA to the bottom of the ECB rate corridor, i.e down to the deposit facility rate, but it still carries some weight because the cost of the funding operations of the ECB are determined by it.

Of course the two issues are connected, as it is more likely that also the MRO rate will be reduced in case of a deep cut of the deposit rate.

To simplify matters, in this post two extreme scenarios will be explored: in the first one the deposit facility rate is reduced by 10 basis points to – 30 basis points and the MRO rate is left unchanged, at +5 basis points; in the second scenario the deposit facility rate is cut by 50 basis points to – 70 and the MRO rate is reduced by 30 basis points to – 25 basis points. To grasp the boldness of this latter move, it should be realized that the ECB would pay banks a non trivial amount of money to give them incentives to borrow large amounts from itself. Any possible rate cut will be bracketed by the two scenarios.

The question is what could be the effect of a rate cut on inflation, either looking directly at the semi-elasticity between interest changes and inflation or breaking down the causality chain into two segments, from the interest rate to the exchange rate of the € and then from the exchange rate to inflation.

In order to provide some back of an envelope calculations of the effect on inflation of a rate cut we need:

- Either directly the semi-elasticity between the interest rate and inflation or

- The semi-elasticity between the interest rate and the exchange rate, both bilateral against the dollar and effective,

- The elasticity between the bilateral exchange rate of the € against the dollar and the effective exchange rate of the €,

- The elasticity between the effective exchange rate and inflation.

We also need to assume the degree to which the potency of a reduction of the deposit facility rate is increased if also the MRO rate is cut. Faute de mieux, I assume that the potency of a cut of both rates (which I call the potency parameter) is 25 per cent higher than that of a cut of only the deposit facility rate.

My assumptions about the relevant elasticities as well as the potency parameter are reported in table 1 below, which harness reasonable estimates drawn from different sources, including the ECB:

Table 1. Parameter and elasticities to estimate how an interest rate change is reflected into inflation.

| Parameter/elasticity | |

| Potency parameter | 1.25 |

| Semi-elasticity interest rate-inflation | 0.2 |

| Semi-elasticity interest rate-bilateral exchange rate | 5.0 |

| Elasticity bilateral €/$-effective exchange rate | 0.57* |

| Semi-elasticity interest rate-effective exchange rate | 2.85** |

| Elasticity between effective exchange rate and inflation | 0.06*** |

- * This elasticity is calculated as the ratio of the percentage change in the effective exchange rate of the € to the percentage change of the €/$ rate over the last 5 years.

- ** The semi-elasticity between the interest rate and the effective exchange rate is obtained from the multiplication of the semi-elasticity between the interest rate and the bilateral €/$ exchange rate and the elasticity between the bilateral and the effective exchange rate.

- ***This elasticity is often defined as “pass through” from the effective exchange rate to inflation.

We can combine the parameters and elasticities in table 1 with our two scenarios for interest rate cuts to get a range of possible changes in inflation. The results are reported in table 2.

Table 2. Range of changes in inflation for different scenarios about interest rate cuts and different parameters and elasticities (Basis points).

| Interest rate to inflation(1) | Interest rate to bilateral exchange rate to effective exchange rate to inflation(2) | Interest rate to effective exchange rate to inflation(3) | |

| Scenario 1 (Deposit rate -10 bp) | 2 | 1.7 | 1.7 |

| Scenario 2 (Deposit rate – 50 bp; MRO rate – 30 bp) | 12.5 | 10.7 | 10.7 |

In the table the different estimates of the increase in inflation, over a horizon of about 3 years, are reported for the two scenarios of reduction of ECB rates and for different paths and parameters. Of course, given the assumptions in table 1, the effect on inflation is the same in columns (2) and (3). Presenting both cases can facilitate, however, calculations if one would choose different elasticities in table 1 3. The overall message is that the effects on exchange rates and inflation are pretty small. They are indeed trivial if the deposit facility interest rate is reduced by only 10 bp. They are, however, still quite small, around 10 basis points, if the ECB would take the very bold path of reducing the deposit facility rate by 50 bp, i.e as far as the Swiss National Bank and as far as it seems possible to do it. It should be recognized, though, that the estimated lower bound of interest rates is uncertain and is now lower than it was previously thought. Indeed Draghi himself admitted as much in his latest press conference. In a previous post 4 I also recently advanced the hypothesis that the lowest level to which rates could be pushed down was just -25 basis points.

Of course, the parameters and elasticities in table 1 are not at all invariant to economic conditions: we know, for instance, that the effect of interest rate changes on inflation is not constant. Still, the parameters would really need to be implausibly different from those in table 1 to produce significant effects on inflation.

In conclusion a further reduction of the ECB rates is unlikely to help much the ECB to regain price stability. At most it could have a supporting role. The heavy lifting should be done by some other measure. While Draghi has hinted that the ECB has many arrows in its quiver when, unlike Leporello in Mozart-Da Ponte opera, he denied that there is a fixed catalogue of measures that the ECB could take 5, it is not clear to me which arrows the quiver actually contains, other than a further interest rate reduction and a time or size expansion of Quantitative Easing. My readers should be aware that I wish that the ECB would consider interventions in the inflation derivative market as a new tool 6 but I discern, alas, still no sign of this. Of course the phantasy of market operation people at the ECB should not be underestimated, and so they could provide a new rabbit that Draghi could pull out of his cylinder. We just have to wait a couple of more weeks to find out.

This post was prepared with the assistance of Madalina Norocea.

- “Knowing what I know now, I don’t think the ECB should act. We know that some countries have gone lower than the ECB but we also know that those are small jurisdictions. I think nobody knows exactly where that kind of new lower bound is but it is lower than where we used to think it is in the past.” Ardo Hansson, Governor of Central Bank of Estonia.[↩]

- “We still feel that the programme has just started. Probably, there is no need now to rush into anything, especially before the end of the year” Ilmārs Rimšēvičs, governor of Central Bank of Latvia.[↩]

- Indeed a little spread-sheet is enclosed in this post, into which the interested reader can input different parameters to see how the results change. Click here [↩]

- Should we worry that we have about the lowest interest rates in the history of humanity?[↩]

- Draghi in his interview to Alessandro Merli in Il Sole XXIV ORE of October 31th 2015.[↩]

- A help for the ECB from the derivative market [↩]