Upward bias vs. downward bias: who will win?

ECB President Draghi confirmed, at the last press conference on September 5th, the unanimous view of the Governing Council: “we wanted to make it clear that we have a downward bias in interest rates for an extended period of time.“ He also said that “The Governing Council confirms that it expects the key ECB interest rates to remain at present or lower levels for an extended period of time. “

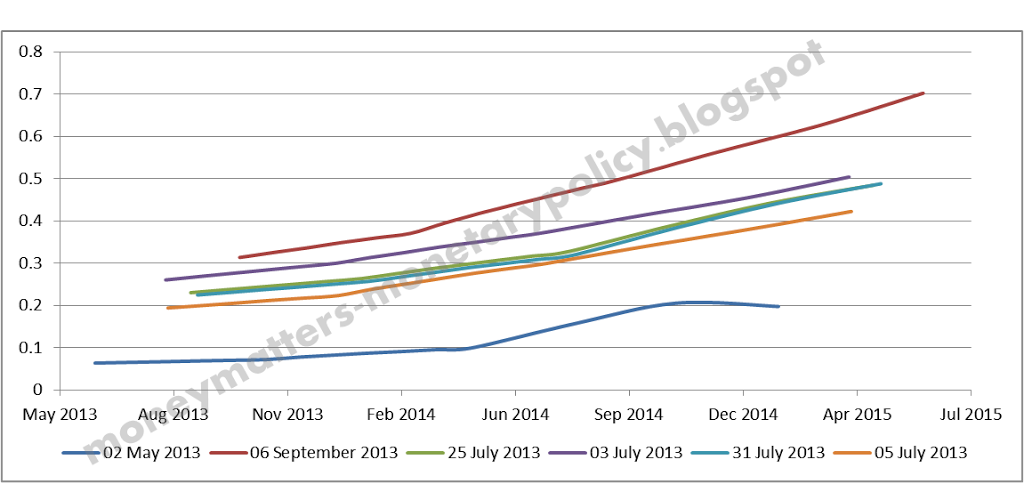

The market has an opposite, upward bias, which got stronger over time, notwithstanding the ECB forward guidance. As seen in the chart below, after the last rate cut by the ECB, at the beginning of May, the money market yield curve was quite flat until the end of 2015; instead, just after the last press conference on September 5th, it indicated a forward overnight money market rate (EONIA) above 35 basis points at the turn of next year and at 70 basis points by mid 2015.

While it is not clear whether the downward bias of the ECB Governing Council refers to the EONIA or to the official (Main Refinancing Rate – MRO) rate: the emphasis in the last press conference on the liquidity situation and on the effect that its developments could have on interest rates shows that the ECB also cares about EONIA and not only about the MRO rate. In any case, while the correlation between EONIA and the MRO is not precise, as it depends on the level of excess liquidity (currently EONIA is around 10 basis points while the MRO is at 50 basis points), still, an EONIA at 0.7 per cent is only consistent with at least one quarter point increase of the MRO.

While it is not clear whether the downward bias of the ECB Governing Council refers to the EONIA or to the official (Main Refinancing Rate – MRO) rate: the emphasis in the last press conference on the liquidity situation and on the effect that its developments could have on interest rates shows that the ECB also cares about EONIA and not only about the MRO rate. In any case, while the correlation between EONIA and the MRO is not precise, as it depends on the level of excess liquidity (currently EONIA is around 10 basis points while the MRO is at 50 basis points), still, an EONIA at 0.7 per cent is only consistent with at least one quarter point increase of the MRO.

Chart 1: EONIA 1 Year Forward Curve

|

| Source: Bloomberg |

So, there is a clear contrast: the Governing Council of the ECB has a unanimous downward bias, the market expects that both the money market and the official rate of the ECB will be increased steadily over the next few quarters.

The upward bias of the market seems inconsistent with inflationary perspectives. The ECB projections show that inflation should be well below the 2.0 per cent objective for both 2013 and 2014 (precisely 1.3 per cent in the latter year). While the ECB has not given its projections for 2015, President Draghi said in the last press conference that “Underlying price pressures in the euro area are expected to remain subdued over the medium term” and there is little expectation that inflation would move away from a level below 2.00 per cent in 2015 or beyond. If it is not higher inflation, what then explains the upward bias of the market?

There are 3 possible explanations for the steepening of the money market yield curve in the euro area:

1.The evaporating excess liquidity due, in particular, to the fact that banks are returning gradually the funding obtained under the 2 three year Long Term Refinancing Operations,

2.The confirmation of the ECB view that the recession is over and that the financial crisis is losing intensity,

3.The spill-over from the rate increase in the US triggered by the “tapering” announcement of the FED President.

Explanations 1 and 2 are clearly interrelated as banks are returning liquidity to the ECB just because of the improvement in financial and economic conditions. Let me therefore concentrate on explanations 1 and 3.

The effect of evaporating excess liquidity on EONIA was illustrated in a previous post by Daluiso and me on Bruegel at the beginning of July (Can the European Central Bank control interest rates?). In the mean time, the estimate for excess liquidity projections derived from the relationship between this variable and the forward EONIA curve has come down: at the beginning of July we estimated that excess liquidity would remain higher than 200 billion at least until Spring 2014, because at that time the money market yield curve was flat until then; now, the steepening of the curve is consistent with a gradual reduction of excess liquidity and its disappearance by the summer of 2014. In the Bruegel post we also explained the mechanism which is behind the relationship between excess liquidity and EONIA: when excess liquidity is very abundant (higher than 100 billion € or so) market participants are sure that the maintenance period will end with an excess of liquidity and the only relevant rate is the one at which banks will be able to place their liquidity surplus with the ECB, i.e. the deposit rate, currently at 0 per cent. For lower levels of excess liquidity market participants start to be unsure on whether the maintenance period will end with a surplus or a deficit of liquidity and the market rate will start moving towards the centre of the corridor, corresponding to the rate on the MRO. If market participants would be assured that the ECB would achieve neither a deficit nor a surplus at the end of the maintenance period (as it happened before the crisis) EONIA would stick constantly very close to the Main Refinancing Operation rate, in the middle of the corridor.

While the empirical relationship between excess liquidity and the EONIA is quite strong, President Draghi rightly stressed that it is far from precise, especially when liquidity starts moving towards zero, and that it depends on other factors. Here the spill-over from the United States comes into play, which follows a well established pattern, whereby rates in the US influence rates in the rest of the world, including in the €-area (Nathan Sheets of Citi had an interesting piece on this on September 5th 2013: Why Are Long-term Rates So Correlated across Countries? – The Role of U.S. Monetary Policy)

In conclusion, the Governing Council has good reasons, mostly of macroeconomic nature, for its downward bias: the control of inflation in the €-area surely does not need higher rates for the foreseeable future. But the market has also good reasons, mostly of financial nature, to have an upward bias. How could the conflict be resolved?

In principle the answer is simple: in the blog post mentioned above, Daluiso and I expressed a doubt about the ability of the ECB to control interest rates, but concluded, albeit hesitantly, that the ECB can control money market rates if it really wants to. This was also the view of the ECB President when he said, referring to the possibility to lower rates: “In any event, we would – as I said – stand ready to take appropriate action as needed.” The practical, and relevant, question is whether the Governing Council wants to enforce its views on the market, judging that macroeconomic reasons trump the financial ones and that the ECB, not the FED, should decide on interest rates in Europe. The answer to this question will determine whether the official rate will be lowered once more in the euro area or not.

[1] Valuable comments were provided by Giuseppe Daluiso.

[2] Research assistance was provided by Mădălina Norocea.