Was the € a good idea?

The question in the title is inspired by an anecdote. While we were living in Frankfurt, my wife and I took the opportunity to tour Germany. The destination of one of these tours was Trier and over there we visited the house of Karl Marx. In the small museum shop (even Marx is commercialized these days!) I saw a poster with a rascal-looking Karl Marx admitting: I am sorry, guys, it was just an idea!

In its simplicity, the poster sent two important messages: first, one can easily downplay the importance of ideas; second, it may take very long to conclude whether an idea is good or not.

These two messages are a sort of preamble to this post: the idea to create the € is one with vast implications and its too early to pass a definitive judgment about it. A little parallel will reinforce my point: just when the Italian lira was about to be substituted by the euro, there was still a discussion whether the monetary unification of Italy in 1861, when the country itself was unified, was a good idea.

In fact, a full answer to the question in the title would require dealing with complex political, indeed historical, issues. In order to limit my post to a workable size and, more importantly, to the borders of my competence, I will first only consider economic factors. I will subsequently explore specifically what the crisis that engulfed the € since 2010 means in terms of answering the question in the title.

Even if drastically simplified, the economic based answer to the question in the title would require a complex counterfactual exercise, reconstructing what history would have been without the €. For instance, one would have to answer questions like: what would have happened to Italian debt if the introduction of the € would have not drastically reduced its cost or where would have the D-mark gone if it would not have been substituted by the €?

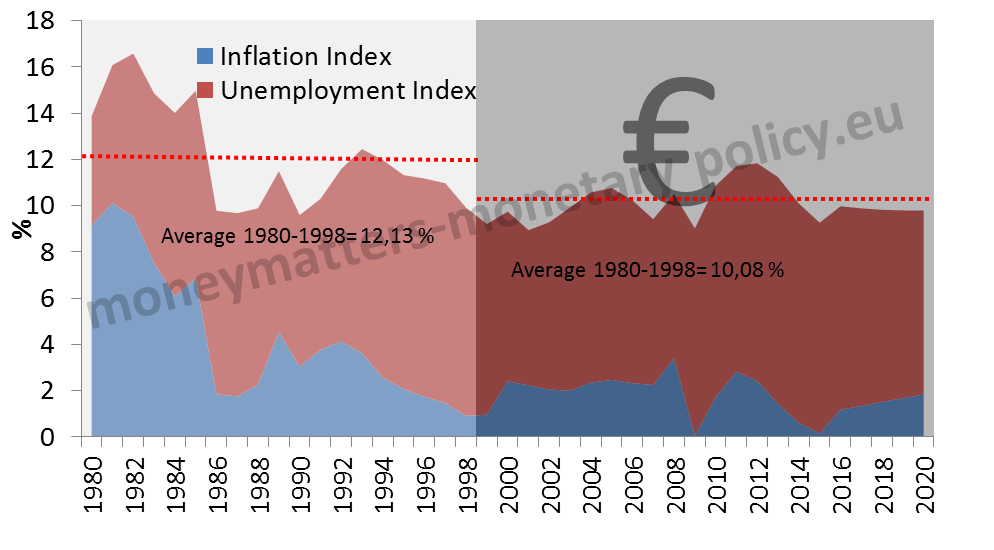

In order to further simplify my approach, in the tradition of so-called misery indices, I will look at its two components: unemployment and inflation. The simple idea behind misery indices, originally thought by the American economist Arthur Okun, is that unemployment and inflation are two macroeconomic “bads”, the sum of which is a synthetic (negative) indication of the welfare of a country. Of course this index loses some of its value when inflation is too low, like now, still it gives a rough indication of the macroeconomic conditions of a country. Specifically, I will assess the resulting composite misery index in the € area against two standards of comparison: one over time and the other over countries. The over time comparison looks at the economic performance of the € area countries (and I will limit the analysis to the initial 11 participants) during the € period with respect to that before the introduction of the €. The over countries comparison looks at the economic performance of the € countries since the introduction of the € against that of EU countries not members of the €-area.

Chart 1. Misery index: pre and post €.*

*11 initial participants to the €.

Source: IMF WEO

The misery index does not send a definitive message when the experience of the 11 initial € participants in the circa two decades of the € period is compared with their experience in the two previous decades: the average of the misery index for the first period is higher than in the second, indicating some improvement in the € time, but it is not obvious that one can make too much out of this difference, also taking into account the imprecision of the index as an indicator of welfare.

The comparison between € and EU-non-€ countries is given in chart 2.

Chart 2. Misery index of €* and EU-non-€ countries. 1998=100

* All 18 € countries

Source: IMF WEO

In the chart, EU countries not part of the € area do somewhat better than € countries in terms of misery index since around 2012, but the two misery indices crossed each other previously and I would not conclude that definitely the € favoured or damaged the € area economic performance with respect to that of EU countries that were not in the €.

Taking the message in the two charts at face value, we should say that, in the two decades with the €, € countries did better than they did in the previous two decades but worse than EU-non-€ countries.

I do not think, however, that such literal reading is justified. The general message that I draw from these two charts, instead, is that it is not obvious that the € damaged the economic performance of the countries that adopted it. Neither can one conclude, however, that it clearly improved it.

Indeed, I believe that any attempt to assess whether the € was a good idea or not requires answering a fundamental methodological question: is a period of about 20 years of economic developments with the € adequate to judge whether it was a good idea? You already know my answer from the point I made about assessing the validity of ideas, whether communism or the euro. Specifically, my sense is that an epochal project like the € requires a longer, secular time dimension to be assessed. Maybe I am too influenced by the evidence emerged during the recent crisis that demonstrated there was a big methodological problem in many pre-crisis empirical econometric and statistical analyses that used too short time series to capture critical secular phenomena, still my contention is that 20 years of data is just too short to pass a definitive judgment on the €.

As mentioned at the beginning of this speech, any reasonable assessment of whether the € was a good idea or not requires also dealing with the fact that the € construction was seriously challenged since the beginning of 2010, to the point of leading many to forecast its demise. Than the relevant question is whether there was a problem with the idea itself of the € or whether there was more an issue of implementation of the idea.

As I wrote in a post I published some time ago 1, it is clear to me that there were three serious limitations in the original Maastricht design. First, financial stability, and within it banking supervision, were left basically at national level instead of being exercised, as it would have been natural in a unified monetary area, at €-area level. This aggravated a global insufficient attention to financial stability issues before the onset of the Great Recession. Second, no effective substitute tool was created to compensate for the loss of the exchange rate in handling idiosyncratic shocks, thus putting too much of a burden on the inefficient “internal devaluation” adjustment. Thirdly, insufficient progress was made in complementing monetary union with progress in other economic policy areas. This insufficiency was particularly evident in the inability to conduct at least a degree of common fiscal policy, in the absence of a public common backstop for banking crises, in the very limited progress in pursuing coordinated structural policies.

These limitations appeared in all their gravity during the Great Recession. What also emerged very strongly, however, was the political determination in all countries, in the core as well as in the periphery of the € area, to defend the € construction and remedy the critical weaknesses which had emerged during the crisis.

The result was a partial surpassing of the limitations of the original Maastricht design. On financial stability there was very important progress towards banking union, by granting supervision of the systemic €-area banks to the ECB and making progress, however insufficient, towards the objective of a common resolution regime. A common deposit guarantee scheme is still missing, however, and the prospects of it being achieved are, at best, mixed. On the issue of compensating the loss of the exchange rate as a tool to deal with idiosyncratic shock, some progress was made by creating first the EFSF and then the ESM, even if most of the burden was taken by the ECB, which fought with its unconventional actions the risk of a demise of the €. On the component of economic policy different from monetary policy, some progress was achieved with the innovations in the coordination procedures, without making, however, the decisive step towards genuine common action.

I have estimated in post I published some time ago 2 that something between two thirds and three quarters of the “Maastricht gap” has been filled during the crisis, thus only partially confirming, so far, the famous Monnet prophecy according to which European unity will be built as cumulated response to the crises that will periodically hit it. What is still missing is a completion of banking union, particularly in its resolution and deposit guarantee components, a move from trying an ever more complicated rule-based approach to fiscal and structural policies to a more decision based approach and a more forceful apparatus to deal with idiosyncratic shocks. More generally, what has been missing during the crisis was a more determined federal way of looking at issues and dealing with them, because of a misguided emphasis on an intergovernmental approach. Many, including me, think that the ECB has been overburdened with tasks during the Great Recession and it was an act of bravura on its side to rise to the challenge. It is not surprising, however, that the only federal executive institution in the €-area, endowed with an efficient decision-making and operational set-up contributed in the most effective way to deal with the crisis. This is rather an indictment of the insistence on the cumbersome and inefficient intergovernmental approach to counter the crisis: the other political €-area institutions found it much more difficult to respond quickly and effectively. Just witness the agonies of nights and week-ends necessary to achieve often half-baked solution at government level and compare them with the much smoother and efficient decision making and action of the ECB.

One can make a great compliment and a great criticism at the way political bodies have dealt with the crisis so far. The great compliment is about the determination to react to events that could have led to catastrophic events. The great criticism is about the way this determination was shown, with an obdurate insistence on an intergovernmental rather than federal approach. The main reason of the still incomplete fulfilment of Monnet´s prophecy is just the insistence on an ineffective intergovernmental approach.

In conclusion, let me summarize my points:

- The summary indications of macroeconomic welfare coming from the so called misery index do not allow to conclude whether the € was a good idea or not. Only more evidence brought about by a longer time period would allow drawing a firmer conclusion;

- The Maastricht design clearly had some serious limitations, these were partially remedied so far during the crisis but the intergovernmental approach did not allow as complete and as quick a remedy as hoped;

- Overall, my sense is that when the Maastricht design was drawn there was awareness that it was incomplete, but not that the incompleteness would have such a serious consequences as during the Great Recession;

- Still I believe that, even if the “fathers of the €” would have correctly forecast how serious the gaps were, they would still have taken the risk of creating the €, and I think I would have agreed with them.

In conclusion, my own, very personal view is that the € was a good idea and this will be proved when more evidence coming from a longer period will be available.

This post was prepared with the assistance of Madalina Norocea.

- Measure your view on the €-area: try the “Monnetomètre” [↩]

- Mentioned above [↩]