What went wrong with Greece?

The immediate answer to the question in the title is that what went wrong in Greece was the inability of Greece and its creditors to agree on a continuation of the lending program, which has led to the current very tense situation. Indeed, while both sides had clear and strong reasons to agree, the result, unless there will be a welcome yes at the forthcoming referendum, is that there will be no agreement, with the prospect of Grexit quite higher than the 1/3 I guessed in a post on April 22nd 1.

In this post, however, I want to find a different and more fundamental reason of the failure. I will do this by first presenting what are, in my view, the economic contours of the failure and then giving my assessment of why the adjustment program was so much less successful in Greece than in other “troika countries”.

There are two graphic ways to illustrate the failure of the Greek adjustment program: one is of a “time series” nature, looking at the progressive deterioration of the Greek economy, the other is of a “cross-section” nature, comparing Greek failure with the other troika countries: Ireland, Portugal, Cyprus and Spain.

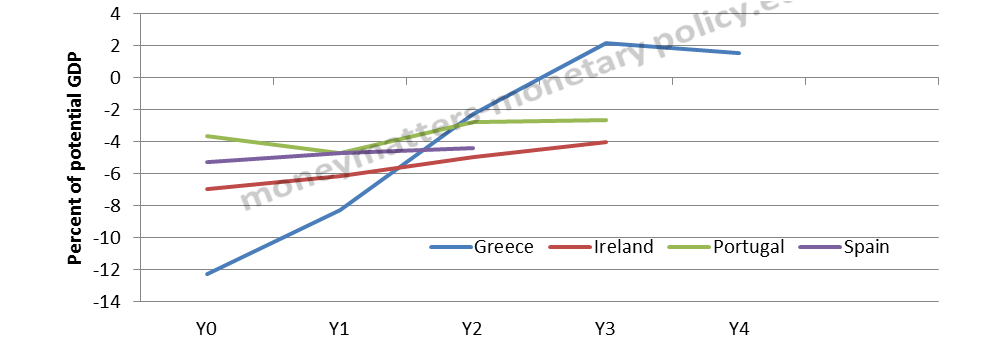

Chart 1 presents “time series” evidence, showing how the forecasts about the GDP loss in Greece during the adjustment programs were progressively downgraded: in the first program a loss of income lower than 10 per cent was expected, in the latest program a loss of one quarter of GDP was recognized. It is worth recalling that no advanced economy had anything like this kind of loss since World War II and that to find losses of such order of magnitude one has to go to war experiences: Italy and Germany, for instance, lost 26 and 62 per cent respectively of their GDP between 1939 and 1946 2. Alternatively, one must compare Greece with emerging economies, in which losses of the same or even larger magnitude have been recorded 3. Indeed some observers would rather put Greece in the emerging rather than in the advanced economies category.

While recognizing that the uncertainty connected to the fact that Greece was the first country to enter into a troika program may have played a role, a program that has led to such a level of loss cannot be characterized in any other way than as a failure.

Chart 1 Changes in Greek GDP forecast in different vintage programs

Source: IMF WEO estimates

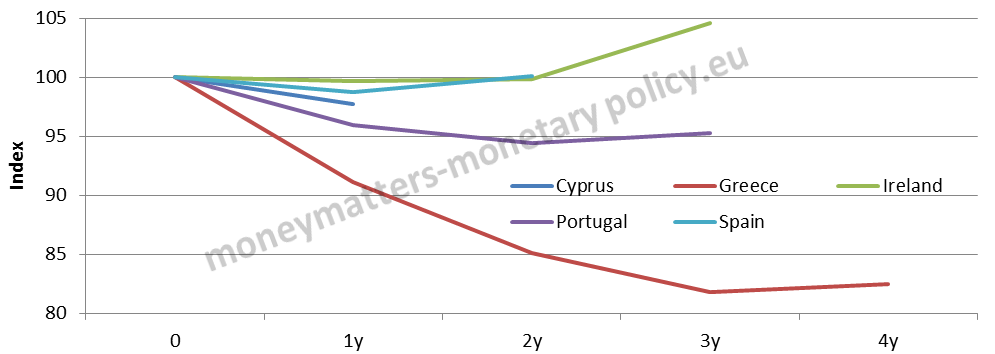

Chart 2 presents the “cross-section” evidence: GDP at the beginning of the adjustment program for Greece, Portugal, Cyprus, Ireland, and Spain is indexed to 100 and its path in subsequent years is charted for the different countries. In the chart one sees that Greece has been a totally different case from the other 4 countries that followed the “troika prescriptions”. While there are some differences between them, Greece stands out as a fully divergent, and much worse, case.

Chart 2. GDP dynamics in the years after the start of the Economic Adjustment Programmes

Source: IMF WEO April 2015

So, the Greek program was a failure looking both at its development over time as well as comparing the experience of this country to that of the other troika countries.

Now, how can we explain the difference?

Let me recall first some elementary concepts.

Austerians and Keynesians, to use too coarse qualifications, admit the obvious fact that, given the standard income equation:

Y=G-T+C+I +X-M,

(where G-T is the budget deficit, C is consumption, I is investment and X-M is the trade balance) reducing the budget deficit decreases aggregate demand and this will have an effect on economic activity and therefore on unemployment. The disagreement between the two schools of thought starts when one has to determine what happens after this obvious impact effect. Austerians think that there would be a fast offset of a reduced budget deficit on aggregate demand from its other components: consumption, investment and net exports. The lower interest and exchange rates as well as the confidence effects of fiscal tightening are the mechanisms that should lead to this offsetting mechanism. In a small open economy, the net export effect is likely to be the most important offsetting demand component. In some special circumstances, for instance when the confidence effects are very strong or the elasticity of net exports to a lower exchange rate is particularly high, there can even be positive demand effects from fiscal tightening, as the impact on consumption, investment and net exports is higher than the initial negative effect of fiscal tightening. On the contrary, Keynesians doubt the strength and rapidity of these compensating effects.

In the light of this elementary framework, we can look at what happened in Greece in comparison to what happened in the other troika countries.

A first look at the current account, in chart 3, does not indicate any substantial difference between Greece and the other countries: all of them, after the beginning of the crisis, achieved a fast reabsorption of the current imbalance as they moved from a deep deficit to about balance or surplus.

Chart 3 Current account balance

Source: IMF WEO April 2015

Somewhat similar was the behaviour of Unit Labour Costs (Chart 4), which were substantially reduced in all troika countries, recovering part of the competitiveness lost with respect to Germany in the initial years of monetary union.

Chart 4 Unit labour costs, total

Source: OECD

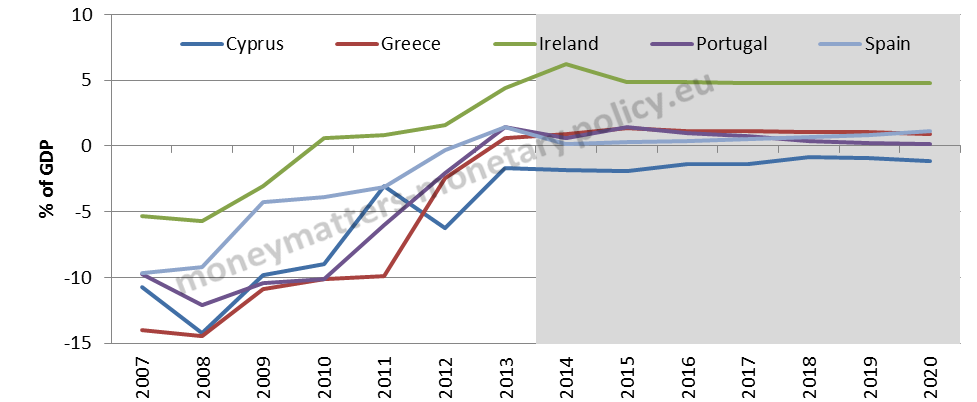

The differences start to emerge when we look at fiscal policy. Chart 5 shows that the fiscal correction started in a much sharper way in Greece than in the other troika countries.

Chart 5: Cyclically adjusted fiscal balances since the start of the programmes

Source: IMF Fiscal Monitor

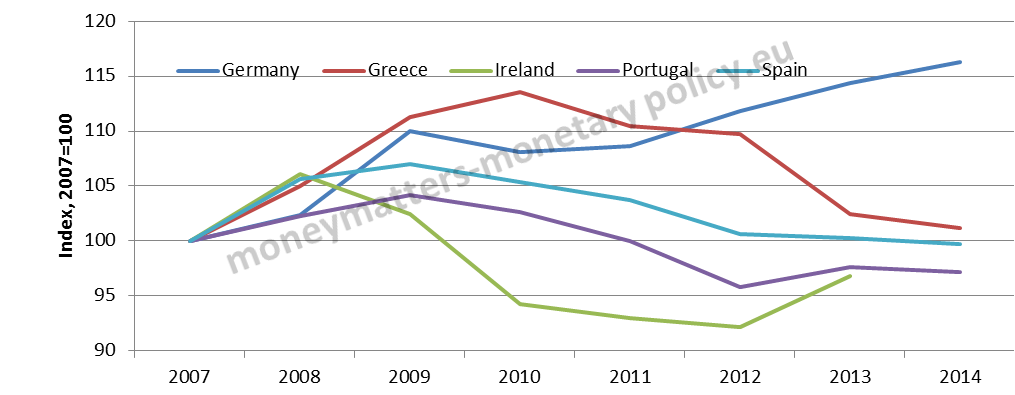

There is also another, in a way more interesting, difference between Greece and the other troika countries. This emerges in Chart 6, reporting the level of exports indexed at 100 in 2007.

Chart 6 Export volumes

Source: AMECO

Here again the different behaviour of Greece is obvious: in Spain, Portugal and, particularly, Ireland exports increased much more than in Greece. Only in Cyprus did they increase less, indeed nearly stagnated.

Table 1 zooms on this phenomenon, showing that, differently from other countries, the bulk of trade account adjustment was achieved through lower imports rather than higher exports, because of demand compression. Both the composition of exports and their geographical destinations contributed to this result, but it does not seem possible to explain the sharp difference between Greece and the other countries just on their basis.

Table 1: Changes in imports/exports (2014 to 2007)

Note: Data in € billion.

Source: AMECO

The same phenomenon is seen in investment: In Ireland, Spain and Portugal investment decreased as a per cent of GDP, with respect to 2007, by some 40 per cent, in Cyprus by 50 per cent and in Greece by 60 per cent.

Chart 7 Investment as per cent of GDP

Source: IMF WEO

The evidence is thus not only that fiscal adjustment was more intense in Greece, but also that the substitution effects between reduced public demand and increased private demand, and in particular investment and exports, was much smaller, hence the much bigger drop of GDP.

The following, logical question is to ask what was behind the lower substitution effect. An answer can be found in the weakness of the productive apparatus in Greece. One symptom of this is the structurally very low market share of global exports of Greece.

Table 1. Market share of global exports of Greece and other troika countries in 2007

Source: WTO

In the table one sees that Greece has a share of global exports of only 0.17 per cent, while Portugal, for instance, with an economy 25% smaller, has a share of global exports that is twice as large. The comparison is even more extreme in the case of Ireland but goes in the same direction for the other troika countries, except Cyprus. So structural conditions denoted a weakness of the productive apparatus of Greece.

In a forthcoming Bruegel publication, Alessio Terzi convincingly shows that this initial weakness was not remedied in the long adjustment programs of Greece. Indeed the structural measures carried out by Greece in complying with the programs, while important in quantity, were concentrated, in the IMF classification reported in the MONA statistics, in the General Government category, which produces growth effects only in the long run. Instead reforms in the “Other structural measures” category, mostly having to do with the product market, which generate much quicker growth effects, were introduced later in the program and constituted only a small part of the total implemented measures.

One way to summarize the results identified so far is that, because of the weakness of the private sector, Greece was not capable of moving from an economic model dominated by public demand and the production of non-tradable goods, to an economy with a more vibrant private sector producing tradable good. In these conditions, the very sharp fiscal adjustment had particularly negative demand effects since exports and investment could not offset it.

One can ask, what are the implications of the analysis conducted so far for the dramatic events taking place just now?

A first implication is that the latest offer by the creditors to resume the program of assistance to Greece was far from perfect, since it still did not recognize sufficiently the need of strong structural measures to re-launch growth in Greece, instead further insisting on fiscal adjustment.

A second implication is that in the absence of an agreement, however imperfect, there is not even the hope that the necessary structural measures will be taken in a subsequent period. The results of the forthcoming referendum are decisive in this respect: a yes vote would re-open negotiations on the adjustment program and one could hope that it would be much stronger on structural measures to revive growth. At the same time it should be recognized that, unless growth surprises dramatically on the upside, Greece will need some form of alleviation of its debt.

A third implication is that the large devaluation of the new currency that would follow Grexit would be unlikely to generate large export flows, given the persisting weakness of the Greek productive sector.

This post was prepared with the assistance of Madalina Norocea. Olivier Ginguene of Pictet Banque and Alessio Terzi of Bruegel provided very useful comments. This version corrects a previous one containing a chart on exports that was affected by a mistake.

- My take of what could happen between Greece and its creditors[↩]

- Data according to Angus Maddison Project[↩]

- Mexico in 1981-1986, Russia in 1997-1999 and Argentina in 1998-2002[↩]

thank you for sharing. why Austerians think that there would be a fast offset of a reduced budget deficit?

They probably overestimated the ability of the Greek productive sector to move from satisfying public demand to satisfying foreign demand. In addition they probably also had too optimistic a view on the effect that structural changes would have on expectations and thus investment. So the two possible offsetting factors, foreign demand and investment, did not compensate the reduction in demand coming from the fiscal tightening.

sorry for asking this, but are the colors in chart 6 still wrong ? Reading the legend, it seems Greek export are actually rising, which btw is what I have seen elsewhere.

Many thanks, indeed you spotted a mistake in the chart on exports, which has now been corrected. The conclusions of the post remain unchanged.

Are the colours for Ireland and Greece swapped on chart 6?

Many thanks for having noted this, indeed the two legends are inverted. I will correct it now.

Nice. Enightening. I have one point to add: service exports of Greece are strong (10% of GDP surplus on the service account). And service exports did really well, in 2014. https://rwer.wordpress.com/2015/03/15/the-10-of-gdp-greek-surplus-on-its-services-trade-balance/

With regard to the manufacturing sector your analysis and the probable disappointing results of a possible devaluation you seem to have the same analysis as Varoufakis in 2012 http://yanisvaroufakis.eu/2012/05/16/weisbrot-and-krugman-are-wrong-greece-cannot-pull-off-an-argentina/

Many thanks for the useful comments.

I wonder how the effect is of the size of the shadow economy, which could be up to 40%, and the effect of the real taxation being so much lower than the supposed taxation. Would that change your explanation and conclusion?

This is a good point. However my analysis was all about changes rather than levels and thus a large share of the shadow economy would not affect the conclusions, unless this share had increased a lot during the period of analysis.