The assessments going around about the package of measures decided by the ECB at its last meeting at the beginning of June are definitely mixed. Some observers are more optimistic than others about its effect, in particular about its ability to remedy the gradual erosion of inflationary expectations and thus reconfirm the achievement by the ECB of its own price stability objective.

I shared this indecisiveness, as I first expressed a “not overwhelming” assessment, which I then upgraded into a “fair chance” one [1]. My warming up to the program was due to a simple reasoning. An impaired, undercapitalised and opaque banking system cannot effectively transmit to the economy the monetary policy impulse imparted by the central bank, however the Comprehensive Balance Sheet Assessment by the ECB should just lead to the repair, recapitalisation and transparency of the €-area banking system and thus give more power to the June package. In a way, the supervisory hand of the ECB is collaborating with the monetary hand and thus achieving a synergy: the ECB thus does not look like the mythical one handed economist, unable to come to a univocal conclusion.

My “warming up” to the ECB package is, still, short of enthusiastic and a 50/50 fair chance does not dispense of the need to closely follow developments to see which way things are moving.

In this post I would like to give my toolkit of indicators to see how things are moving: are they confirming the optimistic assessment, the “fair chance” view, or rather the pessimistic one, the “not overwhelming” one? A periodic assessment of the indicators could help conclude whether the ECB is progressing towards regaining its own definition of price stability.

My indicators, chosen among high frequency ones in order to have timely information, are the following, more or less ranked in order of importance:

- Inflation prospects,

- Exchange rate,

- Medium-long run yields,

- Short term rates.

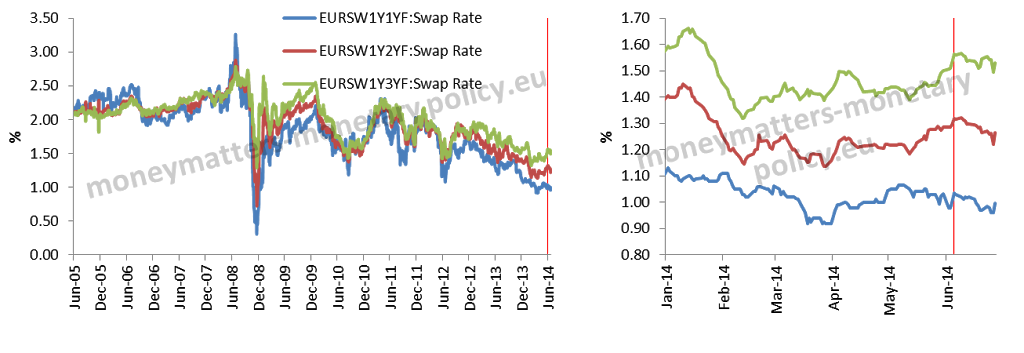

On inflation prospects the only high frequency indicators are break-even inflation rates drawn from the comparison between inflation protected and straight bonds (or from inflations swaps). It is useful in this respect to look both at measures not affected by inertia, like inflation break-even with one year maturity 1, 2 and 3 year forward (Chart 1) as well as steadier measures, less affected by transient shocks, like the 10 year break even inflation (Chart 2) and the five year maturity 1 and 5 year forward (Chart 3). In the charts, the red vertical bar marks the day of the ECB package in June.

Chart 1: Euro swap inflation break-evens, 1 year maturity, 1, 2 and 3 years forward.

Chart 2. French and German inflation 10 year break-evens

Chart 3: Euro swap inflation break-evens, 5 year maturity 1 and 5 year forward

Common source: Bloomberg, Barclays Live

Overall, a sharp eye would only be able to find a little upward move in Chart 3, with the 5 year forward break-even inflation. The other measures of break-even inflation do not show, at least so far, any significant upward move.

On the exchange rate, it is useful to look at both the €/$ rate as well as to the effective exchange rate of the € (Chart 4). There one finds a slight weakening in the first few days after the move by the ECB, but most, or all, of the fall was reabsorbed in the subsequent days.

Chart 4: EUR nominal and effective exchange rate

Source: Bloomberg

Chart 5 reports the changes of short term rates (EONIA, the 3 month and 1 year Euribor and OIS) as well as the change in sovereign yield since the ECB package. For this latter variable, given the difficulty of choosing one single sovereign as representative of the €-area (German securities are lowered by a safe haven effect which symmetrically increases the yields on peripheral bonds), an effective sovereign yield has been computed.

Chart 5: Interest rate changes since the June 5th ECB measures

Source: ECB, Bloomberg, Author’s calculations

Note : The Euro area yield Index weighs with the relevant ECB capital key the yield on the generic 5 year bonds of the relevant jurisdictions. The capital key has been re-based to 100% to include the following countries: Italy, Spain, Germany, Portugal, Ireland, France, Netherlands, Belgium, Greece, Finland, Austria, Slovenia, Latvia.

Of course, other events could have impacted the reported interest rates, even if nothing particular comes to my mind. In any case, the chart indicates a significant fall of EONIA and Euribor and, particularly, of the composite sovereign yield.

My overall assessment of the kit of indicators is that it is too early to conclude whether the “not overwhelming” or the “fair chance” interpretation is being borne out by developments about one month after the ECB package. Still, one can find a glimmer of hope in the fact that longer maturity variables (five year forward break-even inflation and the composite sovereign yield) have started to move, albeit slightly, in the right direction. Indeed it is encouraging that nominal yields have come down while inflation break-even have slightly increased for medium-long term term maturities. Even under this positive interpretation, however, we would need a number of years before inflation would approach again the 2.0% level. The risk of inflation remaining too low for too long cannot, for the time being, be excluded. Still, as the Latins said: “Spes Ultima Dea”.

———————————————————————

[***] Madalina Norocea provided research assistance

[1] A fair chance for the European Central Bank