The Roman comic playwright Titus Maccius Plautus takes up an old adage of Greek origin when he writes in his Bacchides: “Quem di diligent, adolescens moritur”, which translated into English sounds: “Whom the gods love die young”. This is of course a paradox: the empirical proof that gods do not make a favour to those they love by making them die young is the fact that large shares of national income are devoted to maintaining or regaining health, in view of a long life. But, taking the same paradoxical line as Plautus, I am tempted to say: “Happy the countries that had the troika!”

The empirical proof that the troika has not been welcome is to be found in the press comments in those countries that had to ask for support from the European Union as well as in the fact that they unshackle from its control as soon as they can, as Ireland and Portugal have done. Yet there is truth in the fact that the troika did not only bring tough austerity and unemployment.

In three other posts [1] I have shown the huge reduction in the cost of government debt that the troika cure, together with the ECB action, has caused in peripheral countries and, symmetrically, the great capital gains achieved by those, including the ECB, that trusted the € and the €-area and bought peripheral bonds at the peak of the crisis. It is not exaggerated to say that yields on peripheral government bonds have moved away from being unbearable and leading eventually to default, to enter into a region where they are no longer clearly unwarranted. In addition, the troika has led to a re-absorption of unsustainable fiscal and balance of payment imbalances.

In this post I want to draw attention to another positive influence of the troika: the great improvements in the structural conditions in the product and labour markets. Of course, in the simple set-up I use, I cannot distinguish the effect of the market pressure (the bond vigilantes) from that of the troika, so, if you feel that they are missing, add the bond vigilantes to my title.

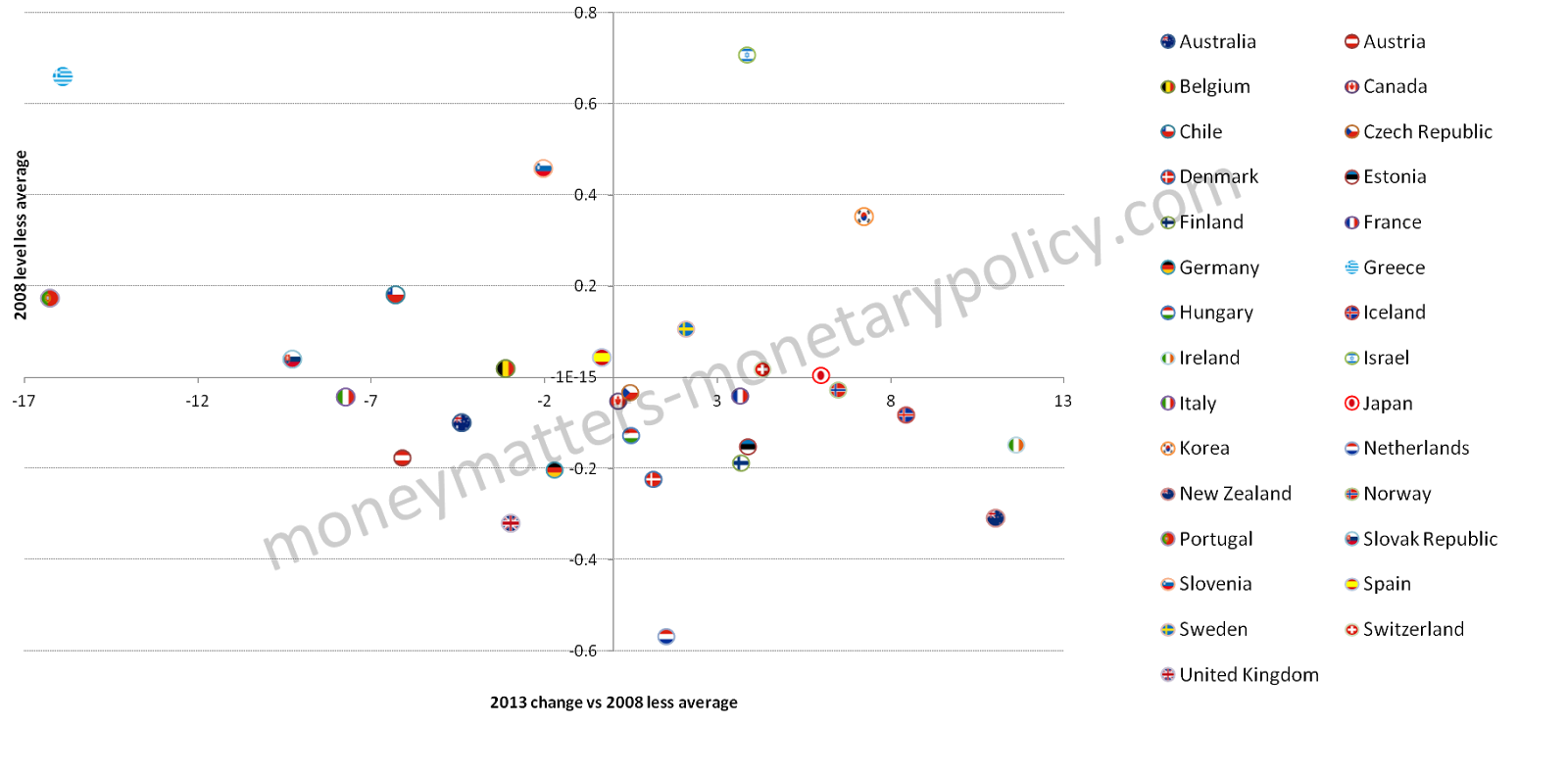

My synthetic point is made in Chart 1. This chart reports on the vertical axis a composite indicator of lack of flexibility and strength of competition in product and labour market in OECD countries in 2008 [2]. On the horizontal axis the changes in the indicator between 2008 and 2013 are reported. The observations for the individual countries correspond to the difference between the national value and the average over all countries considered. The weight of the product market indicator in the overall index is 60%, that of the indicator for permanent workers is 33% and that for temporary workers 17%. The weights reflect my subjective assessment of the importance of the three markets: the large weight for the product market reflects my assessment that the welfare implication of competition in the product market are much clearer than those of competition in the labour market, while the degree of flexibility in the market for permanent workers is more important than that for temporary workers. I regard my weights also as broadly consistent with the considerations presented in the OECD paper (referred to in the legend to chart 1), which clearly indicate that it is not true that labour protection should be as low as possible, while I think that it is difficult to make a case for the optimality of any rent or other form of lack of competition in the product market.

Chart 1: Composite indicator of Product Market and Employment protection

In the upper left quadrant of Chart 1 are the countries that had the highest composite indicator of rigidity and lack of competition in 2008 but have reduced it between that date and 2013. Here one finds all the peripheral countries (even those that only felt the breath but not the actual presence of the troika, like Italy and Slovenia) with the exception of Ireland. Indeed the most important moves towards flexibility and competition have been achieved by, in the order, Portugal, Greece, the Slovak Republic (not obviously a peripheral country), Italy and Spain. It is interesting to observe that France is the only €-area country with a high level of rigidity and lack of competition in 2008 that has not moved towards more flexibility and competition. So, both market pressure and institutional influence in the direction of change have been weaker in France than, say, in Italy or Spain, not to mention Portugal and Greece. So, taking again my paradoxical approach, I would say “Unhappy France that did not get the troika!”

It is also interesting to observe in Chart 1 that all Nordic countries (Sweden, Denmark, Finland, Norway, Estonia) as well as the Netherlands, Chile, Hungary, Austria, Switzerland and Japan are clustered around the origin, meaning that they had an overall indicator of flexibility and competition close to the average and they did not move much from it, while Anglo-Saxon countries are mostly in the lower right quadrant, meaning that they are characterized by more flexibility than the average country considered in the OECD analysis but they have, at least in some cases, reduced that since 2008.

Overall, the prevalence of countries around the North-West/South-East diagonal in the chart indicates a process of convergence towards the average flexibility across the member countries considered.

More detail can be obtained by looking separately at product market regulation (Chart 2) and labour market flexibility (Chart 3). The process of convergence towards the mean appears in both aspects but there are some interesting differences for some countries.

Chart 2: Product Market Regulation

For instance, Spain has done very little in reducing product market regulation, while doing quite a lot on the labour market. Somewhat the opposite holds for Italy, which has done more on product market regulation, even if it was already close to the average in 2008, but has done much less on employment, where it was well above the average. The performances of Greece and Portugal in increasing flexibility are outstanding in both areas, even if the level of flexibility still remains limited. The Netherlands is the most flexible country when it comes to product markets, but is close to the average in terms of employment flexibility. Nordic countries are clustered around the origin in both areas, while Anglo-Saxon countries show even more flexibility, relative to the average, in the employment than in the product market.

Chart 2: Employment protection- Regular contracts

So, in conclusion, a balanced assessment of the troika requires looking at the liability side but also at the asset side. The former basically consists of too intense and rapid increase of taxation and reduction of public expenses, which have brought with them a very high unemployment. The latter consists of the reabsorption of current account and fiscal imbalances, a sharp reduction of the cost of debt and, as argued in this post, quite some progress towards more flexibility in the product and labour market.

The bottom line depends, of course, on the weights that one attributes to the different effects. It is my sense, however, that the weights very much depend on the time horizon: over a short to medium term horizon, unemployment and the sharp increase in taxes and the reduction of public expenses weigh more, while the positive aspects get more weight as the horizon is lengthened. Stephen Jens has aptly said that, while Americans only thought about the demand side and the short to medium term, Europeans have put too much emphasis on the supply side and the long term. If this interpretation is correct, as time goes by the advantages of the European approach should become more evident, unless Europe will resign itself to a low growth trap.

————————————

[***] Madalina Norocea provided research assistance

[1] Trust in Europe paid handsomely!; Has the European Central Bank transformed itself into a hedge fund?; Where did smart money go in 2012?

[2] OECD defines the indicators as Product Market Regulation and Strictness of Employment Protection. The chart is constructed so that the higher a country is on the vertical axis the less flexible is the country while positive (negative) values on the horizontal axis indicate increases (decreases) in rigidity.