What will happen on December 3rd in Sonnemannstraße?

The Bank of England has a tube station named after it and is located in an intriguingly named street: Threadneedle. The Federal Reserve Bank of New York is located in a grandly named Liberty Street. The European Central Bank, less evocatively, has Sonnemannstraße as its address. Most non Germans, and probably many Germans as well, have no idea why the street where the ECB is situated is called that way.

While the name of the street may not be evocative, something important is likely to happen in Sonnemannstraße on December 3rd, i.e. on the occasion of the next meeting of the ECB. In this post I report my expectations for that meeting.

Let me start noting that, in two aspects, the ECB is now in an analogous position to that of the FED around September:

1. Division within the decision making body,

2. Something of a contrast between decent activity and still too low inflation.

As far as the division within the council is concerned, Lautenschläger, Weidmann, Hansson, and Rimšēvičs have raised objections against further easing. However Praet and, most importantly, Draghi, have sent clear easing signals. I also put weight on the fact that the front of traditional hawks does not seem to be united, with Liikanen coming out in favour of more easing. You may recall that, in my view, Liikanen represents the needle of the voting intentions, i.e. the median voter, in the Council.

As far as the macroeconomic perspectives are concerned, the latest news on activity (in particular PMI) are decent and also credit developments are, albeit slowly, improving. However inflation remains very low, now and prospectively. At a time when the ECB seems to give more weight to core inflation, this remains stubbornly around 1.0%. If the ECB will bring down, at the next meeting, its projections for 2017 inflation to 1.5% or below, the members of the Council who want easing will have a much stronger case, as it will not be easy to pretend that inflation is getting back, over the medium term, to the level corresponding to price stability.

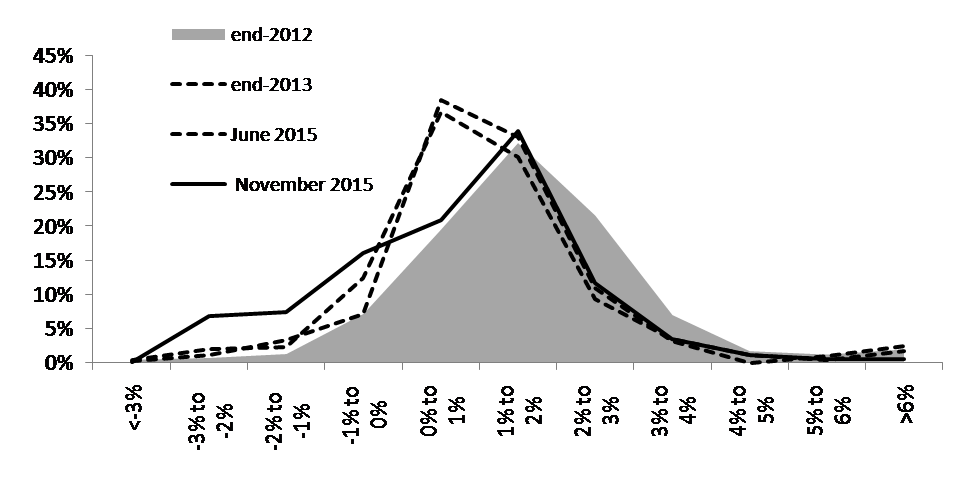

While waiting for the ECB projections, we can already notice that market based inflationary expectations are worrying. Chart 1 reports the distribution of inflationary expectations drawn from inflation swaps . What is evident is the progressive move of the median of the distribution away from the 2.00 target because of the fattening of the left tail of the distribution: in November 2015 about half of the cumulated distribution is for values of inflation of 1.00 per cent of less, at the end of 2011 only about 30 per cent of the cumulated distribution was for values equal or lower than 1.00 per cent. This indicates that financial markets have hardened their expectation of inflation not complying with the ECB objective of 2.00 per cent.

Chart 1. Distribution of inflationary expectations implied from zero coupon HICP-indexed options with 2-year maturity.

Chart 1 was prepared by Juliusz Jablecki.

Weighing on decisions of the Governing Council will also be the fact that current financial conditions and macroeconomic perspectives incorporate further monetary easing. If this would not come in the amount expected, there would be a clear, undesirable, tightening of monetary policy. So, arguing that prospects do not require further easing does not take into account that further easing is already included into prospects and if it does not come there will be an automatic tightening.

While the discussion in the Council, and then the eventual decision, will be affected by the significant hawkish minority, we should not underestimate the ability of Draghi to deliver as well as the overall willingness of the Council to decide on a majority rather than on a consensus basis.

Where does all this lead us in terms of possible concrete moves on December 3rd?

I have tried to document in a previous post 1 the small effect on inflation of a further cut of the ECB rates, indeed the effect is trivial for a reduction of 10 bp as currently included in the OIS curve. However, I do not see the Council willing to go down to Swiss levels, so I expect 20-25 basis points deposit rate cut and the MRO brought down to 0, stopping short of paying banks to give them an incentive to borrow from the ECB.

I do not exclude that, as per some leaks, the ECB could have recourse to a two-tier deposit system, indeed this could be the rabbit that Draghi could draw from his cylinder. In this system, each bank would have a cap on what it can deposit with the ECB at a less penalizing rate (say the current -20 b.p), while the excess could only be deposited at a more penalizing rate (say -40 or -45 b.p.). The question is what would be the effect of this on Eonia and, of course, on Overnight Index Swaps. My expectation is that EONIA will be attracted by the lower rate: once banks would have invested up to their cap on the less penalizing conditions, their decision, at the margin, would be what to do with the remaining liquidity and here the choice is either to deposit with the ECB at, say, -40 b.p., or to lend in the market at a similar level. This conclusion could be slightly qualified by noting that the power of attraction of the lower rate would be weakened if the size of the cap was very high. Still I believe that the more penalizing rate would be the main rate for the equilibrium in the money market.

If indeed a two tier system will be decided, an important implementation question is on what basis would the first tier caps for the individual banks be established. I see here two main options:

1. Use some indicator of bank size,

2. Use banks lending activity.

The simplest, and most likely, indicator of bank size would be compulsory reserves 2: the ECB has the relevant statistics and could easily establish the caps for all the banks that have access to its funding. If this indicator was chosen, there would be, overall, more of a problem for banks in the core of the €-area than for those in the periphery. Indeed it is banks in the core that hold most liquidity at the ECB and thus would potentially loose more because of the increased penalization of the amount exceeding the cap of the first tier.

A link between the caps for the first tier of deposits and the lending activity of a bank, so that a bank would be prized for lending by having access to a less penalizing deposit facility, would smack, in my view, of the direct controls of the 1970’s and 1980’s. Until the ECB established an analogous link in the TLTRO, I had thought that this proximity would have deterred the ECB from taking such measures, but the TLTRO has shown that the ECB has no such timidity. I thus do not exclude that the ECB may attach conditionality to its own rates, since the conditionality of the TLTRO has lost most of its power, because the demand for it has been reduced by the fact that QE is giving permanent liquidity to banks. Under this approach, the ECB would grant less penalizing deposits to banks that lend more. This solution could be less discriminating against banks in the core, depending on how the link between lending and access to the first tier of the deposit facility would be established, since banks in the core could very well have a more buoyant lending activity than banks in the periphery.

In thinking about possible time, size and scope extension of QE I think three issues are relevant:

1. The opposition of the hawk contingent in the council may be particularly strong towards further QE;

2. The experience of the US seems to indicate that the “bang for buck” of QE, say measured by reduction of yield for 100 billion of QE, wears somewhat off;

3. The time extension of QE would not be a strong measure given that the ECB has insisted on the conditionality of the program (at least until September 2016 and in any case until sufficient progress will be achieved in regaining price stability).

Given these three issues, I think the ECB will try to give some new twists to QE. So I think that:

1. They could link more closely the duration of the program to their inflation projections, for instance saying that they will continue until their projections get close enough, in the view of the Council, to 2.0%;

2. They could add some other securities (corporate and local government) to the eligible ones, just to ease the implementation of the program;

3. They could somewhat increase the size of purchases, from 60 to 70 billion per month.

On balance I think the first two changes are more likely than the third.

In conclusion, the ECB will try, in my view, to have a composite strategy that would not risk to under-deliver with respect to expectations. A cut of rates, possibly according to a two tier system, and an adaptation of QE, will likely be part of that composite strategy. However, as I mentioned in some previous posts, I would not exclude that the inventiveness of the market operation people of the ECB will produce some new idea 3.

- Will lower rates help the ECB in regaining price stability? [↩]

- Indeed a possible variant would be just to increase the level of compulsory reserves that are remunerated at the rate of the Main Refinancing Operations[↩]

- I am afraid, though, that my and Juliusz Jablecky`s pet idea of interventions in the market for inflation derivatives (A help for the ECB from the derivative market ) will not be part of the strategy. [↩]