Common evil, lesser evil? Mal comune, mezzo gaudio?

The Italian proverb in the title says that if a problem affects everybody, it is less of a problem. In this post we want to check, through some very simple empirical analysis, whether the problem with price stability engendered by too low inflation is really common to four jurisdictions: the US, the €-area, Japan and the UK. The bottom line is that this is not the case.

The variables to be considered for this exercise are the following:

- Current headline consumer inflation,

- Current core consumer inflation,

- Breakeven inflation for a five year period in five year time (so called 5y5y breakeven inflation),

- Medium term inflation forecast by the relevant central bank.

The variables in point 2 and 3 will be considered also correcting the bias introduced into them by the very low oil price[1].

Table 1 Various inflation indicators, latest available data.

| Variable | United States | €-area | Japan | United Kingdom |

| Headline Inflation | 1.25 | -0.15 | -0.01 | 0.20 |

| Core Inflation | 1.67 | 0.83 | 0.70 | 1.11 |

| Corrected Core Inflation | 1.76 | 0.94 | 0.89 | 1.21 |

| 5y5y Breakeven Inflation | 1.89

|

1.46

|

0.81

|

1.95* |

| Corrected 5y5y Breakeven Inflation | 2.05 | 1.63 |

0.91

|

2.05* |

| Central bank Projection** | 1.9-2.0 | 1.6 | 1.85 | 2.1 |

Data refer to February 2016 for the euro area and US (except for core inflation) while for Japan and UK (as well as US for core inflation) they refer to January 2016.

*Breakeven inflation in UK is calculated using the RPI. Data in the table are based on the assumption of a 1.3% wedge between RPI and CPI.

** Projections are provided by the respective Central Banks and refer to 2018 for the Euro area, US and UK and to 2017 for Japan.

Source: see appendix.

The comparison between the different jurisdictions is facilitated by the fact that the four central banks have, in practice, the same definition of price stability: 2.00%. Looking at the 6 variables, it clearly emerges that the United States and also the United Kingdom are quite close to their objective, indeed, by €-area standards, one would say that price stability prevails in them. The same cannot be said about the €-area and, even more, Japan, where there is quite a distance between current and expected inflation, on one side, and the price stability objective, on the other side.

This consideration only partially matches the different monetary policy prospects in the 4 jurisdictions. In particular in the US and the UK it is not easy to understand, looking at the inflation situation and prospects, the angst about raising rates and a clearer prospect of firming policy rates seems to be justified: price stability is approximately achieved in both countries and in the US also the unemployment rate is at the long run equilibrium estimate. Of course, one could have a different reading of the inflation prospects. For example, in the case of the FED one may want to give more weight to the downward direction in which the break-even inflation is moving, as evidenced in figure 1 below. In addition, there is more than inflation in the information set that a central bank considers to calibrate monetary policy. In the case of the UK it is likely that the prospect of Brexit is weighing on the Bank of England willingness to increase rates. Still, prima facie evidence is that, unlike in the €-area and Japan, price stability is broadly achieved in the US and the UK.

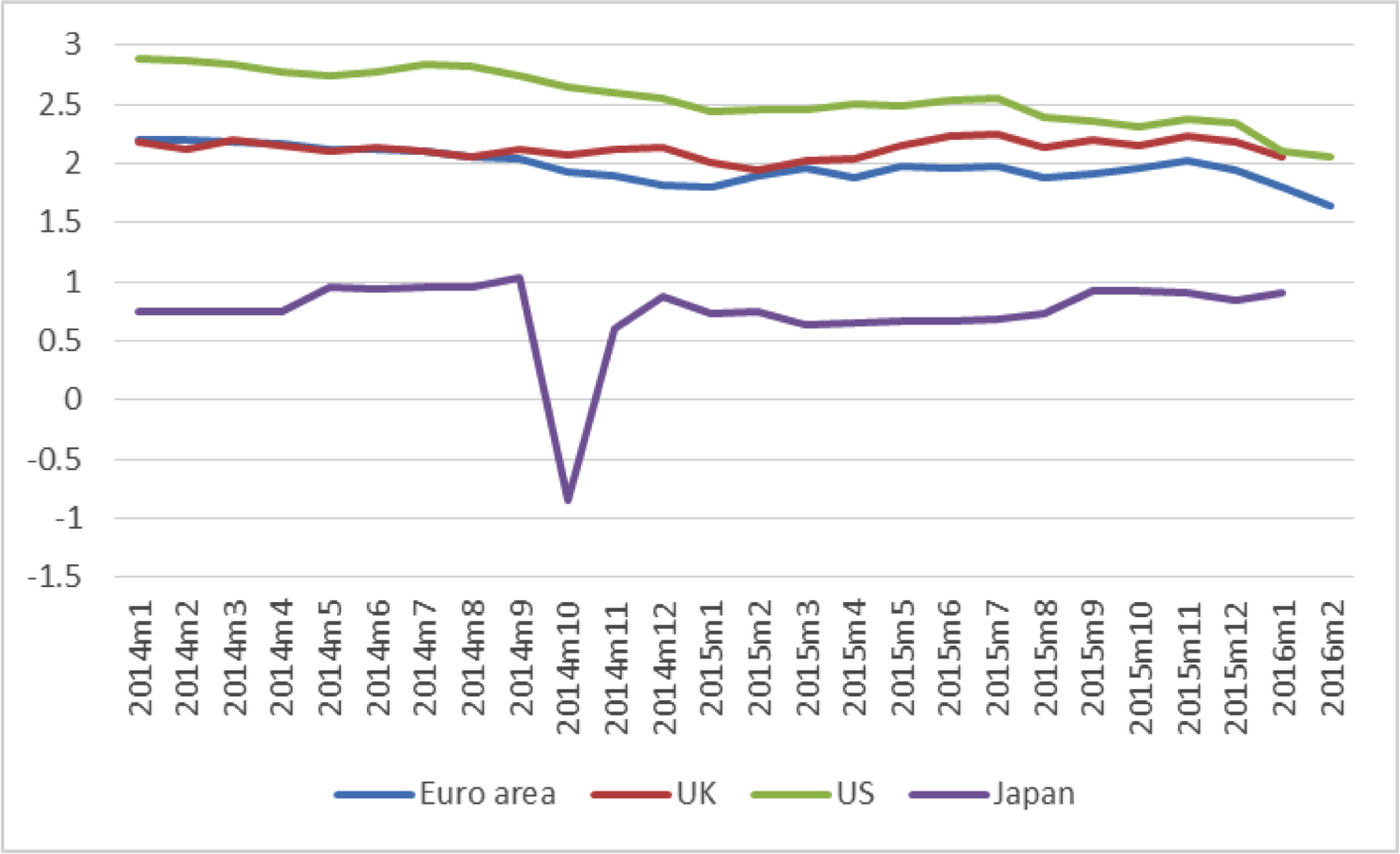

Figure 1 reports the time series of the corrected 5y5y breakeven inflation that shows that in the US and the UK the rate of inflation implied by the financial market, while coming down, is still close to 2.0 per cent, while it is quite lower than that in the €-area and, even more, in Japan.

Figure 1. Corrected 5y5y breakeven inflation

Source: own elaboration on Eurostat, OECD, Datastream, Statistics Japan

Source: own elaboration on Eurostat, OECD, Datastream, Statistics Japan

This post was jointly written by Francesco Papadia and Piero Esposito. Comments of Fabio Noacco, Senior Strategist at Mediobanca, are gratefully acknowledged.

Appendix

The correction of core and breakeven inflation to take into account the effects of movements in energy prices is based on a Phillips curve style equation as in Darvas (2016, see footnote 1). For core inflation, we use a dynamic specification where regressors are the lagged dependent variable, the lag of the output gap and the lag of energy inflation. The latter is measured by the energy component of the index used to measure core inflation. The resulting specification is the following:

(1)![]()

Where πcore is the core inflation, OutGap is the percentage gap between actual and potential GDP and πenergy is the energy component of the price index. For the euro area, United Kingdom and Japan, we use the core version of the Consumer Price Index, which is the variable on which the respective Central Banks measure the inflation target. For United States, we use the Personal Consumption Expenditure index, which is the relevant measure used by the Fed to assess price stability.

As for the correction of breakeven inflation, we rely on a slightly different specification:

(2) Where E(π5y5y) is the long run breakeven inflation expectation, that is the 5 years ahead expectation for the inflation rate in the following 5 years. This measure is derived from inflation-indexed swaps.

Where E(π5y5y) is the long run breakeven inflation expectation, that is the 5 years ahead expectation for the inflation rate in the following 5 years. This measure is derived from inflation-indexed swaps.

In both equations, the correction is obtained by subtracting from the dependent variable πenergy multiplied by the estimated ϒ.

The choice of the specifications (1) and (2) is based on a trade-off between the stability of the coefficient for energy inflation and the number of regressors in the equation. In equation (1) the use of the first lag only is sufficient as additional lags are not significant and do not change significantly the impact of energy inflation. In equation (2), the lagged dependent variable is excluded whereas four lags of the output gap are introduced because of their high significance. This means that hysteresis in economic conditions play an important role in the formation of long-run price expectations.

The estimates are carried out on monthly sample covering the period from January 1999 to February 2016. Data are collected from different sources. For the Euro area and UK, headline, core and energy inflation rates are measured by the HICP provided by Eurostat. For the US, we use the PCE index provided by the Federal Reserve. For Japan we use the CPI provided by Statistics Japan. As monthly measure of output gap, we use the ratio of trend to smoothed GDP calculated by the OECD. Finally, the 5y5y breakeven inflation expectation are collected from Datastream. In the case of UK, inflation linked swaps use the Retail Price Index whereas the BoE measures price stability in terms of consumer prices. In order to convert expectation on the RPI into expectation on the CPI we assume a 1.3% long run wedge between the two measures, as estimated by the BoE.[2]

[1] The correction of the bias of break even inflation for the €-area was presented in the post written with Guntram Wolff on March 2nd 2016: Central banks: From omnipotence to impotence? (http://bruegel.org/2016/03/central-banks-from-omnipotence-to-impotence/). The correction for the bias in core inflation was presented in the post by Zsolt Darvas: Has ECB QE lifted inflation? Of January 12th. (http://bruegel.org/2016/01/has-ecb-qe-lifted-inflation/).

[2] See Bank of England, “Inflation Report”, Febrary 2014. Available at http://www.bankofengland.co.uk/publications/Pages/inflationreport/2014/ir1401.aspx