Galileo Galilei and the €-crisis

Legend says that when Galileo Galilei exited, on the 22nd of June of 1633, from Santa Maria sopra Minerva, in Rome, where the Catholic church held a process against him, he pronounced the famous sentence: “And yet, it moves”, referring to the fact that, contrary to the view of the then majority of people, it was the earth that moves around the sun and not the opposite. Since that day, the case of Galileo Galilei has become the archetypal case to demonstrate that the majority, even when supported by a strong institution such as the catholic church, is not always necessarily right.

I did not carry out a precise quantitative study, but my sense, somewhat supported by the anthology of statements I reported in a previous post [Who said what on the euro?], is that a majority of observers thought, until some time ago, that the € crisis could only have a catastrophic end. One or more exit, from above (Finland?) or from below (Greece?), the entire undoing of monetary union, epidemic defaults were some of the forms the catastrophe could take.

Get me right. The conclusion that the € crisis will not end in a catastrophe is not yet as sure as the fact that it is the earth that circles around the sun and those who held the view that the crisis would not necessarily end in ruins were not geniuses like Galileo. It is too early to proclaim victory on the €-crisis and relent on the effort, set backs are still possible. Still, the majority has clearly changed view and the central scenario does not foresee a ruinous end any more. I find it useful to understand two things: first, what led to the changed prospects; second, why so many people made, what now seems, a wrong forecast.

The change of view only came after an extraordinary battery of remarkable and, to many, unexpected developments:

1.Instead of coming down, the number of countries using the € has further increased to 18, with the adoption of the single currency by Latvia, from the original 11;

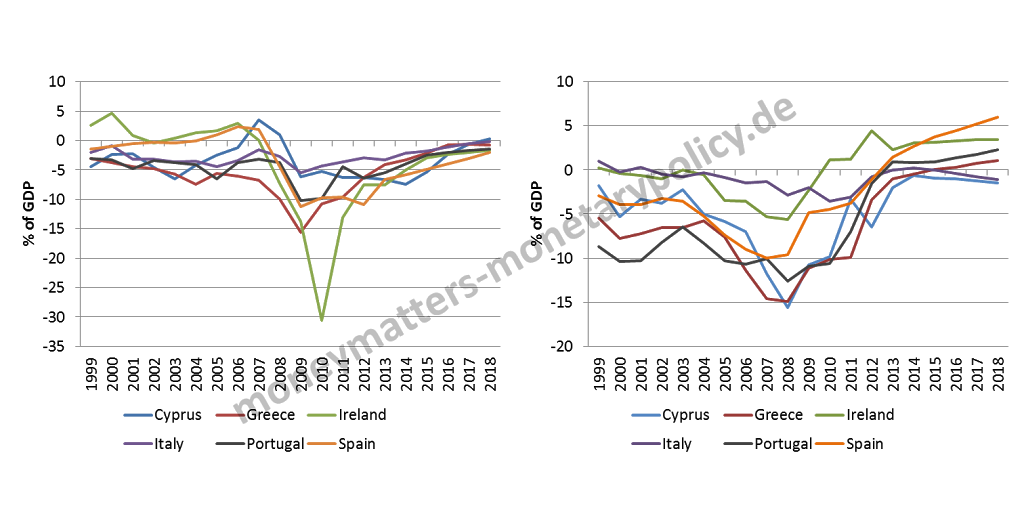

2.All peripheral countries, Spain, Italy, Portugal, Greece, Ireland, Cyprus (See Chart 1) have moved from current account and budget deficits towards equilibrium or into surplus and are regaining competitiveness;

3.Economic recovery is taking place, admittedly with a subdued pace, in the entire €-area;

4.The absence of a mechanism mutualising idiosyncratic shock was, at least partially, remedied during the crisis by inter-governmental financial support, like the European Stability Mechanism, and by the funding provided by the European Central Bank to peripheral banks through its refinancing operations [1];

5.The European Central Bank has avoided an illiquidity induced epidemics of banking defaults and vigorously fought financial fragmentation;

6.Extraordinary progress is being achieved on banking union; while those who insisted on the need of single supervision in the €-area were considered until recently “Pie in the Sky” idealists, now everybody applauds the progress on banking union, with two out of its three components, single supervision and single resolution, being implemented;

7.Rating agencies notice structural progress in program countries [2];

8.Improvements have been achieved in economic governance in the €-area, learning from the limitations and the design flaws of the Growth and Stability Pact;

9.Ireland has exited with flying colours from its adjustment program [3];

10.Spain has exited from its program targeted at rehabilitating Spanish banks, has never lost market access and is paying the lowest cost since February 2006 for borrowing on a 10 year maturity on the market [4];

11.Portugal is close to exiting its program (foreseen for mid 2014) and has regained market access, albeit only partially so far;

12.Greece has seen a stock exchange revival with the ASE index posting the highest level since mid 2011 while Greek PMIs is the highest since August 2009, consistently with forecasts of the beginning of a recovery in 2014 [5];

13.The IMF-EU program in Cyprus is progressing better than planned [6];

14.Italy´s cost of borrowing on a 10 year basis to fund its mammoth debt is the lowest since January 2006.

Source: IMF WEO, Oct 2013

1.From an institutional point of view, the Troika approach, with the IMF, the European Commission and the ECB dictating policies to program countries was, to put it blandly, cumbersome [7];

2.Program countries, on their side, were often slow and timid in recognising the need for correction of their policies, too often the evident difficulties were attributed to the lack of support from the rest of Europe rather than to their obvious policy mistakes;

3.On the economic policy side, in hindsight too much, too quickly was done on the fiscal front and too little, too late on the structural side;

4.Institutional innovations were borne with great difficulty, at the end of long drawn processes;

5.The unemployment situation is bad in the aggregate of the €-area and dramatic in most of the periphery;

6.Debt prospects are heavy for both the public and the private sector in many countries;

7.The rehabilitation of the banking sector still has to go through a challenging “Comprehensive Balance Sheet Assessment” from the ECB and the European Banking Authority.

In addition, all the progress was sort of disguised for very long time by the appalling style with which it was enacted: action seemed always to be late, reactive, forced by events rather than rationally chosen, acrimony between creditors and debtors reached peak levels, brinkmanship reigned. As I advanced in a previous post [Hurray, a crisis!] this was not by chance: surpassing the crisis required cessions of sovereignty and therefore it could be done only if it proved essential and only if others players in the game would also be willing to cede sovereignty [8]. This required an iterative, untidy process and the delays, the quarrels, the posturing created a fog which made it very difficult to many observers, probably the majority, to see the progress that was going on under the surface. One of the prices of the brinkmanship approach was that both markets and public opinion were presented with a distorted, more negative picture of what was happening and this, in itself, prolonged and made the crisis more serious. In conclusion, while it is fair to say that an amount of brinkmanship was unavoidable, there was far too much of it in the managing of the €-crisis.

So, my answers to the two questions I put at the beginning of this post are the following: first, the forecasts about the outcome of the crisis were only changed when progress in dealing with it became so obvious that it could not be ignored any more; second, the wrong forecast of many observers derived from the fog created by the brinkmanship approach in dealing with the crisis.

To go back to Galileo Galilei, the majority of people at his time could not see, beyond the appearance, that it was the earth moving around the sun and not vice versa. Similarly, the appalling style with which the €-area dealt with its crisis made it difficult to see the determination of the Europeans to defend the €, the most advanced form of their progress towards unity. Only overwhelming evidence eventually forced a change of mind.

——————————————————————————————————-

Francesco, a thoughtful post as always. It seems to me that the Eurozone is in a race. On one hand, they are moving slowly to make the currency area more optimal and resilient. Yet on the other hand, the currency is itself creating a problem for many of the economies who are mired in a slow growth scenario. I’m personally not convinced yet that the Eurozone will win its race: http://bit.ly/1e9ifrm.