…and what about the other side of the pond?

While on this side of the Atlantic the ECB was reacting more quickly than expected to the much weaker inflation prospects, I was in the US trying to better understand what is happening over there in the monetary area.

On the basis of the talks I had, I came back with a number of thoughts, which were not necessarily shared by my interlocutors but were stimulated by the discussions I had with them.

These cover: the exit from über-loose US monetary policy, the still strong headwinds that are supposed to persist until 2016, the conclusion that the interest rate is still the most important monetary policy tool and indicator, the question whether the recurrent fiscal fights in Washington are affecting the $ as an international currency. At the end, I also add short comments about the integrity of financial markets and Abenomics that came incidentally during my US talks.

These cover: the exit from über-loose US monetary policy, the still strong headwinds that are supposed to persist until 2016, the conclusion that the interest rate is still the most important monetary policy tool and indicator, the question whether the recurrent fiscal fights in Washington are affecting the $ as an international currency. At the end, I also add short comments about the integrity of financial markets and Abenomics that came incidentally during my US talks.

Exit from über-loose US monetary policy

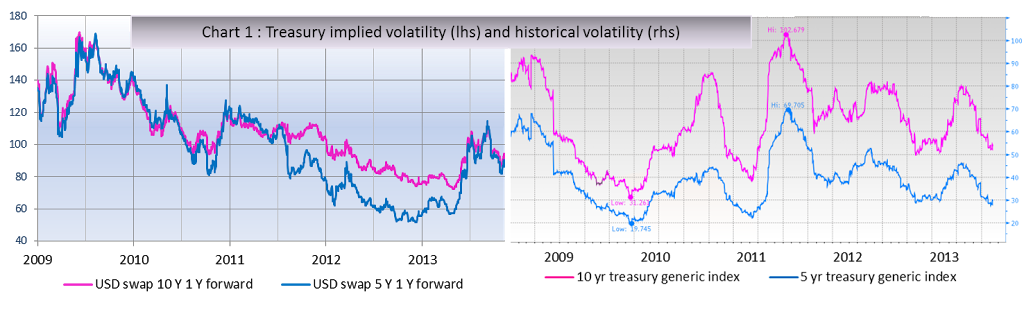

My overall conclusion here is that the gradual exit from the exceptionally easy American monetary policy will be more volatile than commonly believed. To be more precise (or just pedantic?), I think the (option derived) current Implied Standard Deviation of Treasury yields prices is too low and the episode of higher volatility observed around the tapering/no tapering episode in May-September is more an anticipation of what could happen than an occasion to close excessive open positions. Given the importance of the Treasuries market, the increased volatility could spill over to the foreign exchange, the short term interest rate and the equity markets.

|

| Source:Bloomberg |

The reasons for this conclusion are, in my view, the following:

1.The transition to the new FED Board, and in particular to the new Chair, will carry some uncertainty. While quite a lot is known about the dovish inclination of the Chair designate, Ms. Yellen, the correlation between her future behaviour as Chair and her past behaviour as deputy chair will be definitely less than 100%.

2.The market confusion about tapering/non tapering is, basically, due neither to inept communication from the FED nor to inability of the market to understand it but rather to the objective difficulty of exiting from such an exceptionally long and intense period of monetary ease.

3.The fact that, faced with the medium term uncertainties derived from the fiscal dysfunction in Washington, the FED prefers erring on the side of ease.

4.My concern that linking monetary policy to unemployment carries obvious medium term risks, given the noisy relationship between the two, just think of the risk of wrong assumptions about the participation rate and NAIRU.

5.The ability of a central bank, be it the FED, the ECB or any other, to control long term interest rates is more limited than currently markets assume; I am still of the traditional view that the control of the central bank decays along the yield curve, being very good at very short maturities and weaker and weaker as maturity lengthens.

These factors of worry are mitigated by two factors:

1.Current inflation is low in the US.

2.Inflationary expectations are still well behaved, given the past control of inflation by the FED and I do not think the FED would really want to take serious risks in this domain. So, there is little sign that inflation is a risk for the foreseeable future.

On balance, I cannot exclude the risk of a disorderly increase of yields as in 1994.

Still strong headwinds in 2016

As it is well known, in its September Press Conference, the Chair of the FED reported the view of the Federal Open Market Committee that, while inflation will be in 2016 at its target level (around 2.0%) and there will be full employment (with unemployment around 5.5%), interest rates will be only at 2.0%, a half of their long run level, and thus real rates of interest will still be about zero. He also added that: “I imagine it would take a few more years after that to get to the 4 percent level. I couldn’t be much more precise than that—I mean, we’re already obviously stretching the bounds of credibility to talk about specific projections to 2016. But I think you would expect to see that rates would gradually rise for the two or three years after 2016 and ultimately get to 4 percent.”

The Chair justified this surprising projection on the basis of three headwinds: the slow recovery in the housing market, the risk of a continuing fiscal drag and, possibly, the lingering consequences of the financial crisis. Of course, the Chair cautioned against giving to much weight to the projections for 2016. Still, they give a strong sense of the policy intentions of the FED: the very easy monetary policy will have to prevail well into the medium run.

I must admit that I am not confortable with the projection of zero real rates 7 years after the peak of the crisis and with “headwinds” so persistent that they are still felt until 2018 or 2019. As I said, inflation does not seem to be a risk in the US, but I do not think it is warranted to take inflation as dead. Inflationary expectations have been disciplined by the crisis and, most of all, by an appropriate monetary policy from the FED, but they are not constant by nature: appropriate maintenance is needed, especially over a medium to long term horizon.

Unlike me, the market is utterly comfortable with the FED projection of low interest rates for much longer. The Primary Dealer Survey, regularly conducted by the New York FED, shows that market participants expect that rates will remain extraordinarily low. Their median expectation for the Federal Funds Target rate was, in the September Survey, 1.50 and 2.50 % for the end of the first and second half of 2016 respectively and, at 3.50%, still lower than the long run value of 4.0% at the end of 2017. I take this as the result of a combination of two factors in the mind of market participants: inflation developments that do not require higher rates and the ability of the FED to steer a very gradual increase of rates over time. The reasons behind this overall assessment are not very clear to me, but the market seems to be fully convinced about it.

The interest rate is still the most important monetary policy tool and indicator.

The importance attached to the tapering/no tapering question between Summer and Autumn of this year could induce many to think that balance sheet management has become more important than interest rate management as a monetary policy tool. I remain convinced of the contrary and nothing I heard during my trip in the US led me to change my mind. Indeed the preparations of the FED to better manage interest rates, when this will be necessary, by extending the number of institutions which will have access to its reverse repo operations to reabsorb, as needed, excess reserves, is, in my view, a proof that this is also the view of the FED.

It is true that first the tapering and then the no tapering announcements created quite some commotion in the market, but this was, in my view, because the market took them as indications about interest rate changes, notwithstanding the efforts of the FED to separate any slowing down in purchases from any indication about interest rate increases. An “experiment” to validate the interpretation that tapering is more important as a signal about rates than in itself will take place if the FED will start its tapering and, at the same time, revise downward its 6.5% unemployment threshold or introduce an inflation threshold (say 1.5%), whereby it would not raise rates at least until unemployment will have gone down to the lower threshold and inflation will remain lower than the new threshold. With such an articulated move the tapering should be deprived of any signal about interest rate increases and should, therefore, have no or only muted effect on Treasuries yields.

Are the recurrent fiscal fights in Washington affecting the $ as an international currency?

The mechanism through which this could happen is that international reserve managers and sovereign wealth funds, which are very risk averse and slow moving investors, may start to be uncomfortable holding a predominant share of their reserves in a currency subject to shocks of political nature.

Two questions arise in this respect:

1.Is such a phenomenon taking place?

2.Is yes, what is its importance?

The view with which I crossed the Atlantic and that I checked with my interlocutors is that there could be indeed be such a phenomenon, but its effect would be as mild as persistent.

I was presented with different considerations on this topic. One first consideration is that the practical, mostly unintended, effect of the Republican vs. Republican vs. Democrats stalemate is a correction of the budget deficit of the US, which should reassure dollar holders. Another consideration was that there could be a limited negative effect, but this would be trumped by an underlying strength of the dollar, determined by the undoubtedly good growth of the US economy. A third consideration is that reserve managers and sovereign wealth funds are engaged in a long term diversification effort that could just receive a fillip from the difficult fiscal process in Washington. Finally, the point was made that any diversification away from the dollar is limited by the dearth of real alternatives: of course, there can be some move into the euro, which is the second largest international currency, and into smaller currencies, like the Pound, the yen, the Canadian and Australian dollar and so on. But all of these currencies cannot absorb huge reserve diversification. This means that the move could be relatively small for the dollar but more important for the currencies into which diversification would occur, probably complicating their management.

When in the US, I also confirmed two other thoughts:

1.The investigations that are now starting on possible improper behaviour in the foreign exchange market will consolidate, after the many and serious improprieties and frauds that have been uncovered in other areas, the view in public opinion that the financial market wholly lacks integrity. The long-term implications of this, in terms of regulation and willingness of fiscal authorities to act as a backstop, should not be underestimated.

2.Until, or unless, Abenomics third arrow is developed well beyond the Trans Pacific Partnership and the host of minor measures now considered, its ultimate success is uncertain.