Measure your view on the €-area: try the “Monnetomètre”.

Prophecies do not normally have much to do with percentages. In this post, however, I want to try and measure in which percentage Monnet`s famous prophecy, that Europe will be built by cumulating the solutions given to recurrent crises, has been confirmed during the Great Recession. For this purpose I provide, at the end of this post, a little gadget: the “Monnetomètre”.

I participated recently to an interesting seminar at the National Bank of Belgium, organized by Kenneth Dyson and Ivo Maes on “The Architects of the euro”. The purpose of the seminar was, as Ken and Ivo wrote in their introduction, to examine the contribution of “intellectuals who had an active role in the process of designing the institutional arrangements of Economic and Monetary Union (EMU). They constitute a relatively neglected group of persons who were more than just ‘technocratic’ policy-makers. They also performed a critical liaison function between the political founders, who drove forward the EMU process and provided political legitimacy, and the ideational founders, essentially academic economists who provided intellectual ideas that fed into the work of the architects.” 1

The seminar also examined, availing itself of the information generated by the Great Recession, which were the limitations of the design that, at Maastricht, was crystallized in the eponymous Treaty, to a large extent incorporating the contributions of the “Architects”. While it is fair to say that each of the limitations of the Treaty was identified by one or the other of the Architects, none of them saw all the gaps of the Maastricht design. Nor could they foresee how acute would be the European phase of the Great Recession that, also because of the imperfect design of the Treaty, came after the American one. In addition, my guess is that they would be as surprised as me that the crisis is still affecting the €-area more than 5 years since October 2009, when the spark caused by Papandreou`s revelations about the falsified Greek deficit statistics ignited the serious disequilibria that had been accumulating since 1999.

My sense is that the gaps of the Maastricht Treaty revealed by the Great Recession can be divided in three main categories:

- Faulty €-area economic governance, both in the fiscal and structural domains,

- The maintenance of national responsibilities in banking supervision, and more generally in financial stability, in a monetary unified area,

- The absence of a tool to mutualize idiosyncratic shocks, substituting the exchange rate in this function.

Given these gaps, the most important question now is whether Monnet´s prophecy was verified during the current crisis, or whether the crisis was, so to say, wasted. To allow a non-binary answer to this question, one can formulate it differently by asking which percentage of the gaps was filled during the crisis. The answer to this question implies passing a judgment on three, intertwined, developments:

- The changes in economic governance carried out since 2009,

- The realization of Banking Union,

- The establishment of the European Stability Mechanism and the support given to the €-area periphery by the ECB.

Competent and honest people can give different guesses about the percentage to which Monnet´s prophecy`s was realized during the Great Recession. I am afraid I myself did not always give exactly the same answer 2. In any case, at the seminar mentioned above I ventured a guess that some 75 per cent of what needed to be done had been done during the Great Recession. André Sapir, also participating, to the seminar, thought my estimate exaggerated and offered a lower proportion, say 50 per cent. While I unwisely proposed at the seminar to enter into a bazar negotiation with André to agree on a percentage, in this post I want to follow a more analytical, still very judgmental, approach and examine what has been done during the crisis to fill the gaps left open by Maastricht as well as to see what still remains to be done to completely surpass them.

On Economic and Fiscal Union, as is well known, the Maastricht Treaty had written some rules that should have avoided fiscal policy mistakes. These were complemented by the Growth and Stability Pact, which however failed when it should have restrained the fiscal policies of Germany and France in 2003. From this to a general discredit of the Pact there was a short distance. The Growth and Stability Pact basically failed in its task of constraining fiscal policies into some “reasonable” boundaries, but it also revealed a, possibly more serious, flaw in its design, as it did not take into account that excessive private debt could all too easily transform itself into public debt. In addition, it did not protect against fraud, like in Greece. Beyond fiscal issues, it also appeared that excessive divergences had cumulated in economic performance because of structural deficiencies in some countries. The lack of significant growth for well over a decade in Italy and Portugal witnesses to this effect.

Table 1 summarizes the main measures defining economic governance in the €-area.

Table 1. Economic governance measures in the €-area (1998-2013)

A first way to enhance fiscal union would be to try and do more under the rubric of control and guidance of national budgets. The proposal, for instance, to have a EU financial Minister who could prevail over a national government non-complying with the common rules would be an example here. This would be consistent with the common sense principle that sovereignty ends when solvency ends. My sense, however, is that there is not much more that can be done in this area. The tension between common control and national sovereignty, however empty this concept has become in practice, puts a clear limit on what can be done in this area and, with the adaptations and reinforcements achieved during the Great Recession, I think we are at the limit. The recent decision of the European Commission to grant to Italy and France more time to fulfil their fiscal adjustment, however economically justified, reinforces this view. In addition, as argued by Pisani-Ferry and others, the experience of the crisis has shown that a purely national approach to stabilization is too weak on the occasion of a really serious crisis 3. Table 1 shows that significant innovations have been carried out during the Great Recession, complementing the Growth and Stability Pact. While I am not aware that someone has been able to provide a quantitative measure of the degree of “fiscal union” that we would need, compared with what we already have, my sense is that we already have quite something of a fiscal union, partly based on the control and guidance of national budgets, partly based on an embryonic federal approach (Community budget, ESM). I do not believe, however, that this is quite enough, even if we limit our expectations to what is needed to complement monetary union. Quantitatively we need more. Qualitatively the ad hoc, ex post and intergovernmental approach that was followed during the crisis was surely sub optimal 4 .

I believe, instead, that there is room for some incremental improvement in the area of federal budget. I find, in particular, appealing the idea to transfer, as in Pisani-Ferry and others and in an IMF paper, some highly cyclical revenue/expense from national budgets to a federal budget. The example of unemployment benefits on the expense side is an obvious one. On the revenue side, instead, taxes on firms’ profits or on real estate activity may be interesting candidates. The Juncker plan, is inspired by the same idea, but is, in my view, just too bland and episodic to really innovate in this area. A somewhat larger federal budget should not add to total (national + federal) public budget, since the federal component would substitute, not be added, to the national one, and could also be used to reinforce discipline, control and guidance of national budgets if access to federal money was conditional on respecting federal rules.

The attempt to go beyond fiscal union and promote the needed structural measures at €-area level took the form, during the crisis, of the Macroeconomic Imbalances Procedure. With its preventive and corrective component it should, on the basis of a comprehensive view of the different national economies, propose recommendations and then a corrective plan, to be implemented and monitored. The performance of the MIP so far, however, has been, to be generous, modest. Witness, as an example, its total ineffectiveness in pushing Germany to reduce its disproportionate current account surplus.

As far as the funding of national debt is concerned, putting issuance of government bonds on a federal level with a joint and several guarantee would be a complement of a €-area fiscal action and have a strong mutualisation effect: countries hit by a positive shock would implicitly lend part of their borrowing strength to countries hit by a negative shock. Unfortunately, there is no way to precisely distinguish the case in which a genuinely exogenous shock hits a country from the case in which the difficulties derive from wrong national policies. Hence the moral hazard consequences of moving to federal issuance would be gigantic unless, or until, a form of fiscal union well beyond what is now conceivable will be attained. The kind of tight fiscal union prevailing in the United States would be a model here.

The necessity to maintain a balance between, on one hand, joint responsibility and, on the other hand, joint decision-making is not limited to the extreme case of perfect fiscal union and joint and several issuance. This holds also for intermediate cases. Indeed there must always be a balance between fiscal union and common issuance. In particular I think the degree of fiscal union we have already reached would allow some small step towards common issuance, while remaining well short of joint and several issuance. The ideas abound here: the blue-red bonds of Bruegel, the issuance of €-bills, promoted by Graham Bishop, the sinking fund proposed by the German Wise-Men, the Union-bonds of Collignon, the European Safe Bonds of Brunnermeier and others are examples here. The problem is to precisely match the progress on common decision making with the move towards common issuance. Some mild form of common issuance would also support the move to federal level of some expense and revenue, as there cannot always be a perfect match between the two and borrowing may be needed to buffer temporary gaps. For instance this would be needed to transfer the unemployment benefit system to federal level in the form proposed by Pisani-Ferry and others.

As regards Banking Union, Spain and Ireland were, before the crisis, fully respecting the Growth and Stability Pact, as their budget was in surplus and their debt to GDP ratio was well below the Maastricht threshold of 60%. Where problems were brewing, however, was in the over-extended banking sector, financing an unsustainable housing boom. This showed, together with the too narrow scope of the Growth and Stability Pact mentioned above, the second limitation of the Maastricht design: the maintenance of a predominantly national approach to bank supervision. A single currency, a single payment system and a national approach to banking supervision were clearly inconsistent. The maintenance of national supervision also had the, deplorable but inevitable, consequence that national supervisors tended to act as defenders of national champions rather than as genuine supervisors 5.

Indeed as the crisis developed, the awareness grew that it would not be sufficient to move just supervision to a euro-area level, but that one would have to make big strides towards a more encompassing banking union, which comprises also a single resolution mechanism and a common deposit guarantee scheme, in addition to single supervision.

The progress achieved in the area of Banking Union over the last two years is extraordinary. We have the proof of the potency of a crisis to push towards further integration, along the lines of Bergsten and Kirkegaard. Before the crisis, the idea of common supervision, which an “Architect of the euro” like Padoa-Schioppa incessantly advocated, was ridiculed as politically impossible. Now it is hailed as an obviously needed progress. Of the three components of a fully-fledged banking union, one was nearly completely achieved (common supervision) on another (single resolution mechanism) a workable if imperfect solution was achieved, on the third one (a common deposit guarantee scheme) no progress was achieved so far 6 .

One of the conditions for an optimal currency identified by the Optimal Currency Area theory that is missing in Europe is a mechanism to mutualize idiosyncratic shocks that could hit one or another part of the euro area. The reasoning is that when a single currency is created and the exchange rate can no longer fulfil its role as shock absorber, another tool must be found to offset shocks hitting the area in a diversified way. In the United States the shock absorption is carried out by financial integration, labour mobility and transfers from the federal budget. All these factors are much weaker in the euro area and thus idiosyncratic shocks have much more negative effects.

During the Great Recession first the EFSF and then the ESM were created, under the pressure of events, to support countries in the periphery of the €-area. The ESM is an intergovernmental creature and not a genuinely federal one. In addition, the ESM does not have the nature of a budget financed by taxes and was created only ex-post to deal with the crisis, not ex-ante as an insurance mechanism 7. Yet, it is definitely part of an answer to the need to deal with idiosyncratic shocks and indeed I am tempted to define it as part of a fledgling federal budget. There is no question, in fact, that the ESM uses public money that, although indirectly, is covered by taxpayer resources. There is no doubt, either, that public money is used on the basis of political choices: helping Spain deal with the problems of its bank and providing financial resources to Greece, Portugal, Cyprus and Ireland. It should also be recognised that in the ESM/EFSF set-up there is an element of common bond issuance, as the total committed amount is higher than the maximum possible lending (the total capital is 700 billion, about 7.5 per cent of €-area GNP, while the maximum lending capacity is 500 billion), even if it remains well short of establishing a joint and several responsibility.

If it is controversial to classify the ESM in the category of federal budget, helping to deal with idiosyncratic shocks, putting European Central Bank lending in that category is close to heretical. I am myself uneasy doing this, as I value a lot the distinction between monetary and fiscal policy and am convinced that the ECB has remained faithful to its monetary policy function during the Great Recession, including with its sovereign purchasing programs: the Securities Market Program, the Outright Monetary Transactions and the Public Sector Purchase Program. Yet one cannot deny that the very large lending by the ECB, in particular to banks in the periphery, which gave rise to the famous Target2 balances, has to some extent, as a by-product of the monetary policy action, mutualised idiosyncratic shocks. The sudden stop of capital flows towards peripheral banks and countries was offset, at least in part, by very large ECB funding: at the end of 2012, the Target2 balances, which are a reflection of the liquidity support provided by the ECB, exceeded one trillion euro in aggregate and amounted, country by country, to around -50 per cent of GDP for Ireland and Greece, around -40 per cent of GDP for Portugal and Cyprus and -32 per cent of GDP for Spain. Correspondingly, creditor countries had very large surpluses. In addition, the amounts that the ECB lent were not only very large, but also very cheap: for some peripheral banks the very low interest rate charged by the ECB has been a fraction of what they would have had to pay to raise the same amounts in the private market, if they ever had indeed been able to raise them. One should also recognize that by “borrowing in the market” through the issuance of reserves and lending to banks in the periphery, the Eurosystem in a way issued common debt, as it is obvious that the ECB can issue such large amount of debt because it is supported by its own financial strength, in turn contributed by national central banks, and by some conviction that national governments stand by the Eurosystem. The same reasoning applies, at least in part, to the Public Sector Purchase Program, notwithstanding the limited risk pooling characterizing it. The critical importance of the Bundesbank and of the German Bund in supporting the credibility of the ECB as a debtor should be fully recognized here, against the view that sees the German central bank more as an obstruction than as a linchpin of the €-area. At the end, overall, while ECB funding cannot be properly said to belong to a “federal budget”, it surely shared some of its characteristics, in particular it played part of the mutualisation function that federal funds could not play.

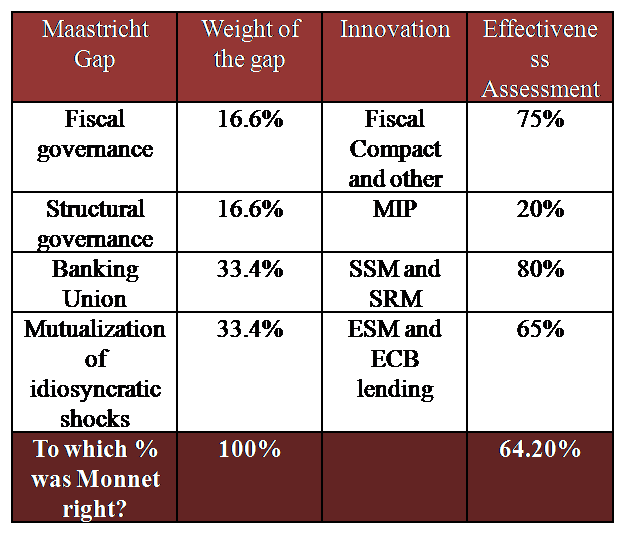

While I started this post saying that I would try and provide a quantitative estimate of the extent to which Monnet`s prophecy was confirmed during the crisis, I have so far given many words but not a single number. My attempt to transform the former in the latter is in the following table, presenting the “Monnetomètre”, i.e. a gadget to quantify one`s assessment to the degree to which the gaps in the Maastricht design have been filled during the Great Recession.

Table 2. From words to numbers: The “Monnetomètre”.

The first column of the table recalls the gaps identified at the beginning of this post, with the first one, relating to economic governance, divided in its two components: the fiscal and the structural one. In the second column the weight I attribute to the gaps is reported: here I found no special reason to weigh the main gaps differently one from the other. In the third column I summarized the innovation enacted during the Great Recession, as illustrated in the text above. In the fourth column, the most judgmental one, I reported my sense of how much of the specific gap was filled during the crisis, the percentage going from a maximum of 80 per cent for Banking Union to a low of 20 per cent for structural measures.

In conclusion, the percentage to which, in my sense, Monnet`s prophecy was confirmed, i.e. the weighted average of the effectiveness of the different measures, sums up to a bit less than 65 per cent. This is lower than the 75 per cent I shot from the hip at the conference and somewhat in the middle between that guess and that of André. After all, maybe I should have engaged in the bazaar dealing with André, as I mentioned at the conference, instead of following my more analytical attempt and I would have reached a similar conclusion. Still, having made explicit the different components is somehow useful, if anything because those not agreeing with my bottom line, could be more specific on the reason why they disagree.

One possible check on my bottom line is to assess whether what is still missing amounts to some 35% of the total. What, in my view, is still missing are the following 5 elements, with the last 2 being less important than the first 3:

- Bringing one highly cyclical fiscal revenue and expense at €-area level,

- A better governance at €-area level of structural measures,

- A limited and prudent step towards common issuance,

- A better bank resolution mechanism than the Single Resolution Mechanism and

- An €-area deposit guarantee system.

To me, what is still missing is not more than a half of what has already been done, so the 65 per cent bottom line for verification of Monnet prophecy looks right to me also from the perspective of what still needs to be done.

Still, as I said, competent and honest people can have a different assessment. André Sapir from Bruegel and Alessandro Leipold of the Lisbon Council, to whom I showed a draft of this post, would rather insist on the “around 50 per cent” guess.

André would not give more than 35 (the average between 50 and 20 for the two components of economic governance), 60 and 50 per cent respectively as estimates of the degree to which the three main gaps have been filled, validating his about 50 per cent bottom line. Alessandro identifies the continued reliance on an intergovernmental, rather than a Community, approach as the main weakness of what has been done so far. This will be particularly damaging for the SRM, which will prove unworkable when put to the test in the midst of a crisis, as he argued in a recent paper 8. As regards economic governance, Alessandro noticed that the big novelty of the innovations is supposed to be the emphasis on ex ante coordination. But not, unfortunately, coordination for the one thing that would truly matter and that would represent major progress: agreeing on an aggregate fiscal stance for the euro area as a whole 9 .

Thus, my little sample of 2 tells me that my bottom line may not be widely shared. To provide a tool to measure views about the degree to which Monnet`s prophecy has been verified I attach a usable “Monnetomètre” i.e. a little spread-sheet where one can insert his or her own weights as well as a subjective quantitative assessment of the effectiveness of the measures adopted so far, following the model of table 2 above. With the Monnetomètre each reader can calculate his own percentage of verification of the prophecy. Those readers of the post that so desire could send me their version of the Monnetomètre as comment in the blog. Should I receive an interesting number of answers I will publish the aggregate result, say in a week time.

This post, incorporating substantial input from Alessandro Leipold of the Lisbon Council, was written with the assistance of Madalina Norocea.

References:

- Céline Allard, Petya Koeva Brooks, John C. Bluedorn, Fabian Bornhorst, Katharine Christopherson, Franziska Ohnsorge, Tigran Poghosyan, Toward a Fiscal Union for the Euro Area, IMF September 2013.

- C.Fred Bergsten and Jacob Funk Kirkegaard,The Coming Resolution of the European Crisis: An update, Peterson Institute, June 2012.

- Graham Bishop, Temporary Eurobill Fund (TEF) – Summary of the Proposal and Timeline, GrahamBishop.com, November 2013.

- Markus K. Brunnermeier, Luis Garicano, Philip R. Lane, Marco Pagano, Ricardo Reis, Tano Santos, David Thesmar, Stijn Van Nieuwerburgh, Dimitri Vayanos, European Safe Bonds (ESBies), The euro-nomics group, September 2011.

- Stefan Collignon, ECB Interventions, OMT and the Bankruptcy of the No-Bailout Principle, European Parliament, Directorate General for Internal Policies, September 2012.

- Henrik Enderlein,Lucas Guttenberg,Jann Spiess, Blueprint for a Cyclical Shock Insurance in the Euro Area, Jaques Delors Institute, September 2013.

- Alessandro Leipold, Banking Union: Getting the Big Picture Right, The Lisbon Council, December 2013.

- Alessandro Leipold, Good Governance for the Euro Area: Proposals for Economic Stability, The Lisbon Council, August 2010.

- Benedicta Marzinotto, André Sapir, Guntram B. Wolff, What Kind Of Fiscal Union?, Bruegel Policy Brief, November 2011.

- Jean Pisani-Ferry, Erkki Vihriälä, Guntram B. Wolff Options for a Euro-Area Fiscal Capacity, Bruegel Policy Contribution, January 2013.

- Jean Pisani-Ferry,Guntram B. Wolff. The Fiscal Implications of a Banking Union,Bruegel Policy Brief, September 2012

- Nicolas Veron, Banking Nationalism and the European Crisis, EVCA, June 2013.

- Herman Van Rompuy, José Manuel Barroso, Jean-Claude Juncker, Mario Draghi, Towars a Genuine Economic and Monetary Union, Four presidents report, European Council of the European Union, December 2012.

- The papers presented at the seminar will be published in a forthcoming book edited by Ivo and Ken, to be published by Oxford University Press. [↩]

- In the article for the first 2014 issue of the London Business School, Business, Strategy Review I was more prudent than at the seminar, even if I did not give a precise percentage of realization, stressing that much remained to be done.[↩]

- “The limits to purely national stabilisation policy became very visible as entire economies were priced out of the market.”[↩]

- It is useful to recall here the direction indicated by the Four Presidents’ Report in December 2012 ( Accessible HERE): The Four Presidents’ Report published in December 2012 argued in favor of a macroeconomic stabilization mechanism for the Euro area. It stipulated that such a mechanism should: not lead to unidirectional or permanent transfers; not undermine incentives for structural reforms; be implementable within the framework and the institutions of the Union; not be an additional crisis-solution mechanism, but rather a complement to the ESM; not lead to an overall increase in tax and expenditure levels. [↩]

- Nicolas Veron aptly wrote about „Banking Nationalism“prevailing before supervision became the responsibility of the ECB: “This attitude can be labelled “banking nationalism” by analogy with “economic nationalism,” an expression which has become commonly used to refer to government supporting or protecting domestic corporate actors perceived as “national champions,” or undermining foreign such actors seen as champions of competing national interests, usually in contexts which involve an element of cross-border economic competition. Banking nationalism is often more potent than other forms of economic nationalism, because of the dense webs of relationships between banking sectors and governments.” Nicolas Veron, Banking Nationalism and the European Crisis, EVCA, Istanbul, 27 June, 2013.[↩]

- The missing element in supervision is that some 15 per cent of the €-area banking sector is not directly subject to the ECB.[↩]

- Enderlein and others[↩]

- Alessandro Leipold, Banking Union: Getting the Big Picture Right, The Lisbon Council, December 2013[↩]

- Alessandro Leipold, Good Governance for the Euro Area: Proposals for Economic Stability, The Lisbon Council, August 2010[↩]

Well, I am not in the mood to participate in de dealing bazaar of the Monnetomètre. Competent and honest people , as you recalled, should recognize that the so-called architects and/or decisionmakers at the time,set up a construction which was utterly fragile , if not flaw. At that time there were some critical economists who have warned but they were ridiculized by the so-called architects and/or decisionmakers.

Well, to my sense, honest and competent people should rehabilitate them. I remember some of them lost even their job!

As you could expect my reading is different. Building the € was a difficult endeavour, intellectually, politically and technically. Architects tried as hard as they could, but could not get the construction perfect from the start. Subsequent repair work, still ongoing, has been remedying the limitations of the initial construction. The “critical economists” you mention should belong to the group of “architects” to the extent that they provided critical and constructive views on how the system should be built.