Is the €-area in 2014 like Japan on the dawn of deflation?

If you are impatient and somewhat trust my judgment, let me give first my synthetic answer to the title question: out of the five criteria I use to compare the current situation in the €-area to that in Japan at the end of the ´90s, two (current situation of the banking sector and inflationary expectations) do not indicate that the €-area is in a better position than Japan when it was about to enter its deflationary period. On one other criterion (central bank activism) there is a slight advantage for the ECB. On the two last criteria (the prospective cleaning up of the banking sector and demography) the situation in the € area is clearly better than it was in Japan. Overall, my sense is that, in particular taking into account the recent hesitations of the ECB to confront too low inflation, confirmed in the last press conference, and the now weakly anchoring of inflationary expectations, one cannot exclude a significant risk of Japanification for the €-area.

If you are patient and want to see my reasoning before accepting my conclusions, here is it.

In Chart 1 we have a nice match between quantitative and literary developments in Japan and, so far, in the €-area. The line about Japan shows how the verbal description of the situation by the Bank of Japan worsened as the deflation got entrenched. The, so far much shorter, ECB line shows a first verbal change with inflation expectations no longer being anchored in the medium term but only in the medium to long term. The fear is that the prolongation of the ECB line and wording will follow the same, worrisome, path of the Bank of Japan.

Chart 1: Core CPI vs central bank literary description

Source: ECB, BOJ

In order to compare the €-area and Japan it is useful to look at the reasons Draghi gave for concluding that the situation in the €-area is better than that of Japan at the dawn of its deflation period. I will look at his reasons, add one of my own to conclude about the validity of the statement that the €-area finds itself in a much better situation than Japan.

1. “The first one [of Draghi reasons to differentiate the €-area from Japan ] which is the most important, i.e. that the ECB has taken decisive action at a very early stage of this crisis. “

Chart 2 reports, in the left panel, the comparison between an estimated Taylor rule and actual interest rates in Japan. The right panel does the same for the €-area.

Chart 2: Taylor rates vs actual policy rates

Source: ECB, BOJ, OECD, Authors’ calculations

Notes: Taylor rules defined as Taylor rule= 1+1.5*inflation rate -1*(unemployment rate -NAIRU); Quarterly NAIRU rates were obtained via linear interpolation ; Core CPI was used as the inflation rate.

Comparing the two experiences, it is not obvious that the ECB has been so much more decisive in its action than the Bank of Japan. Indeed it looks like the Bank of Japan was quite more expansive than the Taylor rule would have implied in the second half of the 90´s and it was only towards the end of the decade, when the Taylor rule would have started to require deeply negative interest rates, that policy rates, bound to zero, indicated a tighter monetary policy stance. Similarly, the comparison between the estimated Taylor rule and the ECB rates would show an easier policy for the ECB until the most recent period, when the Taylor rule would require negative rates also for the €-area.

Of course, during the crisis the interest rate has no longer been a sufficient indicator of monetary policy and the size of the balance sheet has been an important additional policy tool. According to this metric, until Kuroda-san announced the new policy, as the first arrow of Abenomics, the ECB, with its full allotment policy, was much more expansionary than the Bank of Japan.

Considering the two indicators together, my judgment is that there is a slight advantage for the ECB when it comes to “activism” against too low inflation. This is significantly mitigated, however, by the timidity recently shown by the ECB in dealing with the risk of inflation remaining too far from its 2.0% objective for too long.

2. “The second is that the condition of the balance sheets of the banking sector and the corporate sector is not as bad as it was in the 1990s there. “

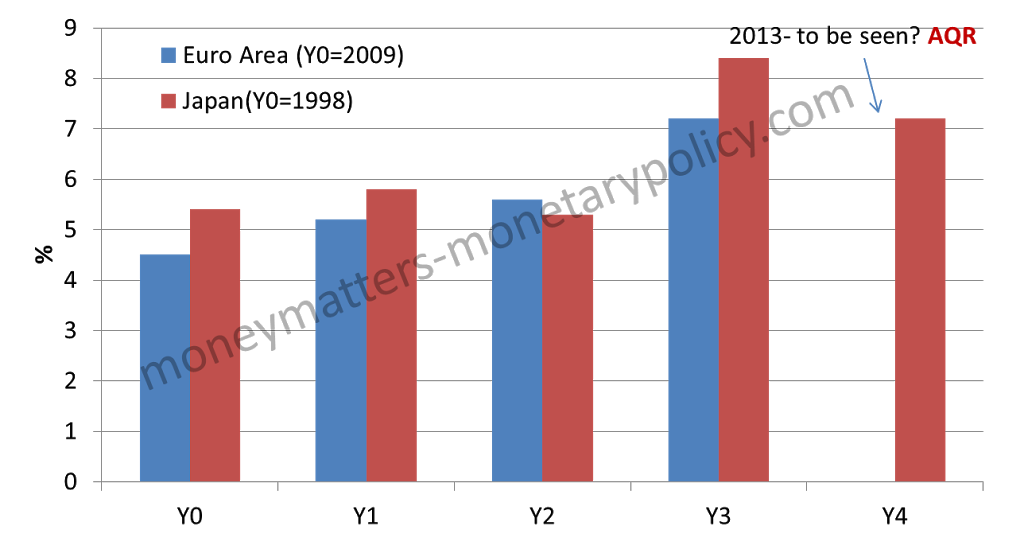

To assess the conditions of the balance sheet of the banking sectors of Japan and of the €-area it is useful to look at one direct and at two indirect indicators. The direct indicator is in Chart 3, reporting the non-performing loans of the two areas as a share of total loans.

Chart 3: Non performing loans

Source: FRB

Notes: Data represents the ratio of defaulting loans (past 90 days) to total gross loans.

A look at the chart does not reveal a strong difference between Japan at the end of the ´90s and the €-area since 2009: while non-performing loans have been usually somewhat lower in the €-area, the difference is not striking.

In Chart 4 the first of the two indirect indicators is represented: the equity price of €-area and Japanese banks as well as the general stock index in the two jurisdictions, rebased at the respective base year (1997 for Japan and 2007 for the €-area). The comparison is not favourable to €-area banks: while the general equity index recovered, at the end of the reported period, much of the losses accumulated since the base year in both the €-area and Japan, the index of €-area banks is less than 50% of the initial level while that of Japanese banks was higher than 60%.

Chart 4 Equity prices: general and bank indices

Source: Bloomberg

In Chart 5 the second of the indirect indicators is represented: the change in the stock of credit to the private sector. Here the comparison is definitely more favourable to €-area banks: their loans have been mostly decreasing but less precipitously than in Japan.

Chart 5: Loans outstanding

Source: ECB, BOJ

Note: BOJ data represents total loans outstanding of domestic banks; ECB data represents total outstanding loans to non-financial institutions.

Overall, a judgmental summary of the three pieces of evidence presented about the banking situation is not clearly in favour of the €-area: is it too ecumenical to conclude with a draw?

3. “The third reason is that we are now proceeding fast with the asset quality review (AQR), which will lead to the repair of our banking system. “

Here I am very keen to agree with Draghi. The Asset Quality Review and the Stress Test promise to be a watershed in the situation of the banking sector in the €-area. In a previous post [1] I illustrated the technical and political difficulties the ECB has to overcome to carry out this task prior to assuming its supervisory responsibilities. I also concluded, however, that the ECB is likely to win this new, difficult challenge. The fact that it has passed even more difficult ones in the past, like smoothly introducing the €, the awareness of the enormous stakes at play and the legal and organizational tools at its disposal make me think that, although difficult, the entire process will end up clearing the air from the opacity which has affected so far the €-area banking system. The strong balance sheet cleaning actions by Italian banks (Unicredit and Intesa) signal that the process is already having positive effects.

4. “And the final reason is that if we look back at how long-term inflation expectations were actually behaving in Japan at that time, we would find out that they were actually not firmly anchored. That is why it is so important that our inflation expectations remain firmly anchored, because they tell people that in a certain amount of time, over the medium term, inflation will go back to our objective, namely close to but below 2%.”

The reading of inflation expectations in Japan is more difficult than in the €-area, but research by the Bank of Japan can be used to compare the Japanese and the €-area experiences. Chart 6 reports the break-even inflation and the consensus forecasts together with estimated trend inflation drawn from a research paper of the Bank of Japan.

Chart 6. Inflation measurements in Japan

Source: Kenji Nishizaki; Toshitaka Sekine; Yoichi Ueno: Chronic Deflation in Japan, BOJ Working paper series, July 2012

Overall my sense is that the situation now in the €-area, as I have illustrated it in a previous post [2], is not significantly better than that of Japan since the half of the ‘90s. Initially, there the drop in inflation was expected to be temporary, in the mid of the ’90s, consensus forecasts for year-ahead Japanese inflation began to fall, but forecasts for 6-10 years out were broadly unchanged (in the range of 1-2%). By the end of the ’90s, 1-year-ahead forecasts for inflation had fallen below zero, but it was not until 2003 that zero inflation was expected on a longer-run horizon – some five years after Japan entered deflation. A key lesson for the ECB from the Japan experience is that, while focusing on long-term inflation expectations measures (the ECB cites 5y5y breakevens as its preferred benchmark) can be defended, short-dated inflation expectations dynamics provide important information on how long-term expectations are evolving. Looking closely at inflationary expectations, as illustrated in a previous post, we have started to see the erosion in the anchoring of medium to long term inflationary expectations in the €-area.

5. Demography (not on Draghi´s list).

The criteria listed by Draghi are mostly in the monetary and financial field, and clearly demography is in a different category. Still, I give so much importance to demography over a long horizon that I do not think one can compare the long term prospects of the €-area with those of Japan without also considering population developments.

In a growth accounting framework, as I examined in a previous post [3], labour force developments are a critical variable. The demographic situation is illustrated by Chart 7, presenting the labour force index and participation rates of Japan and the €-area. On both accounts, while not brilliant, the situation is much better in the €-area than in Japan.

Chart 7: Total labour force (lhs) and labour participation (rhs)

Source: Worldbank

One important factor in the better performance of the €-area is immigration, which is more significant than normally recognized in the €-area while it is practically zero in Japan, as it can be seen in Chart 8.

Chart 8: Net migration flows ( five year estimates)

Source: World Bank

So my bottom line is that on 2 criteria out of 5 (current banking sector situation and inflationary expectations) it is difficult to say that the €-area is in a better situation than Japan when it was about to enter its deflationary period. On one criterion (central bank activism) there is a slight advantage for the ECB, more on past merits than on current performance. On the last two criteria (demography and the prospective cleaning up of the banking sector) the situation in € area is clearly better than it was in Japan. Overall my sense is that, in particular taking into account the recent hesitations of the ECB and the weakly anchoring of inflationary expectations, one cannot exclude a significant risk of Japanification for the €-area.

________________________________________

*** Madalina Norocea provided research assistance to this post

I’m interested in your feedback to this endogenous money ISLM model. It suggests that monetary policy should shift focus away from interest rate targeting. Instead, central banks should try to match the monetary base to the demand for asset money. Also in regards to the zero lower bound, it calls for equipping central banks with new tools in the form of consumption and investment credits that can lift time preferences into positive territory thus reducing the demand for asset money. The model also offers a pretty straight forward explanation of the pro-cyclical nature of the gold standard and the Gibson Paradox.

http://tinyurl.com/k4vjswm