Dissecting the hawks of the ECB

In this post I want to examine what are the nature and the basis of the opposition of some members of the Governing Council of the ECB to Quantitative Easing (QE).

Let´s start with two unanimous agreements, signed by hawks as well as doves in the Governing Council:

- “If needed” there should be recourse to other unconventional measures;

- “The balance sheet is expected go back where it was in March 2012, increasing by about 1 trillion €”.

There are therefore two crucial issues to be examined:

- Are new unconventional measures already needed or should one wait for worsened conditions?

- What is the basis for expecting that indeed the balance sheet of the ECB would increase, without the need of additional measures, by 1 trillion €?

A literal reading of the different statements by the ECB hawks shows that there is no absolute opposition to additional unconventional measures, which I take to be a clumsy paraphrase of QE, but rather doubts about their effectiveness and, most of all, the judgment that they are not yet needed in current circumstances. A few statements suffice to show this:

Bundesbank President Jens Weidmann “rejected the notion that the ECB’s Governing Council needed to swiftly adopt additional unconventional monetary policy measures in the form of a quantitative easing package. Given the rather modest and uncertain impact of a broad QE package, together with the risks and side-effects it could bring and the unclear need for it at present, I would greet such a package with scepticism at this time,…” (emphasis added) [Speech delivered at Club of Frankfurt Economic Journalists, 17 of December 2014; available Here]

ECB Board member Lautenschläger said: “Long-term interest rates on Spanish and Italian government bonds, for example, are already lower than those from the U.S. or the U.K. It is therefore questionable whether we should ‘depress’ interest rates for the securities class even further. …Even if it is good to be prepared, one should beware of showing activism,…In any case, we’d have to wait three, four, five months to be able to judge the impact of existing stimulus”. [Speech delivered on 29 of November 2014; Source Bloomberg]

An analogous idea was expressed by some members of the Executive Board that are not generally considered as hawks, but with a clear difference of emphasis as regards the timing with respect to the hawks. Thus, last June Benoit Coeure said about QE: “It is possible, it is in the toolbox, but it isn’t needed today.We’ve been clear that in case inflation would be too low for too long, we can use additional instruments, including additional non-standard measures. But we’re not in that situation today.” [ 20 of June 2014; Source WSJ] . But some 5 month later Coeure gave a different sense of the timing, while not showing unconditional enthusiasm for QE: “There is a large consensus on the Governing Council to do more and we are now discussing the instruments to use,… [but ] there is no guarantee that what worked in the US or Japan can be reproduced identically with us.… We must think for ourselves, based on the economic, financial and institutional specifics of the euro area. It is this reflection which is underway and which may resolved quickly.” [16 of December; Source L’Opinion Magazine]

Vice President Constancio also mentioned the need to wait a while longer before having recourse to QE, but definitely over a more precise and arguably shorter horizon: “We expect that the adopted measures will lead within the time of the programme, the balance sheet to go back to the size it had in early 2012,… We have, of course, to closely monitor if the pace of its evolution is in line with that expectation. In particular, during the first quarter of next year we will be able to gauge better if that is the case. …If not, we will have to consider buying other assets, including sovereign bonds in the secondary market, the bulkier and more liquid market of securities available.” [26 of November 2014; Source FT]

The question whether more measures are needed or not now is easy to answer in the neat framework of the ECB: is the objective to keep inflation lower but close to 2.0% in the medium term respected or not? Of course, there is a degree of flexibility in the definition of the ECB objective, how many years is a medium-term long? 1 And does the length of the medium term change depending on conditions? As we have no way to answer these questions in abstract, let´s try and measure how far in the future must the “medium term” be stretched for price stability to be regained.

One way to do this is to see when one year breakeven forward inflation gets back to 2%. I.e. calculate for any year starting with 2015 and going forward as far in the future as possible when one year breakeven inflation will approximate 2.%.

Another approach is to calculate how long an average inflation starting with the actual data of 2013 would have to be for it to approach 2%. I.e. starting with a two year average for 2013 and 2014, then moving to a 3 years average adding the one year breakeven inflation for 2015, then a 4 year average adding the inflation forward for 2016 and so on, when would an average close to 2% be reached, if ever? The two approaches are presented in Chart 1.

Chart 1. Break-even forward inflation: yearly values and progressively longer average.

Source: Barclays Live

The blue bars represent actual inflation in 2013 and 2014 and break-even one-year-forward inflation for successive years until 2028. Here we see that it is only around 2022 that the yearly rate of inflation is expected by the market to get back below but close to 2.00%. This approach quantifies in 8 years the “medium term” included in the ECB inflation objective, which is not within my (and I guess most people´s) definition of “medium term”.

The red bars report the average inflation over a progressively longer period of time: the bar for 2013 gives the actual inflation for that year, the bar for 2014 the average over 2013 and 2014, the bar for 2015 the average over the three years to 2015, with the last year represented by break-even inflation for that year, and so on. One sees that not even in 2028 the average rate of inflation approximates 2.00%. Another way to put the same result is that for the 16 years between 2013 and 2028 the average inflation is expected not to reach even 1.5%, which is not, in my view, close to 2.00%.

Yet another test is to look at long term inflation forecasts by economists (Professional forecasters, Consensus forecast and Economic forecasts). This is done in chart 2.

Chart 2: Inflation forecasts

Source: ECB, Consensus Economics, European Commission, IMF

Inflation forecasts cannot be extended beyond 2016 but price stability is not approached in the shorter period they cover.

The conclusion on this first point is that the prospect of inflation getting back to the ECB objective is very far into the future, well beyond any reasonable definition of “medium term”, indeed over a time horizon where forecasting errors make any projection close to useless. Thus the conclusion that the ECB should wait further before taking additional measures is not justified and the “wait a while longer” conclusion of the hawks is not empirically founded. In a post published in March of last year I argued that inflationary expectations had already moved from being firmly to weakly anchored 2. Now the situation has clearly worsened and further waiting is not justified.

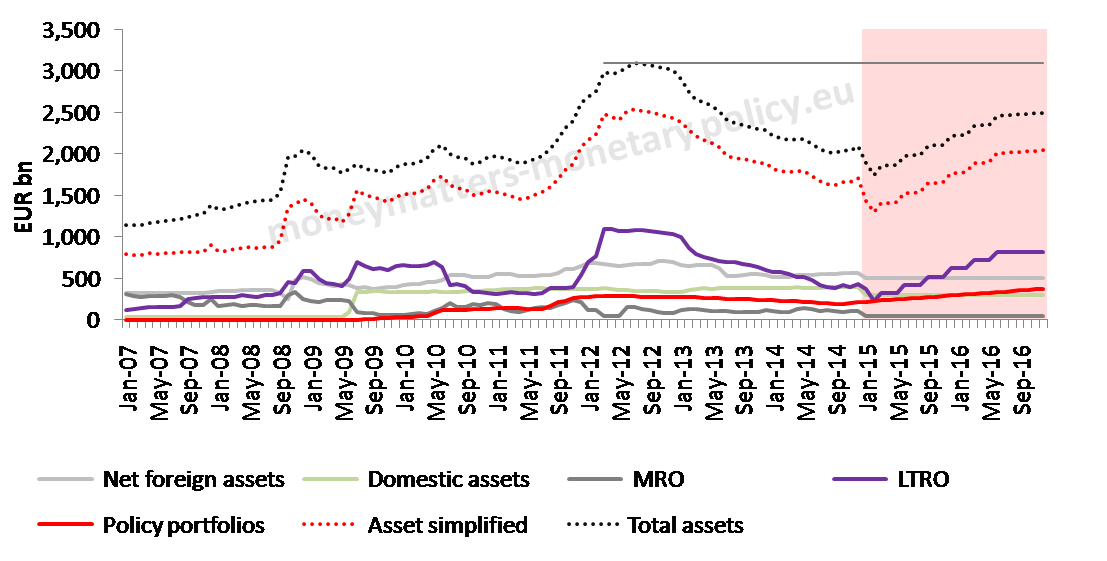

As for the second argument put forward by the hawks, that the balance sheet is expected to get back to March 2012 (even if they do not agree that this is “an intention”), an analysis of current measures and trends (ABS and Covered bonds purchases, TLTRO, reimbursement of 3 Y LTROs, possible reduction of other repo operations) is needed to project forward the balance sheet. This is done in Chart 3 on the basis of the assumptions listed in the Annex.

Chart 3: ECB balance sheet forecast

Source: ECB, Authors’ calculation

The result of the exercise shows that current trends are much short of the “unanimous expectations”: my estimate is that only about half of the “expected” trillion increase is likely without the help of QE.

My overall conclusion is that neither the argument that one should wait further before taking new measures to comply with the ECB price stability objective nor the expectation that the balance sheet of the ECB will reach back the level of March 2012 find empirical support. Then, the reader may ask, what is their logical basis? I am afraid I do not find one and I am left with the worrying thought that they are based on ideology more than reasoning.

ANNEX

The following assumptions were made for the forecast of the ECB balance sheet to the end of 2016:

The total monthly policy portfolio changes are the sum of the below mentioned figures:

• The policy portfolios account has been changing because of maturing assets on average by -4 bn EUR per month, from the end of CBPP2 to the start of CBPP3 ;

• The ABS purchases so far are at 0.7 bn EUR on average per month;

• The CBPP3 purchases are at 10 bn EUR on average per month;

The LTRO account:

• Next tranches of TLTROs are in March, June, September and December 2015 and in March and June 2016. These bring about increases by an average of 100 bn EUR, corresponding to the average of the first 2 TLTROs.

• For January and February 2015 the 3 year maturing LTROs outstanding were subtracted.

The Net foreign and Domestic assets were considered constant, the USD repo as well as the Marginal Lending Facility and the Fine tuning operations are considered null, the MRO assumed to be 50 bn EUR.

Simplified Assets vs Total Assets

The Simplified Assets are the sum of the above mentioned accounts. The average difference of the two accounts between 2007 and 2014 was added to the Simplified assets to forecast the Total assets.

Table 1: Forecast of various accounts of the ECB balance sheet

Source: ECB, Authors’ calculations

Madalina Norocea gave assistance in preparing this post.

- In a previous post I showed that only averaging inflation over a period longer than what is normally understood to be the medium term could one conclude that the stabilization of prices by the ECB has been precise enough[↩]

- From firmly to weakly anchored, or the importance of an adverb![↩]

Is at the start economy not ideology? Why are some believers of the “free market hypothesis” and others more of State intervention? What to think about the different lecture the BIS and the FED and the ECB have about the actual crisis and the remedies.I feel sorry to say that it is the BIS who “predicted” sooner the financial crisis of 2008 and not the the FED nor the ECB.