Was the € a good idea, Mark II?

In a post I published in November 2015 (Was the € a good idea?) I asked whether the euro was a good idea or not. The conclusion of that post was that “the summary indications of macroeconomic welfare coming from the so called misery index do not allow to conclude whether the € was a good idea or not. Only more evidence brought about by a longer time period would allow drawing a firmer conclusion”. I also added, though, that “my own, very personal view is that the € was a good idea and this will be proved when more evidence coming from a longer period will be available.”

In this post I want to explore a bit further some macroeconomic consequences of the introduction of the €. In a future post I plan to deal with the more specific question of whether the € is the cause of the dismal macroeconomic performance of Italy, which needs to be surpassed to assure that Italy can maintain the € (Can Italy maintain the €? Yes, if it grows, unlike in the last 17 years.).

Since many impatient readers may not be willing to go to page 15 to find my bottom line, I give it here.

The conclusion of the post is that the introduction of the € delivered a large bonus to peripheral countries, in particular to Spain and Italy, in terms of lower nominal and real interest rates. The latter phenomenon resulted from an asymmetry between the real and the financial sector. In peripheral €-area countries the financial sector adapted completely to the change in monetary regime and brought interest rates down to the low German level. In the real sector, instead, neither private nor public behaviour adapted completely to the € and both actual and expected inflation remained higher than in the core of the €-area. In the first decade of the € Italy and Spain enjoyed the bonanza of much lower unemployment and, in Spain, higher growth. However, the oblivious attitude of policies in these two countries allowed a number of imbalances to accumulate and the bonus offered by the € was squandered. Eventually, the Great Recession can be interpreted as a painful, and thus effective, learning period at the end of which also the real sector of the peripheral economies will have adapted to the new monetary regime and enjoy the benefits of a stable currency, unlike the national ones it substituted, without creating the imbalances that characterized the first decade of existence of the €.

After all, I am still of the view that the accumulation of evidence will make clearer over time that yes, the € was a good idea, even if I am fully aware that not enough evidence has been gathered as yet to convince everybody about this conclusion.

My story starts with the so-called Great Moderation, i.e. the circa two decades, between the middle 1980s and the beginning of the Great Recession in 2007-2008, of low and stable inflation and steady growth in most advanced economies.

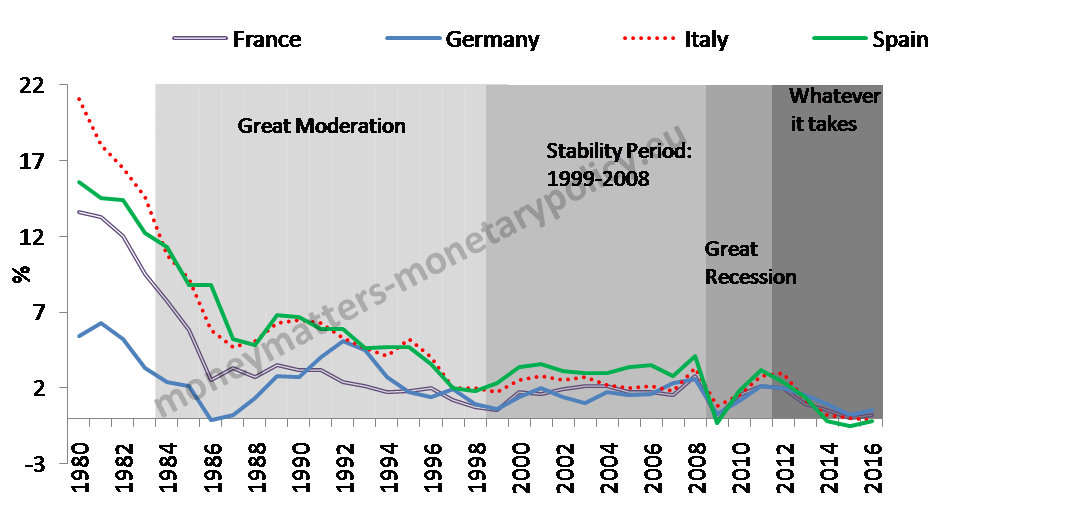

During the Great Moderation, and particularly in the second half of the 1990s before the introduction of the €, a strong and sustained decrease of nominal interest rates took place in the countries that, during the crisis, would be considered as peripheral to the euro-area. The introduction of the euro at the beginning of 1999 perfected this move. Indeed the low level of interest rates that had prevailed over a long time in the core countries with a long history of price stability, especially Germany, came to prevail all across the euro-area. This is seen in figure 1 where yields for 10-year government bonds are reported since 1980 for the four largest economies of the euro-area, Germany and France, representing the core, Italy and Spain, representing the periphery.

Figure 1. 10-Year nominal government bond yields in selected euro-area countries (1980–2016).

Source: European Commission, Annual Macro-Economic database (AMECO).

Here four different periods are clearly identified. First, there was the convergence period, which roughly coincides with the Great Moderation, starting in the early 1980s, getting more obvious in the middle of the 1990s with the prospect of the single monetary policy and eventually perfecting itself just before the launch of the € in 1999. Second, a period of stability ensued, which lasted until the autumn of 2008. During this second period, liquidity and credit premia, in addition to expected short-term rates, and thus yields, were practically the same for all €-area sovereign issuers. The denomination of this second period as “Stability Period” should not hide the fact that, as it will be seen in subsequent figures, serious imbalances accumulated while it lasted. The third period started with the Great Recession, after the failure of Lehman Brothers, and had its climax at the peak of euro-area sovereign debt crisis, in the summer of 2012. In this period yields in the periphery went sharply up while those in the core continued their downward trend. Within the Great Recession period it is useful to indicate a sub-period dated to start with the partial reabsorption of the tensions after the ECB President Mario Draghi delivered his famous speech in London in July of 2012, stating that the ECB would do “whatever it takes” to preserve the euro.

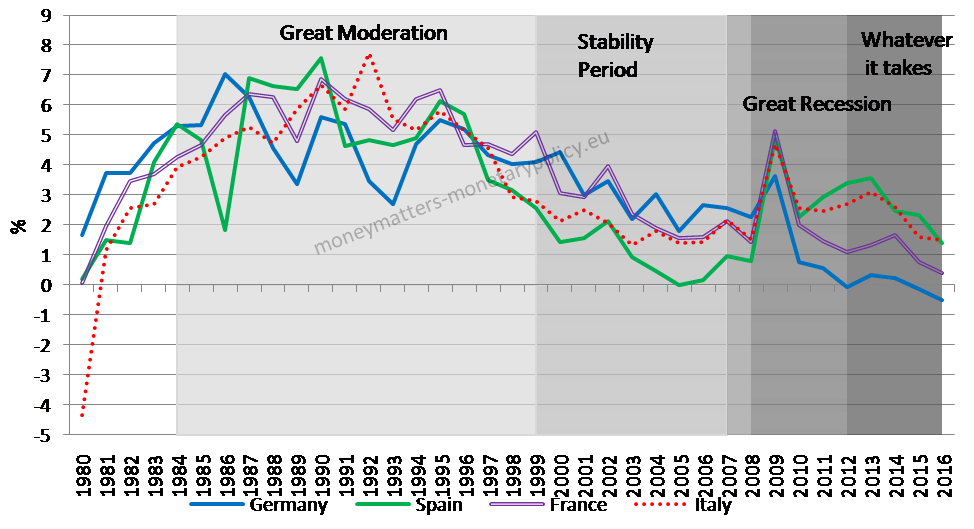

While during the Great Moderation nominal interest rates in the periphery approached those in the core and followed them lower during the Stability Period, actual inflation and inflationary expectations did not adjust to the same degree.

Figure 2 reports the inflation rates of the four selected €-area countries, showing that for last years of the Great Moderation and for practically the entire “Stability Period” inflation in the peripheral countries, particularly in Spain, was higher than in the core.

Overall it seems that not all countries were interpreting in the same way the inflation anchor provided by the ECB. Whereas the below, but close to, 2 percent indicated a ceiling for price increases in some countries, in others this looked like a floor for the annual inflation rate.

Figure 2. Consumer Price Inflation in selected euro area countries (1980–2016).

Source:OECD Statistical database

Source:OECD Statistical database

An analogous phenomenon, particularly pronounced for Spain, can be observed for survey based inflationary expectations, as reported in figure 3. In particular the light yellow shading shows the imperfect convergence of inflation expectation between the periphery (simple average of Italy and Spain) and the core (simply average of Germany and France) in the Stability Period.

Figure 3. Survey-based inflation expectations in selected euro area countries (1985-2017).

Source: own calculations based on OECD and European Commission Business and Consumer Survey.

Note: Inflation expectations refer to the one year ahead inflation rate in the respective countries, estimated from survey data.

The full convergence of nominal interest rates and the only partial convergence of inflation and inflationary expectations is consistent with an asymmetric behaviour between the financial and the real sector. The former, where interest rates are determined, adapted itself completely to the new monetary policy regime of low and stable inflation brought about by the introduction of the €, managed by the ECB. Instead the real sector in the peripheral countries, where inflation and inflation expectations are generated, adapted only partially to the euro. This result is reminiscent of the Dornbusch “overshooting” effect 1, whereby the exchange rate reacts more quickly than relative inflation and a monetary shock leads to an impact depreciation of the exchange rate that is higher than the long run depreciation, thus giving rise to a subsequent gradual exchange rate appreciation.

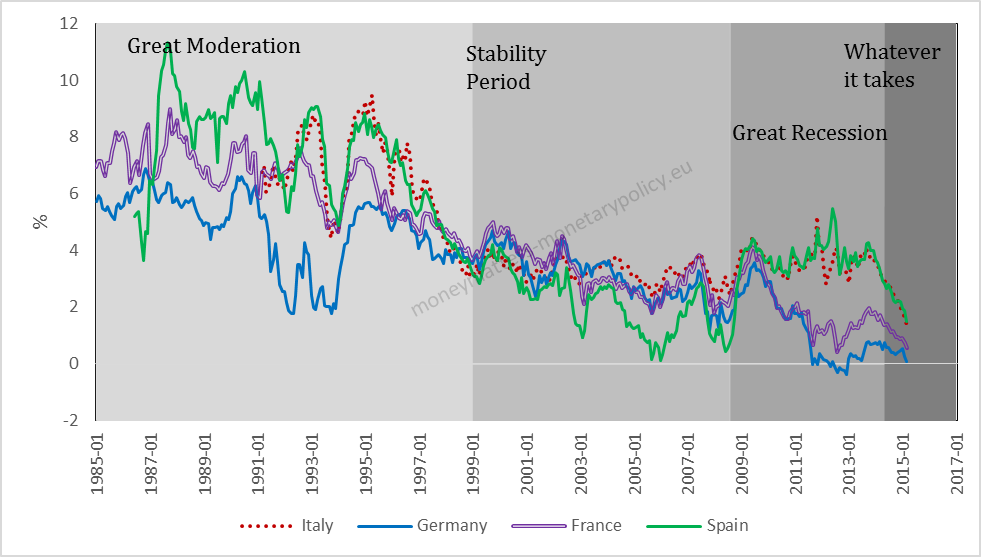

In the initial years of monetary union, the asymmetric behaviour between the real and the financial sectors determined lower real interest rates in the periphery than in the core of the euro area but then the relationship dramatically inverted during the Great Recession. This result can be seen in Figure 4: real rates of interest were much lower in the periphery than in the core of the €-area starting in the final years of the “Great Moderation” and during the “Stability Period”. With the beginning of the “Great Recession” a dramatic inversion occurred and real rates in the periphery surpassed those in the core. Both the lowering of the real rate during the Stability Period and its jacking up during the Great Recession was more extreme in Spain than in Italy: for instance in the former country, the real rate moved from close to 0 in 2005-2006 to 3.6 per cent in 2013.

Figure 4. Real interest rates calculated from consumer prices, selected countries (1980 – 2016).

Source: European Commission, Annual Macro-Economic database (AMECO).

Source: European Commission, Annual Macro-Economic database (AMECO).

An analogous phenomenon can be seen in figure 5, where real interest rates are calculated using estimates of inflationary expectations.

Figure 5. Real interest rates calculated from estimated expected inflation rates, selected countries (1980 – 2016).

Source: own calculations based on OECD and European Commission Business and Consumer Survey. Note: the real rates are calculated ex-post, subtracting one-year ahead inflation expectations at time t from the nominal interest rates at time t.

In this chart the case of Spain stands out, with real rates lower than in the core countries for most of the stability period. The case of Italy is, instead, mixed.

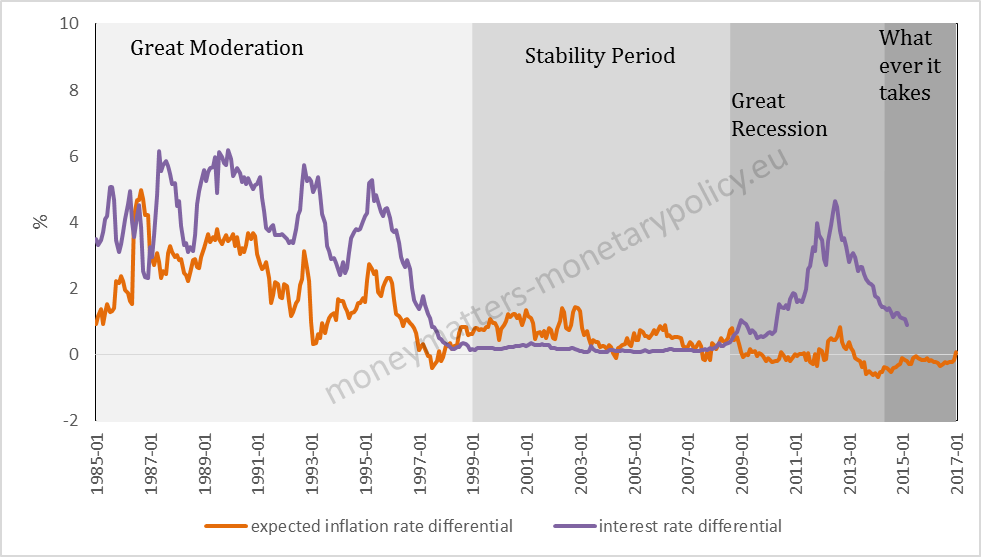

A synthetic view of the different behaviour or inflation and interest rate differentials in the core and periphery of the €-area can be seen in figure 6.

Figure 6. Differentials of expected inflation and 10-year government bond yields between periphery and core of the euro area.

Source: own calculations based on OECD and European Commission Business and Consumer Survey. Note: both the expected inflation and the interest rate differential are calculated as the difference between periphery (simple average between Italy and Spain) and core (simple average between Germany and France).

In figure 6 on sees quite striking developments. In the periphery the interest rate differential was higher than the expected inflation differential in the Great Moderation and in the Great Recession periods. However, the relationship inverted in the Stability Period, roughly corresponding to the first decade of the €. Another way to look at this behaviour, is to observe that the real rate of interest was always higher in the periphery than in the core with the only exception of the Stability Period.

This is also seen in table 1 reporting over three periods (1985-1997, 1998-2008 2, 2009-2016), the average ten year yield, inflation expectations and real interest rates in the periphery and in the core. The evidence in table 1 confirms that there was practically full interest rate convergence between the periphery and the core of the € area since the introduction of the €, while the convergence of inflation expectations was less than perfect. Hence, unlike in the previous period, real rates of interest were lower in the periphery than in the core during the “Stability Period”. During the Great Recession/Whatever it takes period, as also shown in table 1, there was instead practically full convergence of inflation and inflation expectations between the core and the periphery, but interest rates diverged again, with those in the periphery significantly higher than in the core.

Table 1. Average ten-year government bond yield, average inflation expectations and average real interest rates (%).

| 1985-1997 | 1998-2008 | 2009-2016 | ||||

| North | South | North | South | North | South | |

| Ten year yield | 7.7 | 11.6 | 4.4 | 4.5 | 2.4 | 4.3 |

| inflation expectations | 2.0 | 4.0 | 1.1 | 1.7 | 0.9 | 0.8 |

| real interest rates | 5.7 | 7.6 | 3.2 | 2.8 | 1.5 | 3.5 |

Source: own calculations based on OECD and European Commission Business and Consumer Survey.

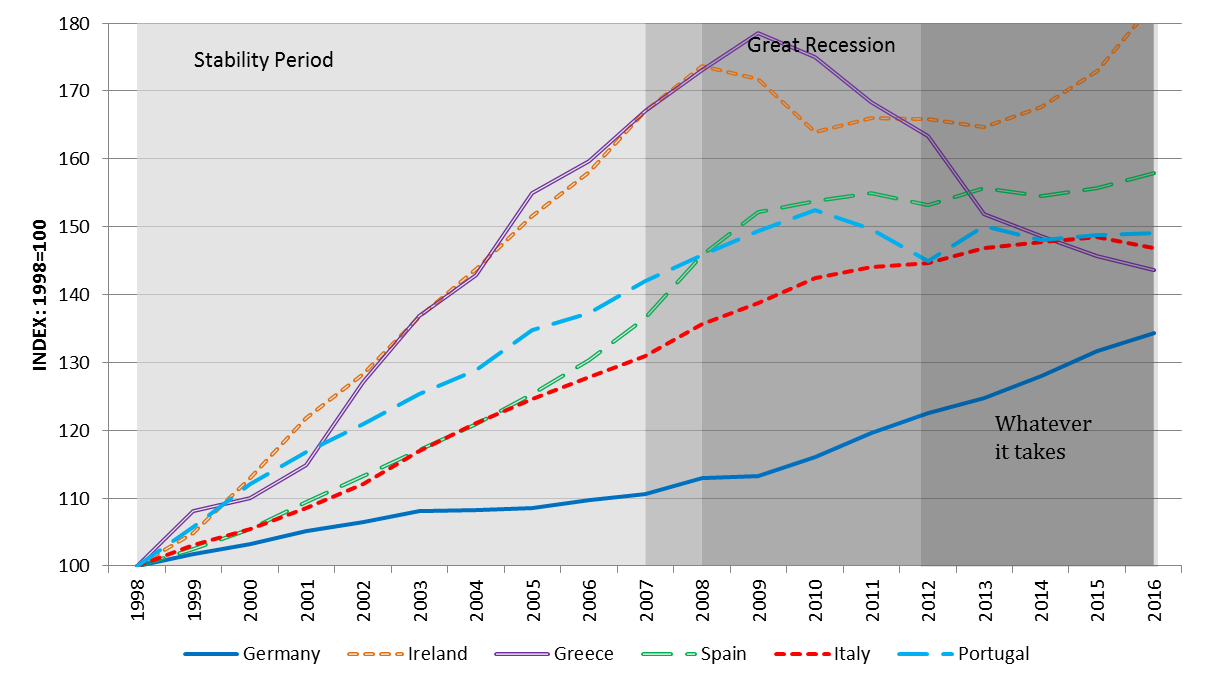

The higher inflation, actual and expected, in the periphery in the “Stability Period” was also visible in wages, which grew much faster than in the core, as seen in Figure 7. In the early years of the single currency, a decade after its unification, Germany was seen as the sick man of Europe 3. The German government reacted to this situation with a number of structural reforms, particularly in the labor market. After the so called Hartz reforms 4, it seemed natural that inflation and wages in the periphery, affected by the inertia in adapting to the new monetary regime introduced by the euro, would exceed those in Germany. As a consequence, too little attention was paid to the loss of competitiveness in the periphery, which was getting substantial on a cumulative basis. This was aggravated by a wrong emphasis on real wages, where higher inflation seemed to compensate for the competitiveness loss from higher wages. This was however the wrong perspective in a monetary union where the common exchange rate could not reflect national inflationary differentials. Only after the beginning of the Great Recession was there a partial convergence between wages in the periphery and those in Germany, as wages in the peripheral countries mostly stabilized or decreased and wages in Germany began to climb more significantly.

Figure 7. Compensation per employee in euro-area countries, index 1998=100 (1998–2016).

Source: European Commission, Annual Macro-Economic database (AMECO).

The loss of competitiveness in the periphery contributed to large current account deficits that worsened until the onset of the Great Recession, when they were sharply corrected, as seen in Figure 8. The developments of savings imbalances between the core and periphery in the euro-area resembled those taking place between the US and China.

Figure 8. Current account balances in euro-area peripheral countries, as per cent of GDP (1980-2016).

Source: IMF World Economic Outlook.

With the onset of the Great Recession, the private capital flows from the core that had easily funded the current account deficits, since the euro had eliminated exchange rate risk, “suddenly stopped” 5 .

In some countries of the periphery, namely Italy, Greece, and Portugal, the fiscal stance further contributed to the large current account imbalances. This occurred because the favourable effect of the lower cost of public debt due to lower interest rates was not sufficiently exploited to correct fiscal imbalances, as seen in Figure 8.

The fiscal correction took place during the Great Recession, once the focus of the crisis shifted to Europe, but only after the recession and the decision to bail out banks brought about a huge aggravation of fiscal imbalances. It was only since around the middle of the 2010s that fiscal balances in the periphery climbed closer to zero.

The inertia in lowering inflation and inflationary expectations in the periphery may have also contributed to fiscal deficits, as governments may have continued expecting that inflation would eat into the real value of debt, thus reducing its burden.

Figure 9. Budget balances in euro-area peripheral countries, as per cent of GDP (1980 – 2016).

Source IMF Economic Outlook and European Commission – Annual Macro-Economic database (AMECO).

In Greece, Portugal and, to some extent, Italy, the excessive credit took the form of large public deficits and, eventually, debt as well as large external borrowing and debt. In some other countries, namely Ireland and Spain, the fiscal balance fully respected the Maastricht criteria at the onset of the Great Recession, with average deficit clearly below 3.0 percent and the debt-to-GDP ratio lower than 60 percent. Only large current account deficits indicated excessive demand. However, somewhat similarly to the situation in the US, real estate prices increased sharply, with house purchases and real estate projects being financed by bank lending. The low level of expected real rates fed the demand of funding to purchase real estate and supervisory policy either did not see this problem or just did not care about it. Thus household debt increased sharply. In Ireland and Spain excessive debt took the form of heavy external borrowing and large indebtedness by the domestic private sector. This, however, duly transformed itself into public debt during the crisis, when governments bailed out the banks with public funds.

Overall, the interpretation provided above, based on the asymmetry between the financial and the real sectors of the peripheral economies, is quite powerful, because it can help explain a number of features in the shift from the “Stability Period” to the “Great Recession”: the dramatic inversion of the relationship between real interest rates in the periphery and the core, higher wages in the former group of countries up to the Great Recession, the deterioration and then the improvement of current account balances, the behaviour of budget deficits, the real estate boom and the heavy private sector indebtedness in some peripheral countries, eventually also the strong increase of non performing loans in the peripheral countries.

The same interpretation also lends itself to a happy-ending prognosis: the Great Recession would have offered a very painful and thus effective learning experience to the peripheral countries, forcing them to adapt also inflation and inflationary expectations to the stable monetary policy of the European Central Bank, as the memory of the less stable monetary policies of their national central banks fades in the past. This conclusion is consistent with the fact that inflation and inflation expectations in the periphery no longer deviated from those in the core since the beginning of the Great Recession, as was seen in figure 2 and 3 and in table 1.The phenomena observed in the circa first two decades of the € should thus be interpreted as a una tantum, painful, learning period.

It is useful to see whether the interpretation line offered so far also helps to explain growth and unemployment behaviour. As seen below, this looks the case more for Spain than for Italy.

The lower real interest rates in the periphery between the second half of the 1990s and the beginning of the Great Recession, brought about by the asymmetric reaction of the real and the financial market to the introduction of the €, should have buoyed up growth and reduced unemployment. However, the growing current account deficits in most peripheral countries indicate that part of the additional demand brought about by lower real rates spilled over abroad, under the guise of higher net imports.

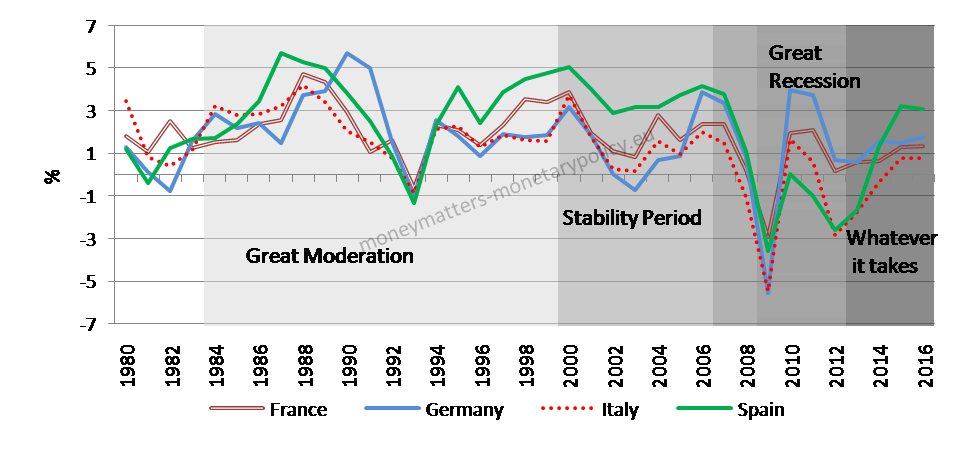

Figure 10 reports the end result of these contrasting developments, as well as those of the myriad other factors influencing growth and unemployment.

Figure 10. Growth rates of selected €-area countries.

Source: OECD Statistical database

Source: OECD Statistical database

Here the experience of Spain fits very well the interpretation offered above, while that of Italy matches it only imperfectly. In Spain one can find the effect of low real interest rates in a growth rate significantly higher since the mid 1990’s than in the two core countries. Subsequently, the impact of the Great Recession was, not surprisingly, stronger in Spain than in the core and only around the middle of the 2010s did growth in Spain surpass again that in Germany and France. In Italy, instead, growth remained for most of the period between the mid 1980s and the beginning of the Great Recession lower than in the other 3 countries. During the Great Recession growth came further down in Italy, with only a limited recovery since 2012. Overall stagnation in Italy is to be measured in decades more than years and looks more a structural phenomenon than one heavily influenced by changes in real interest rates. However, as I mentioned above, I will address the specific case of Italy in another post.

Figure 11. Unemployment rates in selected €-area countries.

Source: IMF WEO.

The unemployment rate tells a similar story. Spain achieved a spectacular reduction of unemployment in the last years of the Great Moderation, with the prospect of € adoption, which continued in the Stability Period. Then during the Great Recession a dramatic worsening occurred, with only a partial recovery since 2012. In Italy there was a sustained reduction of the unemployment rate after the adoption of the € and until the Great Recession, during which it about doubled, with only a partial recovery in the last few years. The unemployment rate was much more stable in the core countries and only since 2005 did it come down significantly in Germany, but not in France.

This post is an excerpt of a book Tuomas Välimäki and I are writing for Oxford University Press, Central Banking in Turbulent Times, which should be published in the autumn of this year.

This post was prepared with the assistance of Pia Hüttl and Madalina Norocea.

- Rudi Dornbusch, Expectations and exchange rate dynamics. Journal of political Economy, 1976. Revisited by K. Rogoff, Dornbusch`s Overshooting Model After Twenty –Five Years, IMF Working Paper. February 2002.[↩]

- The stability period is made to start in 1998, since by that time the approximation oft he € had already led to a perfect alignment of interest rates.[↩]

- The Economist, June 3rd 1999, The Sick Man of the euro.[↩]

- The Economist, November 17th 2004, Germany on the mend.[↩]

- S. Merler and J. Pisani-Ferri (2012), Sudden stops in the euro-area. Bruegel Policy Contribution, 29 March 2012.[↩]

I will respond in more detail, but there are reasons to doubt if nation wide average wages are a good indicator of competitivety (they are a good indicator, however, of consumption leading to additional imports…): https://www.worldeconomicsassociation.org/newsletterarticles/ulc/