Satisfaction On The Banks Of The Main

Some readers have told me that they find my titles a little cryptic, so let me start by explaining the title of this post.

The Main is the river crossing Frankfurt and the impressive new building of the European Central Bank is just over the banks of the Main. So the sense of my title is that I perceive a general message of satisfaction coming from the European Central Bank, which claims for itself much, indeed a bit too much, of the merit for the positive developments it notices. I see, however, in ECB utterances also some factors that suggest caution: first, the Greek situation; second, the meagre prospects about long term growth; third, bond price volatility; fourth, exchange rate developments. I expect the satisfaction as well as the factors of caution will come out clearly from the forthcoming press conference of Draghi

Let me first briefly address the sense of satisfaction and then the reasons for caution.

The first reason of satisfaction is the clear improvement in the short-term outlook. I would not do much of the fact that at 0.4 per cent in the first quarter of 2015 growth was higher in the €-area than in the US and the UK, -0.70 and 0.30 per cent respectively. One quarter data is too fragile an evidence to build upon it a significant story. Still the fact is that, at long last, the €-area seems to have moved away from the stagnation in which it languished for a long period. On inflation the progress is less obvious and it is not granted as yet that inflation will return towards 2.0 per cent, as projected by the ECB for 2017. Still the deterioration of inflationary expectations has been stopped and some progress back towards price stability has been achieved, as shown by the five year in five year inflationary expectations derived from inflation swaps. Too early to claim success, but less ground for despair.

Chart 1. Inflation expectations ( 5y,5y fwd)

Source: Barclays live

A second reason of satisfaction is that bank lending, as I illustrated in a previous post 1, is showing signs of recovery, arguably also as a consequence of ECB action, including the Comprehensive Balance Sheet Assessment and all the monetary policy measures taken by the ECB, culminating in QE.

The smooth progress in the implementation of QE and its desired effect on financial variables, especially because of the portfolio balance effect, is a third reason of satisfaction. Coeurè has recently argued, contrary to some market commentary, that the ECB sees complementarity between QE and the negative deposit rate. Furthermore, he added, ECB purchases have not bumped into non-price-elastic sellers, at least as yet. In addition, there is less of a risk of an ever-tighter constraint on ECB purchases coming from a growing share of sovereign bonds yielding less than the negative 20 basis points of the deposit facility rate. What I also notice is that the guerrilla against QE in the Council seems to have subsided. The tone in the last “Monetary Policy Accounts”, as the ECB quasi minutes are pedantically called, was one of strong support for the current policy course, with little echo of opposition. Weidmann and his allies could surely have asked for a minority view to be represented, but I hardly found a trace of it. 2 Maybe the hawks realised that their strident opposition was not justified. Let me note, en passant, that by opposing measures that turned out to be useful the Bundesbank may have jeopardized its long term influence in the Council, thus weakening its needed support for a sound money in the ECB.

Let me now come to the four reasons for caution.

Over a short horizon, the most worrying issue is Greece. I have given in a previous post 3 my subjective assessment that, possibly after having gone through the shock of capital controls and other emergency measures, there is a two thirds probability that Greece will remain in the €-area and I stick by that guess. Still the process is excruciating: Greece finally has to deliver, creditors are waiting for it to do so. What I do not understand is that the issue of contention is the fiscal stance: I think that Greece needs structural measures, especially in the product markets to improve its competitiveness, more than another dose of fiscal tightening. Let me note in addition a disagreement between the recent Financial Stability Review of the ECB and some market observers. The former stresses the risks that could come from Grexit, the latter argue, instead, that the €-area should be relatively immune to shocks coming from Greece. I think that this is one of the few cases in which ignorance is a good thing: I do not want to find out who is right. However, if the worse comes to the worse and Greece shows no willingness to take the necessary measures, Grexit, with all its risks, will have to be accepted.

Over a longer time horizon, the biggest worry is the prospect of a long period of anaemic growth: the €-area economy grew for a long period before the Great Recession at a nearly 2.5 per cent pace, not exciting but acceptable. Now a pace of 1 per cent is already ambitious and without higher growth the two grave stock problems affecting the €-area economy, unemployment and debt, cannot be properly addressed. The alarmed speech of Draghi in Sintra 4 sends a clear strategic message in this respect. I read into it, however, also a more subtle tactical message addressed to both the hawks, who say that the ECB is doing already too much, and to those who would want the ECB to do even more: the ECB has done a lot and there is little more that it can do. For the long term problems of the €-area economy the monetary policy tool is ineffective and inappropriate, structural reforms are essential, even more on product rather than labour market, because of the different demand impact.

On a much lower scale, I also take the volatility of bonds as another element of caution for the ECB. The question is whether the jerks of Bund prices which appeared at the end of April were a one off event, possibly connected to uncertainty about the implementation of QE, or they have to be read as a repetition of the crash of Treasuries of October 2014. If the two events are an indication of a structural dearth of liquidity affecting two of the most important bond markets in the world, than a serious analysis of the causes is needed. An important fact in this respect is stressed by the ECB Financial Stability Review: the lack of liquidity is affecting the bond market more than other critical markets, like the equity market for blue chip companies and the foreign exchange market for major currencies. So the causes must be found in some specific characteristics of the bond market. If you listen to some bankers, the cause of illiquidity is regulation, prohibiting banks to take positions and thus act as buffers in the market. Even if the source of the argument is suspicious, as banks are logically against stringent regulation, it is worth examining it with care.

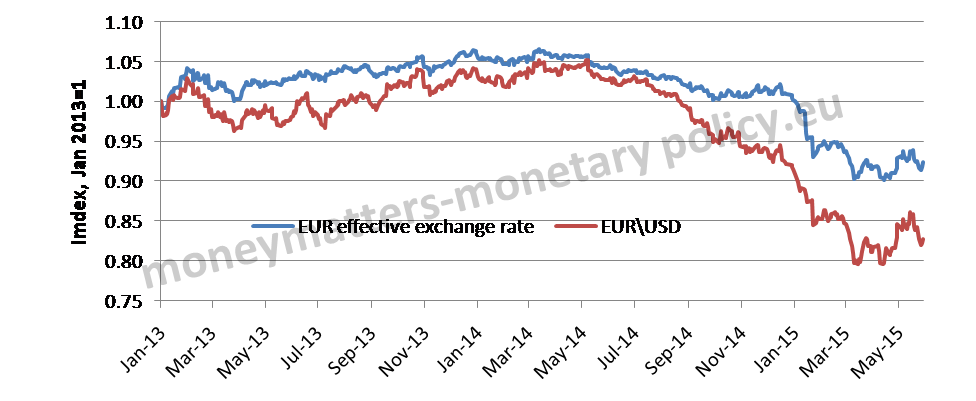

What I see as last, and least, element of caution for the ECB is the recent € Exchange appreciation. This I put last and least essentially because of quantitative reasons: the appreciation is too modest to really raise much apprehension. This can be seen in the following chart reporting the exchange rate of the € both against the dollar and in effective terms.

Chart 2 : EUR exchange rate ( effective vs. USD)

Source: ECB SDW

There one sees that the recent appreciation against the dollar has undone only a small fraction of the change in the opposite direction since mid May 2014. One also sees a confirmation of the bias implicit in looking at the dollar-€ rate instead of the more meaningful effective exchange rate. The two differ quite significantly because there are currencies, like the pound, the Swedish krona and the Swiss franc, that are quite important for €-area external trade and tend to follow the € against the dollar, providing a “ballast effect” to the effective exchange rate of the €. My rule of thumb is that the elasticity of the effective exchange rate of the € to the dollar-€ rate is about 0.5. Indeed over the last 12 month the exchange rate of the € has depreciated by 19% against the dollar but only by 11% in effective terms. Another measure to assess the lower variability of the €-effective exchange rate with respect to the exchange rate against the dollar is to calculate the ratio of the two relative standard deviations: since 1999 this ratio is 0.57. So, the worst that can be said, from the ECB perspective, about the recent appreciation of the € is that it is not welcome.

In conclusion, one can understand both the sense of satisfaction hovering over the banks of the Main as well as the reasons to be cautious. Indeed it would be surprising if the ECB would incur in the mortal sin of central bankers: complacency.

Madalina Norocea provided assistance in preparing this post.

- Bank credit supply is improving in the €-area [↩]

- The only, faint trace of a lack of unanimity in the manifest satisfaction about the current policy course of the ECB is to be found in the “Overall” word that starts the following quotation from the Monetary Policy Accounts: “Overall, members agreed that emphasis needed to be placed on a steady course of monetary policy with a focus on the firm implementation of the Governing Council’s recent monetary policy decisions. The Governing Council therefore reaffirmed its intention to conduct purchases until the end of September 2016 and, in any case, until a sustained adjustment was visible in the path of inflation consistent with the Governing Council’s aim of achieving inflation rates below, but close to, 2% over the medium term.”[↩]

- My take of what could happen between Greece and its creditors[↩]

- “ … the short-term impact of structural reforms does not just depend on when they are implemented, but how – namely, the credibility of reforms, the type of reforms and their interaction with other policy measures. And if structural reforms are well-designed along these parameters, they can in fact have a largely neutral, if not positive impact on short-term demand – and even in adverse cyclical conditions.” , Draghi, ECB Forum on Central Banking Sintra, 22 May 2015[↩]