The international role of the euro

European Commission president Jean-Claude Juncker raised, in his latest State of the Union address on September 12th, an issue that has been somewhat dormant over recent years: the international role of the euro. Indeed, he announced that the Commission would present plans “to strengthen the international role of the euro” before the end of the year.

This statement raises two important issues:

- Should indeed the euro area pursue a more important international role for its currency?

- What are the tools that the euro area could deploy to pursue this objective, if indeed it is deemed desirable?

Any plan about increasing the international role of the euro should start from the current situation: what is the actual international role of the euro, i.e. its use outside the borders of the euro-area, and how has it changed over the two decades of its existence?

One very important and very clear fact is that the euro is the second-most important currency in all possible international uses, whether in the private or in the official domain. The first-ranking currency by a good margin is the dollar, while other currencies cover minimal shares.

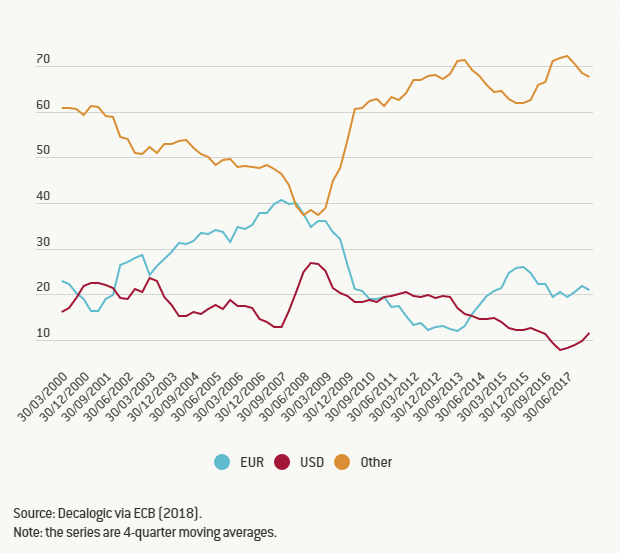

The ranking between the dollar and the euro has not changed in the last two decades, is very likely to remain unchanged in the foreseeable future, and can be seen as a continuation of the situation preceding the introduction of the euro – when the deutschmark and some other European currencies were internationally used. The shares of the dollar and the euro, however, have changed over time and what one has gained the other has lost. This is visible in all possible international uses of the two currencies by the private or the public sector, but is clearest in the role of the two currencies to denominate foreign currency bonds, as in Figure 1, i.e. when a resident of one country uses a foreign currency to issue debt.

Figure 1: Foreign–currency-denominated debt issuance by currency

The shares of the two currencies are of course much more stable if one looks at stocks, for instance of international bonds or foreign reserves, instead of flows as in Figure 1. But the phenomenon is still visible.

Theoretical considerations as well as empirical regularities allow for the establishment of the most important factors determining the relative international role of different countries:

- Size of the country issuing the international currency

- Development of the underlying financial market

- Freedom of capital movements

- Political and military power of the issuing country

- Financial stability of the issuing country, relative to the stability of other countries

- A policy by the issuing country to assist, or deter, the international use of its currency

The first four factors are characterised by strong inertia and therefore cannot explain the changes in the international use of the currencies that have taken place over the years. The last two, instead, can move quite significantly over time. One very important case in this respect is that of the fluctuations in the international use of the euro that took place before, during and after the Great Recession.

This is documented in Figure 2, reporting the share of foreign-currency-denominated debt issuance in euros as well as the degree of euro-area financial integration, as captured in the index calculated by the European Central Bank (ECB). Both series increased between the launch of the euro and the beginning of the Great Recession, decreased substantially in the course of that recession and started a recovery around 2012. This shows a high correlation between the international use of the euro and the stress in the euro-area financial market (as measured by the changes in its integration).

Figure 2: Foreign-currency-denominated debt issued in euro and index of financial integration

Taking into account the evidence in Figure 1, the question about the desirability of a more important international role for the euro can be formulated more precisely: should euro-area authorities pursue policies that would increase the share of the euro as an international currency?

One often-mentioned advantage of issuing an international currency, mostly elaborated with the example of the dollar in mind, takes the evocative name of “exorbitant privilege”1. International seignorage is the first item under this general term, referring to the pecuniary advantage deriving from the use of zero-yielding banknotes by foreign entities and from the lower yield on external liabilities due to the international demand for the sovereign paper of the country issuing the international currency.

While seignorage was estimated at a non-negligible 1% for the US,2 the much lower circulation of euro banknotes outside the euro area – with respect to the foreign circulation of dollar banknotes – and the absence of federal euro bonds – covering the same role as Treasuries – make this advantage much less significant for the euro area. Also, the cheaper external borrowing allowed by the issuance of liabilities in one’s own currency is less important for a jurisdiction, like the euro area, with large current account surpluses.

Another aspect, often mentioned for the US, is the “denomination rents” that banks derive from the use of their ‘home’ currency in international finance. As for seignorage, the advantage for European banks to conduct international business in their domestic currency is not as important as for US banks, since the former banks have significantly reduced their international activity during the financial crisis. In addition, for their international business, European banks use foreign currencies (in particular the dollar) more often than American banks.

Overall, the financial advantages stemming from the international use of the euro are quite limited. Analogously limited, however, are the disadvantages that could derive from such use for the conduct of monetary policy. These disadvantages made the Bundesbank reluctant to allow the deutschmark to be used internationally and are likely to have led the ECB to its policy of “neither hindering nor promoting the international use of the euro”. But the much larger size of the euro-area economy, with respect to that of Germany, and the emphasis of the ECB on interest rates rather than on monetary aggregates substantially attenuate the fear that external shocks may affect the conduct of monetary policy.

The most important benefit for Europe from a larger international role of the euro can be found in what one could call “financial autonomy”. The influence over the EU, deriving from the extraterritorial reach of US rules, decisions and policies granted by the very extensive international role of the dollar, would be reduced if the euro had a wider international use. This has become more relevant as the interests of the US appear more frequently different from those of Europe, as the case of Iran sanctions has recently shown. One could also link a wider international role for the euro to a multilateral set-up, in which the outsized role of any single currency would be reduced and competition between currencies would be enhanced.

Given the desirability of increasing the international role of the euro, the second question asked at the beginning of this piece is relevant: “What are the tools that the euro-area could deploy to pursue this objective?”

A larger international role of the euro could be promoted if the ECB would surpass its ‘neutral’ attitude towards it. This would carry an important message and could be linked to the repeated requests of the ECB to complete banking union and progress on capital market union. A possible operational development would be if the ECB would show willingness to to enter into a series of swaps with central banks of countries that are extensively using the euro, while maintaining under its control the drawings on the swaps, lest they affect monetary policy. The experience during the Great Recession has indeed shown that international money markets can seize up and central bank intervention may be needed to repair broken market intermediation. The opening up of swaps from the Federal Reserve of the United States to a number of central banks, including prominently the ECB, was a decisive step in this respect. The less forthcoming policy of the ECB in granting swaps to non-euro central banks was consistent with its ‘neutral’ policy towards the international role of the euro.

More importantly, the reversal of the gains in the international role of the euro accumulated in the first decade of monetary union, which accompanied the onset of the Great Recession, shows that substantial progress critically depends on the general stability of the euro area and, specifically, on the smooth functioning of its financial system. So, for instance, the completion of banking union, progress on capital market union, the surpassing of the shock that will inevitably be wrought by Brexit, and the creation of a common ‘federal’ bond – which would cover in the euro area the role that Treasuries play in the United States – are necessary steps to increase the international role of the euro.

In a broader perspective, progress also in the set-up of euro-area economic policy, in its fiscal and structural components, would favour a larger international use of the euro. In a still broader perspective, the international use of the euro would be expanded if the EU would pursue a more united, and thus more effective, external and defence policy.

These policies would have effects well beyond the international use of the euro and, while in principle desirable, they are not easy to be achieved. The choice to embark on them depends on broader considerations than just enhancing the international role of the euro. The right perspective is that the broader international role of the euro, and the ‘financial autonomy’ that this would bring, would be an additional advantage to be taken into account while pursuing the aforementioned, much broader, policies.

This post was written by Francesco Papadia and Konstantinos Efstathiou.

.

References

Cohen, B. (2012) ‘The Benefits and Costs of an International Currency: Getting the Calculus Right’, Open Economies Review, 23(1), 13-31.

McCauley, R. (2015) ‘Does the US dollar confer an exorbitant privilege?’, Journal of International Money and Finance, 57, 1-14

US Treasury (2006) ‘The use and counterfeiting of United States currency abroad. Part 3. Final report to the Congress by the Secretary of the Treasury, in consultation with the Advanced Counterfeit Deterrence Steering Committee, pursuant to Section 807 of PL 104–132, September’

Hey ,

I see website http://www.moneymatters-monetarypolicy.eu and its impressive.I wonder if the content or banners advertising options available on your site ?

What will be the price if we would like to put an article on your site?

Note : Article must not be any text like sponsored or advertise or like that

Cheers

hallet biran

Dear Sir,

many thanks for your enquiry.

I am not sure I understood what your request is. In any case I would not accept anything that is not written by me on my blog.