A cobweb in the Eurotower

Eurotower is the name of the building currently hosting the European Central Bank, waiting to move into its new premises later in the year, but it is not that the cleaning people in the Eurotower are not serious about their job: the cobweb I refer to in the title is the one presented in old microeconomic textbooks.

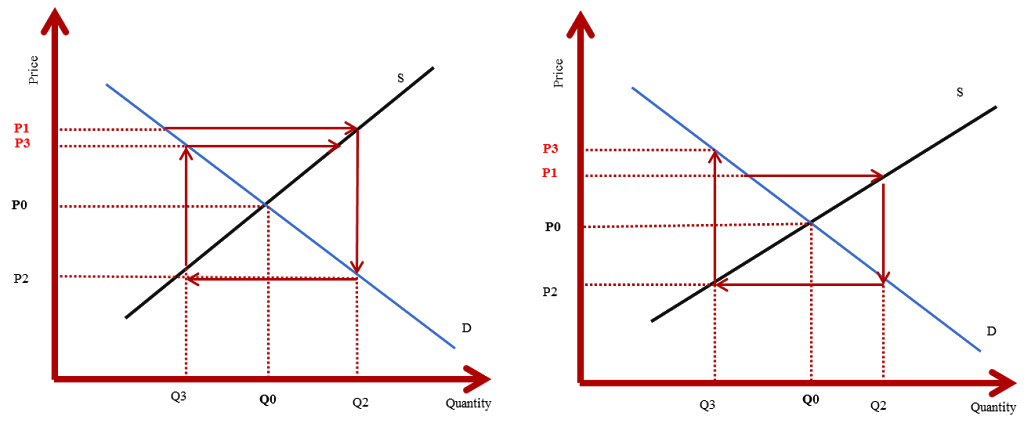

In the text I studied upon, back in the seventies (Henderson and Quandt, Microeconomic Theory, a mathematical approach), the chart of the stable and the unstable versions of the cobweb, respectively, was presented as follows:

In the text I studied upon, back in the seventies (Henderson and Quandt, Microeconomic Theory, a mathematical approach), the chart of the stable and the unstable versions of the cobweb, respectively, was presented as follows:

Chart 1: Stable ( lhs) and unstable (rhs) cobweb

|

| Source: Authors’ interpretation of cobweb model |

The story was that if supply is a function of yesterday´s price while demand depends on today´s price (as it would happen in the production of goods with a long production cycle, like an agricultural one), then price and supply movements in a chart like the one I reproduced above would depict a “cobweb” with the stable or the unstable version depending on the relative elasticities of demand and supply.

Of course, in more modern text book the issue would be presented in a much richer way, given the developments that have taken place in game theory and in the theory of economic expectations since my textbook was written. Still the original cobweb chart is sufficient to illustrate a pattern of the relationship between excess liquidity (which is the quantity in the cobweb chart) and the overnight interest rate (which is the price) that may be establishing itself in the €-area.

Before I analyse the issue, let me present the evidence. Chart 2 represents the EONIA and excess liquidity developments since beginning of November 2013. It is clear that the two variables have been much more volatile since the second half of December than before. At the end of last year there was obviously a reinforced end of year effect, as I argued in two previous posts. But the volatility spilled over into the first weeks of 2014.

Chart 2: EONIA and Eurosystem excess liquidity since November 2013

|

| Source: ECB SDW, Authors’ calculations |

The scatter diagram in Chart 3 however shows that there has been a (non linear) relationship between the two variables, albeit pretty noisy, during this period. This should not come to a surprise to those who have read some of my previous posts [1] in which I illustrated the relationship between excess liquidity and EONIA. In any case, to be refreshed about the empirical relationship between the two variables, look again at the long term scatter diagram in Chart 4, which shows a non-linear relationship between the two variables, whereby EONIA goes very close to the deposit facility rate (currently 0) for large amounts of excess liquidity (say higher than 200 billion) while it gravitates around the Main Refinancing Operations (MRO) rate when excess liquidity is close to zero [2].

Chart 3: Correlation between EONIA and Chart 4: Correlation between EONIA and

excess liquidity since November 2013 excess liquidity since 1999

Common source: ECB SDW, Authors’ calculations, in the vertical axis the difference between EONIA and the MRO rate is represented.

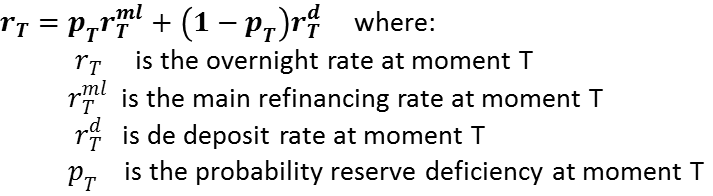

The President of the ECB has stressed in his last Press conferences [3] that, as one can indeed see in Chart 4, the relationship between excess liquidity and overnight rate is not precise. But a noisy relationship is still a relationship. And it is not only empirical observation that tells us that the two variables are connected. The fundamental equation of interest rate fixation in a corridor approach [4] tells us that when excess liquidity is very abundant banks know with probability one that they will end the maintenance period with an excess of liquidity and therefore the only relevant rate is the one on the deposit facility (currently 0), where they can place their excess liquidity. Before the crisis, instead, the ECB assured banks that they would end the maintenance period neither with a surplus nor with a deficit of liquidity and therefore the probability of an excess or a surplus of liquidity was the same and therefore EONIA was stable and close to the MRO rate, in the middle of the corridor between the deposit and the marginal lending facility rate.

The long term scatter diagram in Chart 4 tells us something more than there is a noisy relationship between excess liquidity and EONIA: it also tells us that the noise around the interpolating line grows steeply when the amount of excess liquidity moves below some 200 billion €, as banks have more dispersed expectations about the liquidity situation that will prevail at the end of the maintenance period. And 200 billion € just defines the region of excess liquidity which has been prevailing since December of last year, due to the fact that banks have returned, particularly in 2013, much of the liquidity they had borrowed under the two 3 year Longer Term Refinancing Operations.

So to summarise the points so far:

- Excess liquidity and EONIA have been particularly volatile over the last few weeks,

- Still the long term noisy relationship between the two variables, which can be explained in theory and observed in reality, applies,

- At the prevailing level of excess liquidity, the noise around the relationship between the two variables starts to be particularly high.

What I said so far does not justify as yet my “cobweb” story. To complete the picture you have to recall that it is banks that determine the amount of liquidity prevailing in the system: since October of 2008, in fact, the ECB satisfies in full the demand for liquidity of banks, having moved to fixed-rate full-allotment tenders. Less noticed, until recently, was another possible source of central bank liquidity in the hand of banks: the non participation to the weekly operations conducted by the ECB to sterilise the liquidity created by the purchase of peripheral bonds in the Securities Market Program, amounting currently to some 180 billion. By non participating to the operations banks “create” central bank liquidity, as it has happened recently.

Of course, the demand for liquidity of banks depends on its cost: when liquidity is cheap they will ask a lot of it, when it is expensive they will ask less. And the cost must be meant in a broad sense: 25 basis points, the current cost of liquidity drawn either from refinancing operations or (in terms of opportunity cost) by non participating to sterilisation operations, can be very cheap when there are tensions in the money market that push very high the rate (possibly the shadow rate) at which banks, particularly from the periphery, could borrow in the market. When tensions subside, 25 bp can start to be expensive and banks have less incentives to borrow from the ECB [5]. Indeed, as tensions have substantially come down, the demand for liquidity from banks has decreased and excess liquidity in the scatter diagram in Chart 4 has moved towards the “unstable” region below 200 billion. And here comes the “cobweb” pattern: when EONIA is low, banks draw little liquidity from the ECB (either participating less to refinancing operations or returning the liquidity borrowed under the two 3 year LTROs or, still, underbidding at the SMP sterilisation operations) but then EONIA moves up, possibly above the cost of ECB funding, which then becomes again relatively cheap and thus recreates an incentive to borrow from the ECB, but then liquidity increases, EONIA goes down and the incentive to borrow disappears and… the Perpetuum Mobile of Johan Strauss II is achieved. In short, banks have an incentive to borrow from the ECB when liquidity is scarce and interest rates are high, but in so doing they increase liquidity and bring interest rates down.

Sophisticating the analysis and making the behaviour of a rational bank to depend on its expectations rathe than the lagged price doesn’t lead to stability: it is profitable to be contrarian and to borrow from the ECB when other banks do not do it and do not borrow when other banks do borrow. But there is no way to know what other banks will do, hence the irregular oscillation up and down of the rate shown in Chart 2. Rational expectations do not solve the issue in this case as they can not settle the indeterminacy between individual and collective bank behaviour.

Sophisticating the analysis and making the behaviour of a rational bank to depend on its expectations rathe than the lagged price doesn’t lead to stability: it is profitable to be contrarian and to borrow from the ECB when other banks do not do it and do not borrow when other banks do borrow. But there is no way to know what other banks will do, hence the irregular oscillation up and down of the rate shown in Chart 2. Rational expectations do not solve the issue in this case as they can not settle the indeterminacy between individual and collective bank behaviour.

So, in current conditions, it is not by chance that the hinge of the yield curve, the EONIA rate, is unstable: there are systematic reasons for this instability.

If this is the diagnosis, what is the therapy? What can the ECB do to counter this instability?

I will not explore the theoretical case in which the ECB would regain control of liquidity by returning to fixed-amount variable-rate auctions, as it has formally stated that it will maintain full allotment fixed rate tenders at least until July 2015 [6] .But even leaving to banks the power to determine liquidity in the €-area, the ECB could counter the cobweb pattern if this were to continue for too long.

First, it could increase the outstanding liquidity in the system by stopping altogether the sterilisation operations, thus injecting, on an outright basis, some 180 billion of liquidity in the system. This could be reinforced by reducing the compulsory reserve coefficient, say by a half, thus injecting another 50 billion. This would bring back excess liquidity well into the area in the scatter diagram of Chart 4 where EONIA is very close to the deposit facility rate (0 currently). Of course, over time banks could reduce the amount of excess liquidity by returning larger amounts of money borrowed under the two 3 years operations and by borrowing less under the other refinancing operations. Still this would require plausibly a protracted period of time during which the cobweb would be avoided.

Another solution would be to give incentives to banks to borrow more liquidity, by making it cheaper. The obvious way to do this would be to lower the official rate, say from 25 to 10 basis points. This reduction would also apply to the maximum rate applied in sterilisation operations and therefore the cobweb pattern would have a more limited range to move.

Lastly, the ECB could find it more acceptable, as it does not require an official change of the MRO rate or an explicit decision to stop sterilisation, to just reduce, say to 10 basis points, the maximum rate of sterilisation operations, meaning that, whenever EONIA would move above that level, banks would have no incentive to participate to sterilisation operations, thus increasing excess liquidity [7]. In a way, bringing down the maximum rate on sterilisation operations to 10 basis points would mean that banks could borrow up to around 180 billion at that cheaper level, thus increasing their demand of liquidity. In current conditions, lowering the maximum rate on refinancing operations would lead to an easing of monetary conditions, even if less than a reduction of the MRO rate would do.

Lastly, the ECB could find it more acceptable, as it does not require an official change of the MRO rate or an explicit decision to stop sterilisation, to just reduce, say to 10 basis points, the maximum rate of sterilisation operations, meaning that, whenever EONIA would move above that level, banks would have no incentive to participate to sterilisation operations, thus increasing excess liquidity [7]. In a way, bringing down the maximum rate on sterilisation operations to 10 basis points would mean that banks could borrow up to around 180 billion at that cheaper level, thus increasing their demand of liquidity. In current conditions, lowering the maximum rate on refinancing operations would lead to an easing of monetary conditions, even if less than a reduction of the MRO rate would do.

Of course, the exit from the excess liquidity situation will have to be engineered at a certain point in time. But, as the forward guidance of the ECB made clear, that certain point in time is still quite far in the future and there will be time to think about the best way to return to a normal situation.

*** Research assistance was provided by Mădălina Norocea

[1]See previous posts: Three liquidity scenarios after the year-end and € liquidity is getting more valuable: what can be done about it?

[2] In difference terms, this means that the difference between EONIA and the MRO rate is zero when excess liquidity is zero while it is close to the difference between the MRO and the Deposit Facility rate when liquidity is very abundant.

[3] “(…) let me reiterate once again that it is very, very difficult to. If you look at the excess liquidity recorded on 19 December 2011, you will see excess liquidity standing at around €300 billion and the EONIA at 57 basis points. Let us then move to 15 May 2013: excess liquidity was €303 billion, i.e. roughly the same amount as on 19 December 2011, but the EONIA was only 8 basis points. It is thus very, very difficult to draw the conclusion that there is a stable relationship between the two variables.”, Mario Draghi, Press conference, 9th of January 2014

[4]

[5] The latter phenomenon is arguably reinforced by the fact that the stigma effect implicit in borrowing from the ECB increases the total cost of drawing liquidity from ECB operations

[6] “ (…)we decided today to continue conducting the main refinancing operations (MROs) as fixed rate tender procedures with full allotment for as long as necessary, and at least until the end of the 6th maintenance period of 2015 on 7 July 2015” Mario Draghi, Press conference, 7th of November 2013

[7] This approach was suggested to me in a conversation with Brian Sack, my former counterpart at the New York FED, who is now at the D. E. Shaw Group.